Answered step by step

Verified Expert Solution

Question

1 Approved Answer

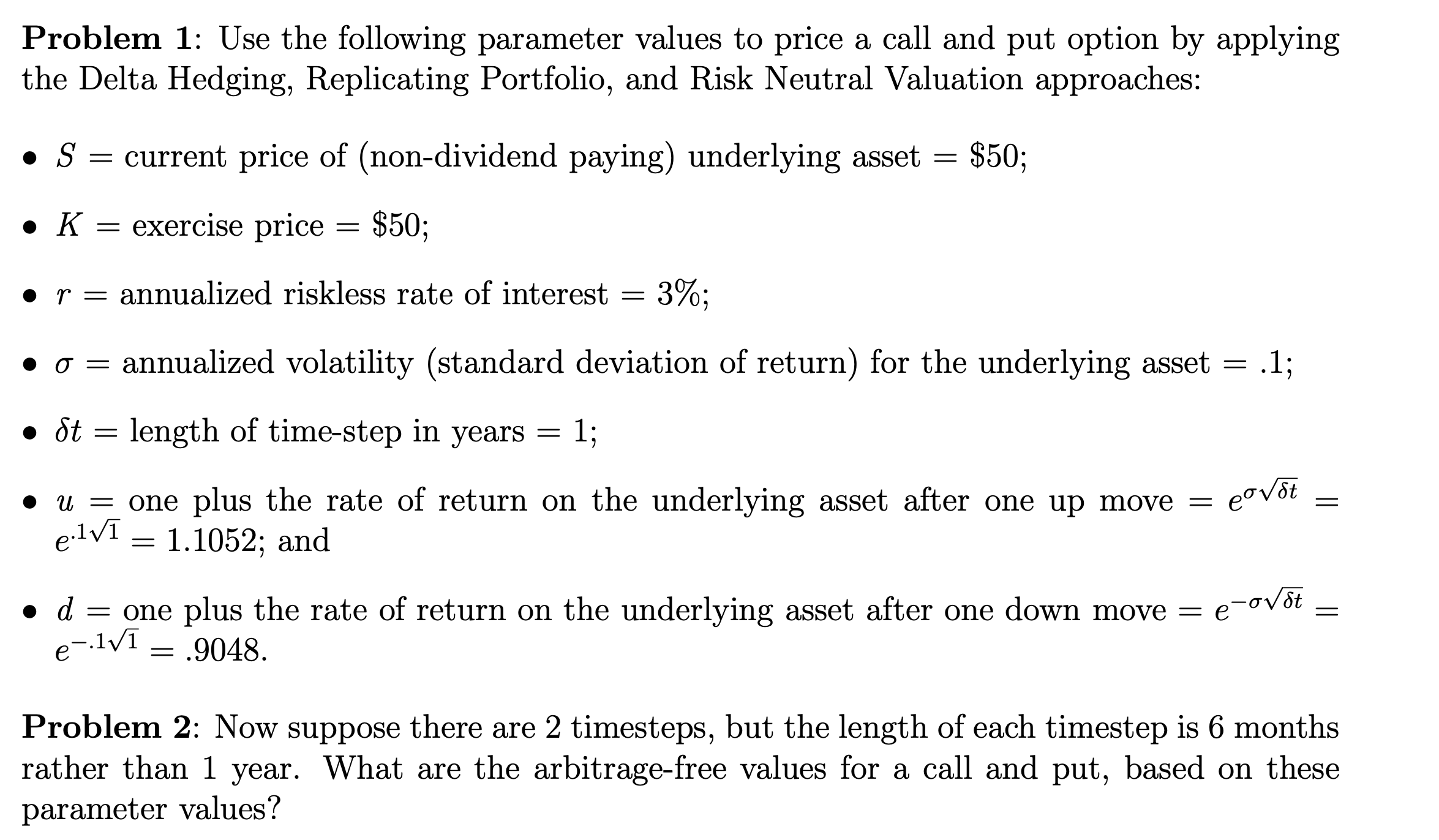

Problem 1 : Use the following parameter values to price a call and put option by applying the Delta Hedging, Replicating Portfolio, and Risk Neutral

Problem : Use the following parameter values to price a call and put option by applying

the Delta Hedging, Replicating Portfolio, and Risk Neutral Valuation approaches:

current price of nondividend paying underlying asset $;

exercise price $;

annualized riskless rate of interest ;

annualized volatility standard deviation of return for the underlying asset ;

length of timestep in years ;

one plus the rate of return on the underlying asset after one up move

; and

one plus the rate of return on the underlying asset after one down move

Problem : Now suppose there are timesteps, but the length of each timestep is months

rather than year. What are the arbitragefree values for a call and put, based on these

parameter values?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The ImpactAssets Handbook For Investors

Authors: Jed Emerson

1st Edition

1783087293, 978-1783087297