Answered step by step

Verified Expert Solution

Question

1 Approved Answer

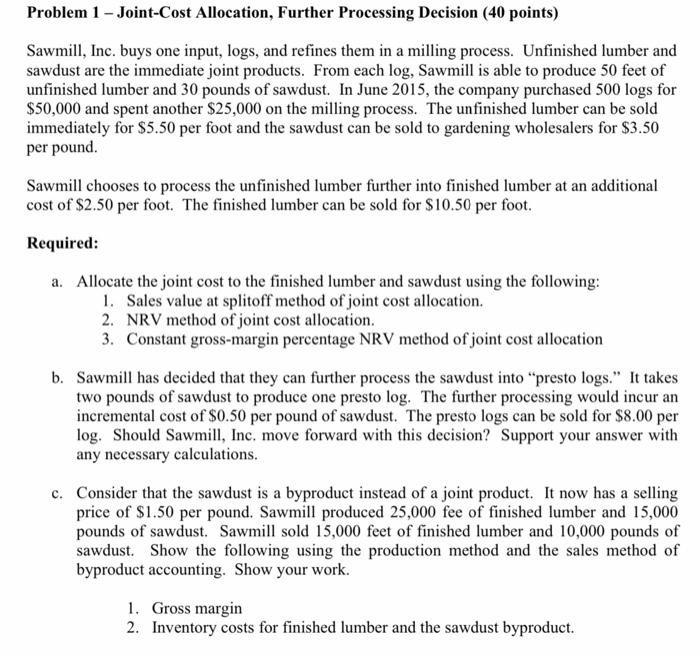

Problem 1 Joint-Cost Allocation, Further Processing Decision (40 points) Sawmill, Inc. buys one input, logs, and refines them in a milling process. Unfinished lumber and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Frank Woods Business Accounting Volume 1

Authors: Frank Wood, Alan Sangster

10th Edition

9780273681496