Answered step by step

Verified Expert Solution

Question

1 Approved Answer

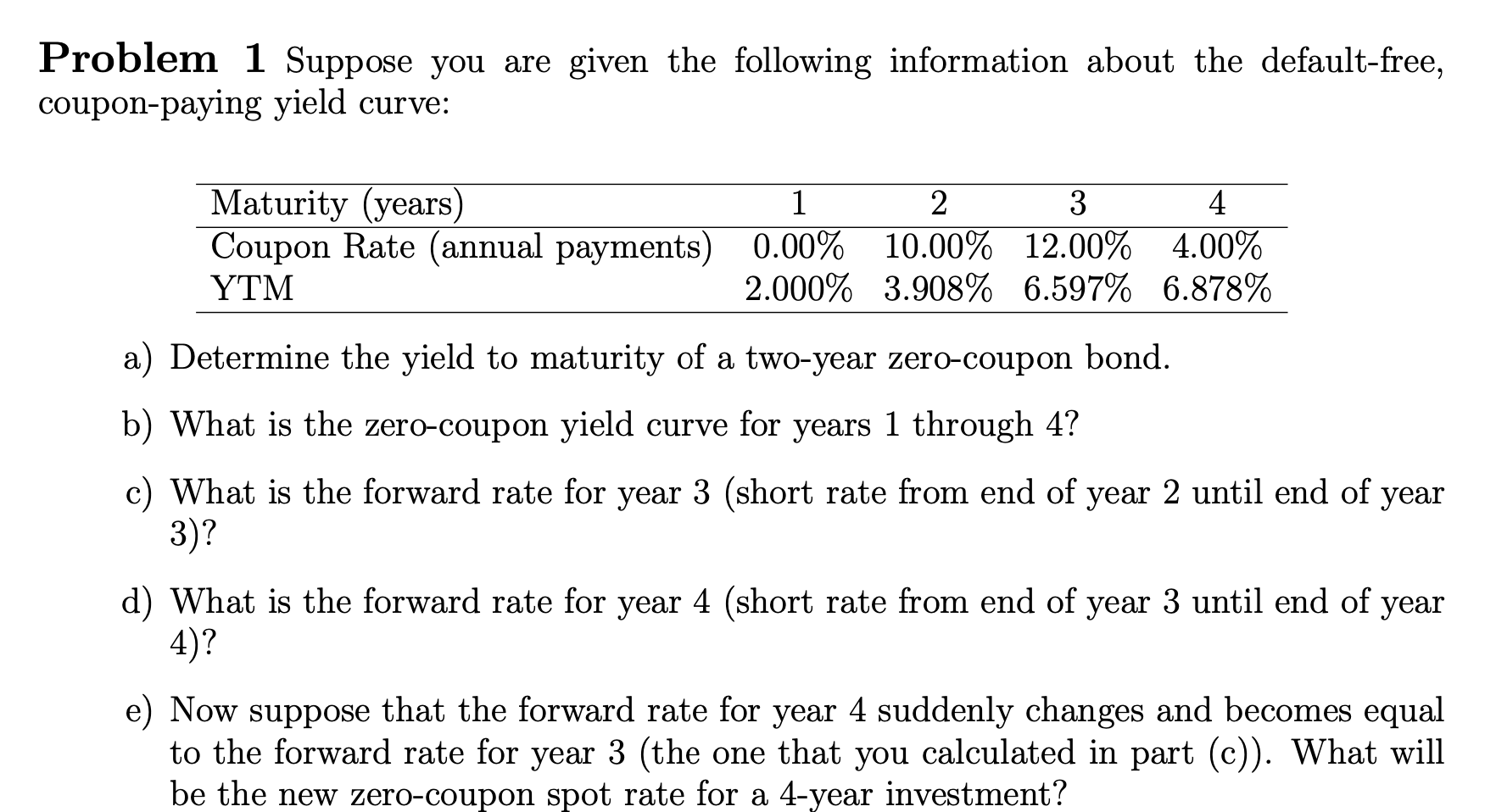

Problem 1 Suppose you are given the following information about the default - free, coupon - paying yield curve: a ) Determine the yield to

Problem Suppose you are given the following information about the defaultfree,

couponpaying yield curve:

a Determine the yield to maturity of a twoyear zerocoupon bond.

b What is the zerocoupon yield curve for years through

c What is the forward rate for year short rate from end of year until end of year

d What is the forward rate for year short rate from end of year until end of year

e Now suppose that the forward rate for year suddenly changes and becomes equal

to the forward rate for year the one that you calculated in part c What will

be the new zerocoupon spot rate for a year investment?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Financial Intermediation

Authors: Harold L. Cole

1st Edition

0190941707, 978-0190941703