Answered step by step

Verified Expert Solution

Question

1 Approved Answer

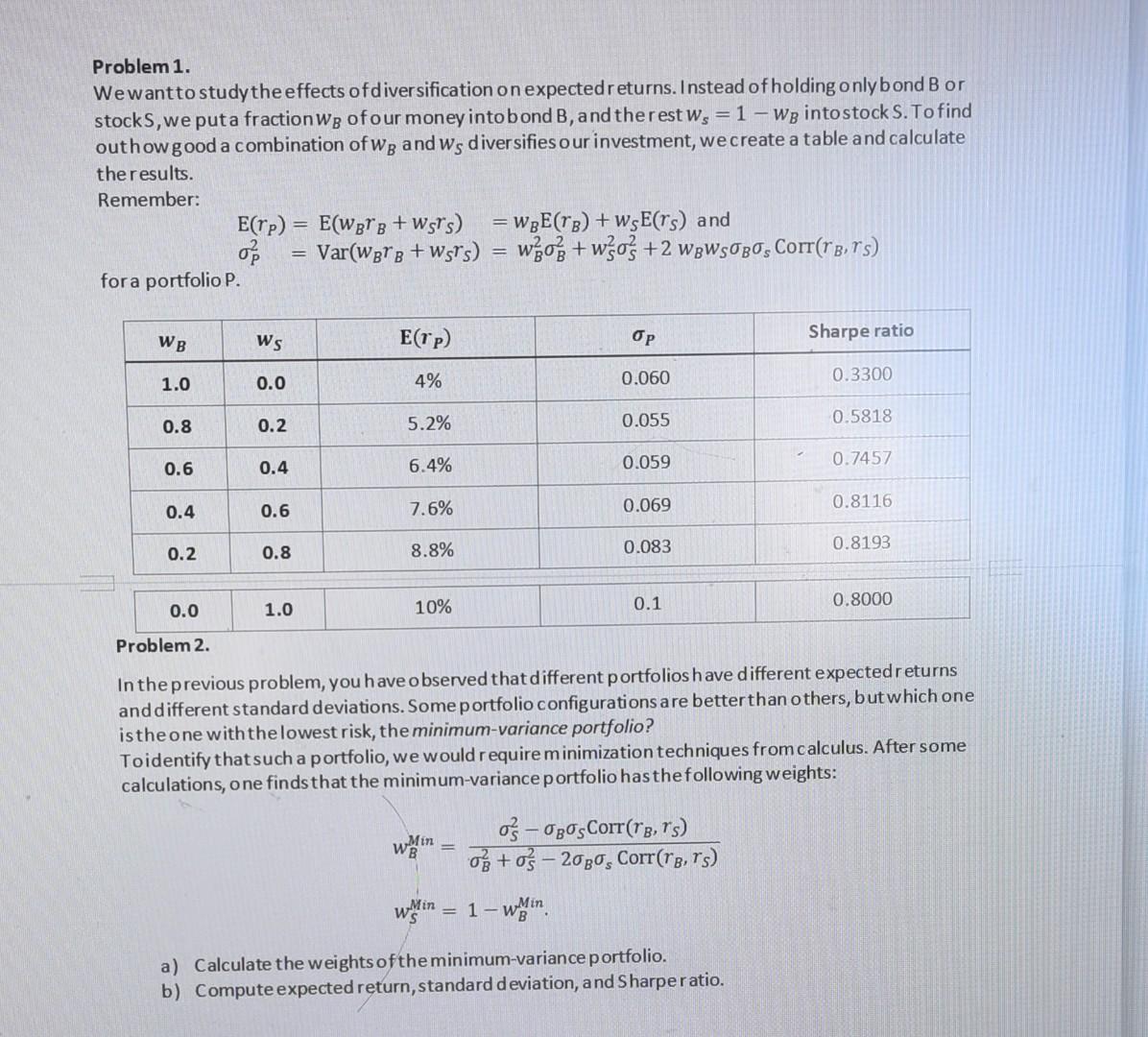

Problem 1. Wewant to study the effects ofdiversification on expected returns. Instead of holding only b ond B or stockS, we puta fraction wB of

Problem 1. Wewant to study the effects ofdiversification on expected returns. Instead of holding only b ond B or stockS, we puta fraction wB of our money intobond B, and the rest ws=1wB intostock S. To find outhow good a combination of wB and wS diver sifiesour investment, we create a table and calculate theresults. Remember: E(rP)=E(wBrB+wSrS)=wBE(rB)+wSE(rS)andP2=Var(wBrB+wSrS)=wB2B2+wS2S2+2wBwSBSCorr(rB,rS) for a portfolio P. Problem 2. In the previous problem, you have observed that different portfoliosh ave different expected returns and different standard deviations. Some portfolio configurations are better than others, but which one is the one with the lowest risk, the minimum-variance portfolio? Toidentify that such a portfolio, we would r equire minimization techniques from calculus. After some calculations, one finds that the minimum-variance portfolio has the following weights: wBMin=B2+S22BsCorr(rB,rS)S2BSCorr(rB,rS)wSMin=1wBMin. a) Calculate the weights of the minimum-variance portfolio. b) Compute expected return, standard deviation, and Sharpe ratio. Problem 1. Wewant to study the effects ofdiversification on expected returns. Instead of holding only b ond B or stockS, we puta fraction wB of our money intobond B, and the rest ws=1wB intostock S. To find outhow good a combination of wB and wS diver sifiesour investment, we create a table and calculate theresults. Remember: E(rP)=E(wBrB+wSrS)=wBE(rB)+wSE(rS)andP2=Var(wBrB+wSrS)=wB2B2+wS2S2+2wBwSBSCorr(rB,rS) for a portfolio P. Problem 2. In the previous problem, you have observed that different portfoliosh ave different expected returns and different standard deviations. Some portfolio configurations are better than others, but which one is the one with the lowest risk, the minimum-variance portfolio? Toidentify that such a portfolio, we would r equire minimization techniques from calculus. After some calculations, one finds that the minimum-variance portfolio has the following weights: wBMin=B2+S22BsCorr(rB,rS)S2BSCorr(rB,rS)wSMin=1wBMin. a) Calculate the weights of the minimum-variance portfolio. b) Compute expected return, standard deviation, and Sharpe ratio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Research Methods And Applications In Empirical Finance

Authors: Adrian R. Bell, Chris Brooks, Marcel Prokopczuk

1st Edition

1782540172, 978-1782540175