Answered step by step

Verified Expert Solution

Question

1 Approved Answer

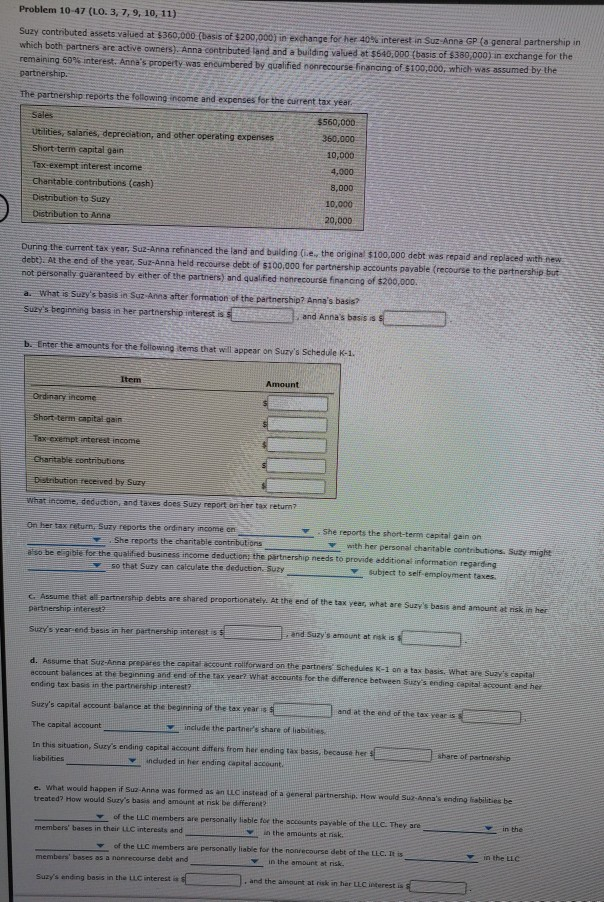

Problem 10-47 (10.3, 7, 9, 10, 11) Suzy contributed assets valued at $360,000 (basis of $200,000) in exchange for her 40% interest in Sur Anna

Problem 10-47 (10.3, 7, 9, 10, 11) Suzy contributed assets valued at $360,000 (basis of $200,000) in exchange for her 40% interest in Sur Anna GP (a general partnership in which both partners are active owners). Anna contributed land and building valued at $540,000 (basis of $380,000) in exchange for the remaining 60% interest. Anne's property was encumbered by qualified nonrecourse financing of $100,000, which was assumed by the partnership The partnership reports the following income and expenses for the current tax year Sales Utilities, salanes, depreciation, and other operating expenses Short term capital gain I exempt interest income $560,000 360,000 10,000 4.000 8,000 10,000 20,000 Chantable contributions (cash) Distribution to Suzy Distribution to Anna During the current tax year, Sut-Anna refinanced the land and building (ie, the original $100.000 debt was repaid and replaced with new debt). At the end of the year, Suz-Anna held recourse debt of 5100,000 for partnership accounts payable (recourse to the partnership but not personally guaranteed by either of the partners) and qualified nonrecourse financing of $200,000. a. What is Suzy's basis in SuzAnna after formation of the partnership? Anna's basis? Suzy's beginning bass in her partnership interest is l and Anna's besis is b. Enter the amounts for the following items that will appear on Sury's Schedule K-1. Short-term capital gain Tax Exempt interest income Charitable contributions tribution received by Suzy West income deduction, and taxes does Sury report on her tax return? O bertax return, Suty reports the ordinary income on . She reports the short-term capital gain on She reports the charitable contributions with her personal charitable contributions Suity might so be egible for the qualified business come deduction, the partnership needs to provide additional information regarding so that Suzy can calculate the deduction Suzy subject to self employment taxes Assume that all partnership debts are shared proportionately. At the end of the tax year, what are Suzy's basis and amount at risk in her partnership interest Suzy's year-end besis in her pastnership interest is de and Suzy's amount at niskis d. Assume that Suzna prepares the capital account riforward on the partners Schedules K-1 on a tax basis. What are Suzy's capital account balances at the beginning and end of the tax year? What accounts for the difference between Suzy's ending capital count and her ending tax bass in the partnership interest? Sury's capital account balance at the beginning of the tax years and at the end of the tax year is The capital account include the partner's share of liabilities In this situation, Sury's ending capital account differs from her ending Tax basis, because her share of partnership liabilities included in her ending capital account. e. What would happen if Suzanne was formed as an LLC instead of a general partnersho. How would su. Anna's ending liabilities bei treated? How would sury's basis and amount at nak be different of the LLC members are personally able for the accounts payable of the LLC. They are members' bases in their interests and in the amounts at risk. in the of the LLC members are personally liable for the mondecourse debt of the LLC. It is members bases as a novecourse debt and in the amount at ns. Sury's anding basis in the interest i C . and the amount at risk in her LLC interest Problem 10-47 (10.3, 7, 9, 10, 11) Suzy contributed assets valued at $360,000 (basis of $200,000) in exchange for her 40% interest in Sur Anna GP (a general partnership in which both partners are active owners). Anna contributed land and building valued at $540,000 (basis of $380,000) in exchange for the remaining 60% interest. Anne's property was encumbered by qualified nonrecourse financing of $100,000, which was assumed by the partnership The partnership reports the following income and expenses for the current tax year Sales Utilities, salanes, depreciation, and other operating expenses Short term capital gain I exempt interest income $560,000 360,000 10,000 4.000 8,000 10,000 20,000 Chantable contributions (cash) Distribution to Suzy Distribution to Anna During the current tax year, Sut-Anna refinanced the land and building (ie, the original $100.000 debt was repaid and replaced with new debt). At the end of the year, Suz-Anna held recourse debt of 5100,000 for partnership accounts payable (recourse to the partnership but not personally guaranteed by either of the partners) and qualified nonrecourse financing of $200,000. a. What is Suzy's basis in SuzAnna after formation of the partnership? Anna's basis? Suzy's beginning bass in her partnership interest is l and Anna's besis is b. Enter the amounts for the following items that will appear on Sury's Schedule K-1. Short-term capital gain Tax Exempt interest income Charitable contributions tribution received by Suzy West income deduction, and taxes does Sury report on her tax return? O bertax return, Suty reports the ordinary income on . She reports the short-term capital gain on She reports the charitable contributions with her personal charitable contributions Suity might so be egible for the qualified business come deduction, the partnership needs to provide additional information regarding so that Suzy can calculate the deduction Suzy subject to self employment taxes Assume that all partnership debts are shared proportionately. At the end of the tax year, what are Suzy's basis and amount at risk in her partnership interest Suzy's year-end besis in her pastnership interest is de and Suzy's amount at niskis d. Assume that Suzna prepares the capital account riforward on the partners Schedules K-1 on a tax basis. What are Suzy's capital account balances at the beginning and end of the tax year? What accounts for the difference between Suzy's ending capital count and her ending tax bass in the partnership interest? Sury's capital account balance at the beginning of the tax years and at the end of the tax year is The capital account include the partner's share of liabilities In this situation, Sury's ending capital account differs from her ending Tax basis, because her share of partnership liabilities included in her ending capital account. e. What would happen if Suzanne was formed as an LLC instead of a general partnersho. How would su. Anna's ending liabilities bei treated? How would sury's basis and amount at nak be different of the LLC members are personally able for the accounts payable of the LLC. They are members' bases in their interests and in the amounts at risk. in the of the LLC members are personally liable for the mondecourse debt of the LLC. It is members bases as a novecourse debt and in the amount at ns. Sury's anding basis in the interest i C . and the amount at risk in her LLC interest

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Connect For Computer Accounting With Quickbooks 2021

Authors: Author

20th Edition

1264069200, 9781264069200