Problem 11- 61 from 2021 book Prepare 2020 return without software usage. Just download the forms from irs.gov and fill them.

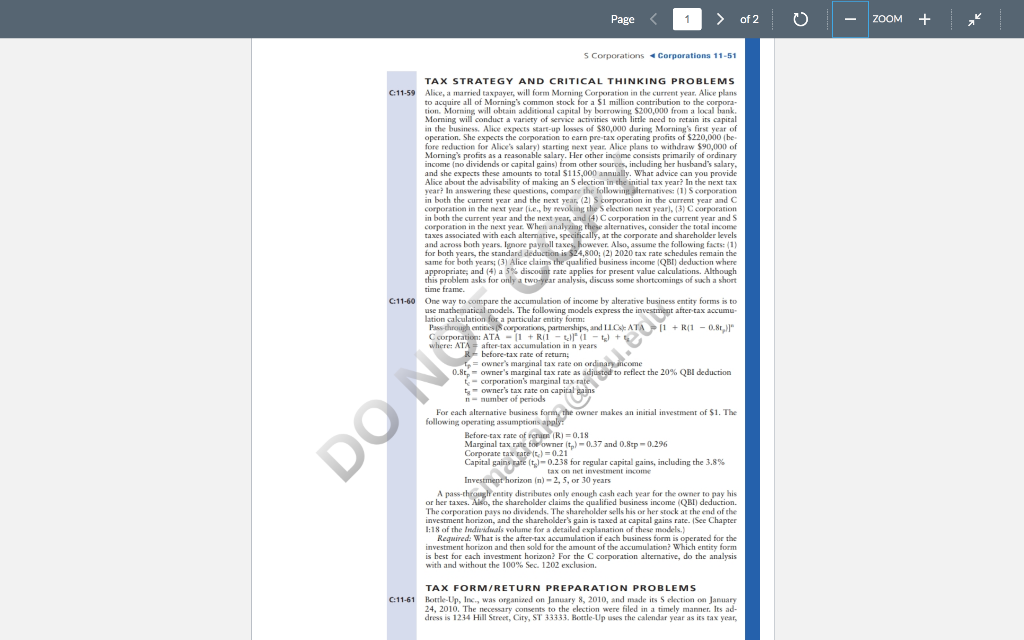

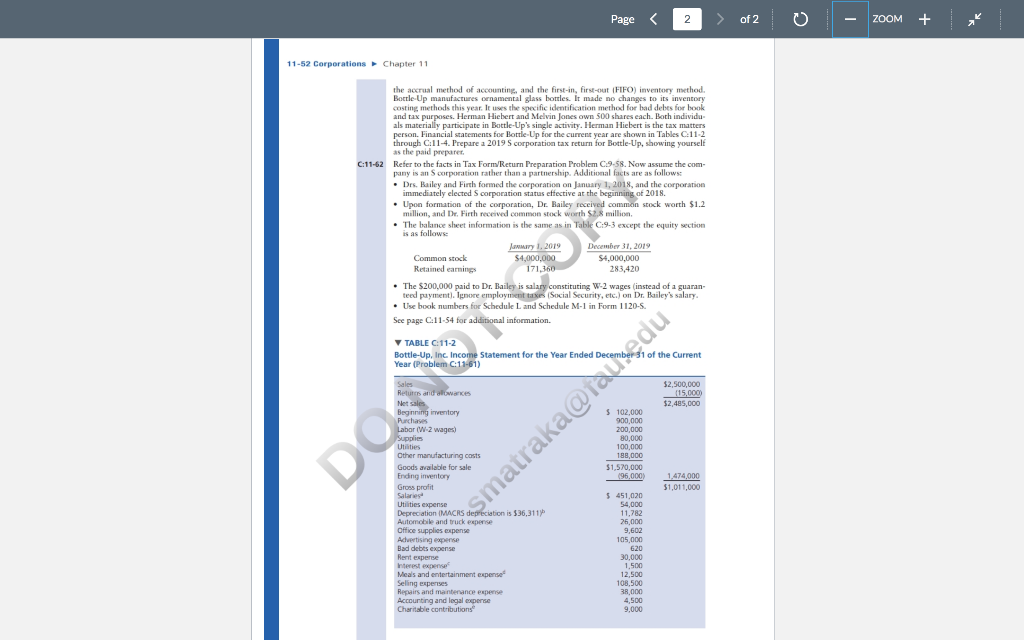

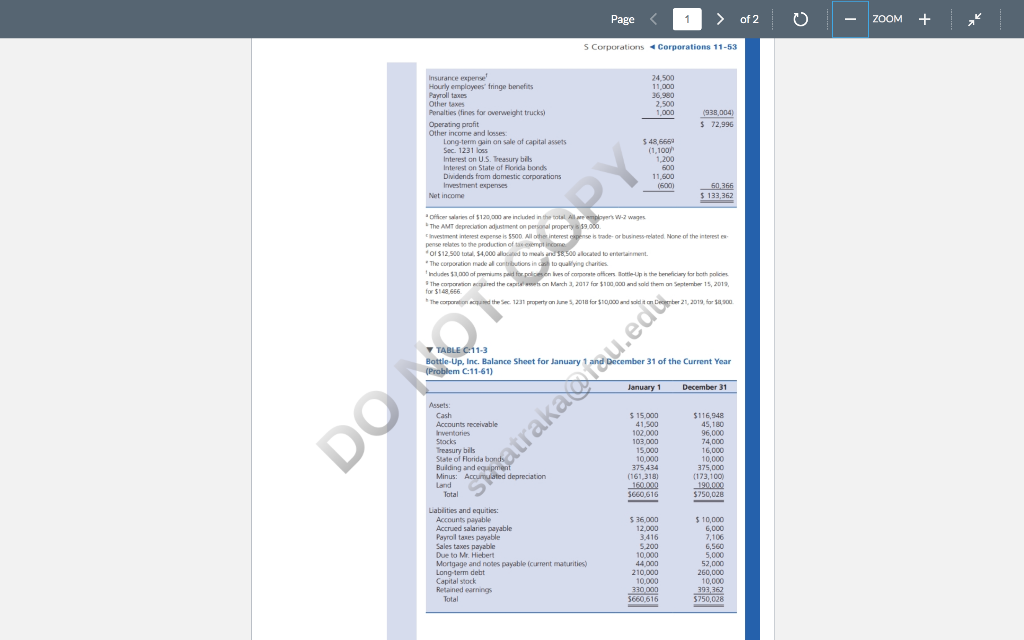

Page 1 > of 2 0 ZOOM + s Corporations Corporations 11-51 TAX STRATEGY AND CRITICAL THINKING PROBLEMS C11-59 Alice, a married taxpayer, will form Morning Corporation in the current year. Alice plans to acquire all of Morning's common stock for a $1 million contribution to the corpora- tion. Morning will obtain additional capital by borrowing $200,000 from a local bank Morning will conduct a variety of service activities with little need to retain its capital in the business. Alice expects start-up losses of $80,000 during Mornings first year of operation. She expects the corporation to earn pre-tax operating profits of $220,000 be fore reduction for Alice's salary) starting next year. Alice plans to withdraw $90,000 of Morning's profits as a reasonable salary. Her other income consists primarily of ordinary income no dividends or capital gains) from other sources, including her husband's salary, and she expects these amounts to total $115,000 annually. What advice can you provide Alice about the advisability of making an Selection in the initial tax year? In the next tax year? In answering these questions, compare the following alternatives: (1) Scorporation in both the current year and the next year, (2) Scorporation in the current year and C corporation in the next year ie, by revoking the selection next year), (3) corporation in both the current year and the next year, and (4) corporation in the current year and corporation in the next year. When analyzing these alternatives, consider the total income taxes associated with each alternative, specifically, at the corporate and shareholder levels and across bach years. Ignore payroll taxes, however. Also, assume the following facts: (1) for both years, the standard deduction is $24,800, (2) 2020 tax rate schedules remain the same for both years: (3) Alice daims the qualified business income (QBT) deduction where appropriate; and (4) a 5% discount rate applies for present value calculations. Although this problem asks for only a two-year analysis, discuss some shortcomings of such a short a -, time frame. C11-60 One way to compare the accumulation of income by alterative business entity forms is to use mathematical models. The following models express the investment after-tax accumu- Pass through entines corporaties, partnerships, and Il.CAT , , 11 + R/1 -0.8.)" R/1 , corporation: ATA - 11 + RI - - + where: ATA = after-tax accumulation in n years - R-before-tax rate of return; L = owner's marginal tax rate on ordinary income 0.8t - owner's marginal tax rate as adjusted to reflect the 20% QBI deduction - corporation's marginal tax rate - owner's tax rate on capital gains n-number of periods - For each alternative business form, the owner makes an initial investment of $1. The following operating assumptions poly Before tax rate of raon R) = 0.18 Marginal tax rate for ownert) -0.37 and 0.8tp -0.296 Corporate tax rate it. ) - 0.21 Capital gains ratet,-0.238 for regular capital gains, including the 3.8% tax on net investment income Investment horizon (n) -2,5, or 30 years A pass-throughentity distributes only enough cash each year for the owner to pay his or her taxes. Also, the shareholder claims the qualified business income (QBI) deduction. The corporation pays no dividends. The shareholder sells his or her stock at the end of the investment horizon, and the shareholder's gain is taxed at capital gains rate. See Chapter 1:18 of the Indianiduals volume for a detailed explanation of these models.) Required. What is the after tax accumulation if each business form is operated for the investment horizon and then sold for the amount of the accumulation which entity form is best for each investment horizon? For the corporation alternative, do the analysis with and without the 100% Sec. 1202 exclusion. ON OG he Mas eu TAX FORM/RETURN PREPARATION PROBLEMS C11-61 Bottle-Up, Inc., was organized on January 8, 2010, and made its Selection on January 24, 2010. The necessary consent to the election were filed in a timely manner. Its ad- dress is 1234 Hill Street, City, ST 33333. Hottle-Up uses the calendar year as its tax year, Page of 2 0 ZOOM + 11-52 Corporations Chapter 11 the accrual method of accounting, and the first-in, first-out (FIFO) inventory method. Bottle-Up manufactures ornamental glass bottles. It made no changes to its inventory costing methods this year. It uses the specific identification method for bad debts for book and tax purposes. Herman Hiebert and Melvin Jones own 500 shares each. Both individu als materially participate in Bottle-Up's single activity. Herman Hiebert is the tax matters person. Financial statements for Bottle-Lip for the current year are shown in Tables C.11-2 through C:11-4. Prepare a 2019 S corporation tax return for Bottle-Up, showing yourself as the paid prepare C:11-62 Refer to the facts in Tax Form Return Preparation Problem C9-58. Now assume the com- pany is an corporation rather than a partnership. Additional facts are as follows Drs. Bailey and Firth formed the corporation on January 1, 2018, and the corporation immediately elected Scorporation status effective at the beginning of 2018. . Upon formation of the corporation, De Bailey received common stock worth $1.2 million, and Dr. Firth received common stock worth $2.8 million The balance sheet information is the same as in Table C:9-3 except the equity section is as follows Janary 1, 2019 December 31, 2019 Common stock $4,000,000 $4,000,000 Retained earnings 171,360 283,420 The $200,000 paid to Dr. Bailey is salary constituting W-2 wages (instead of a guaran teed payment). Ignore employment taxes Social Security, etc.) on Dr. Bailey's salary. Use book numbers for Schedule Land Schedule M-1 in Form 1120-. See page C:11.54 for additional information. TABLE C:11-2 Bottle-Up, Inc Income Statement for the Year Ended December 31 of the Current Year (Problem C:11-61) $2,500,000 115,000 $2,485,000 DO Sales Returns and allowances Net sales Beginning inventory Purchases Labor (W-2 wages) Supplies Utilities Other manufacturing costs Goods available for sale Ending inventory Gross profit Salaries Utilities expense Depreciation (MACRS depreciation is 536,311 Automobile and truck expense Office supplies expense Advertising expense Bad debts expense $ 102,000 900,000 200,000 80,000 100,000 188,000 $1,570,000 (96.000 smatraka@rauldu 1,474,000 $1,011,000 Rent espere $ 451,020 54,000 11,782 25,000 9,602 105,000 620 30,000 1,500 12,500 108,500 38.000 4,500 9,000 Meals and entertainment expense Selling expenses Repairs and maintenance expense Accounting and legal expense Charitable contribution > of 2 0 - ZOOM + s Corporations Corporation Naation January 1 December 31 DO matrakalau.edu Page of 2 0 ZOOM + 11-54 Corporations Chapter 11 TABLE C11-4 Bottle-Up, Inc Statement of Change in Retained Earnings, for the Current Year Ended December 31 (Problem C11-61) $330,000 Balance, January 1 Plus. Net income Minus: Dividends $133.362 (70.000 53,362 Balance, December 31 3393,362 *The January 1 accumulated adjustments account balance is $274300 Required: Prepare the 2019 S corporation tax return Form 1120-5), including the fol- lowing additional schedules and forme: Schedule D, Form 4562, and Schedule K 1. Optional: (1) Complete Schedule M-2 in Form 1120 5 even though the company never been a corporation. For this purpose, the accumulated adjustments account at the beginning of 2019 is $171,360. (2) Prepare a schedule for each shareholder's basis in his or her corporation stock. For this purpose, Hailey's stock basis at the beginning of 2019 is $1,251,468 and Firth's is $2,535,952 C11-63 Short Tex Form. Refer to the facts in Problem C:11-36, and prepare Form 1120-5, Schedule K based on these facts. su CASE STUDY PROBLEM 6:11-64 Debra has operated a family counseling practice for a number of years as a sole proprietor, She owns the condominium office space that she occupies in addition to her professional library and office furniture. She has a limited amount of working capital and little need to accumulate additional business assets. Her total business acts are about $150,000, with an $80,000 mortgage on the office space being her only liability. Typically, she has withdrawn any unneeded assets at the end of the year. Tebra las used her personal car for business travel and charged the business for the mileage at the appropriate mileage rate provided by the IRS. Over the last three years, Debral practice has grown so that she now forecasts $80,000 of income being earned this year. Debra has contributed small amounts to an Individual Retirement Account (RA) each you, but her contributions have never reached the annual limits. Although she has never been sued, Debra recently has become concerned about legal liability. An attomey friend of hers has suggested that she incorpo- rate her business to protect herself against being sued and to save taxes. Required: You are a good friend of Debrals and a CPA; she asks your opinion on incorpo- . rating her business. You are to meet with Dehra tomorrow for lunch. Prepare a draft af the points you feel should be discussed over lunch about incorporating the family counsel- ing practice. DO ma TAX RESEARCH PROBLEMS C:11-65 Cato Corporation incorporated six years ago in California, with Tim and Elesa, husband and wife, owning all the Gato stock. Immediately thereafter, Cato made an Selection of fective for that year. Tim and Elesa filed the necessary consent to the election. On March 10 of last year, Tim and Elesa transferred 15% of the Cato stock to the Reid and Susan Trust, an irrevocable trust created three years earlier for the benefit of their two minor children. Early in the current year, Tim and Elesa's tax accountant learns about the trans- fer and advises the couple that the transfer of the stock to the trust may have terminated Cato's Selection. Prepare a memorandum for your tax manager indicating any action Tim and Elesa can take that will permit Cato to retain its Selection Research sources sug- gested by the tax manager include Secs. 1361(c)2), 13621d1(2), and 13621). Page 1 > of 2 0 ZOOM + s Corporations Corporations 11-51 TAX STRATEGY AND CRITICAL THINKING PROBLEMS C11-59 Alice, a married taxpayer, will form Morning Corporation in the current year. Alice plans to acquire all of Morning's common stock for a $1 million contribution to the corpora- tion. Morning will obtain additional capital by borrowing $200,000 from a local bank Morning will conduct a variety of service activities with little need to retain its capital in the business. Alice expects start-up losses of $80,000 during Mornings first year of operation. She expects the corporation to earn pre-tax operating profits of $220,000 be fore reduction for Alice's salary) starting next year. Alice plans to withdraw $90,000 of Morning's profits as a reasonable salary. Her other income consists primarily of ordinary income no dividends or capital gains) from other sources, including her husband's salary, and she expects these amounts to total $115,000 annually. What advice can you provide Alice about the advisability of making an Selection in the initial tax year? In the next tax year? In answering these questions, compare the following alternatives: (1) Scorporation in both the current year and the next year, (2) Scorporation in the current year and C corporation in the next year ie, by revoking the selection next year), (3) corporation in both the current year and the next year, and (4) corporation in the current year and corporation in the next year. When analyzing these alternatives, consider the total income taxes associated with each alternative, specifically, at the corporate and shareholder levels and across bach years. Ignore payroll taxes, however. Also, assume the following facts: (1) for both years, the standard deduction is $24,800, (2) 2020 tax rate schedules remain the same for both years: (3) Alice daims the qualified business income (QBT) deduction where appropriate; and (4) a 5% discount rate applies for present value calculations. Although this problem asks for only a two-year analysis, discuss some shortcomings of such a short a -, time frame. C11-60 One way to compare the accumulation of income by alterative business entity forms is to use mathematical models. The following models express the investment after-tax accumu- Pass through entines corporaties, partnerships, and Il.CAT , , 11 + R/1 -0.8.)" R/1 , corporation: ATA - 11 + RI - - + where: ATA = after-tax accumulation in n years - R-before-tax rate of return; L = owner's marginal tax rate on ordinary income 0.8t - owner's marginal tax rate as adjusted to reflect the 20% QBI deduction - corporation's marginal tax rate - owner's tax rate on capital gains n-number of periods - For each alternative business form, the owner makes an initial investment of $1. The following operating assumptions poly Before tax rate of raon R) = 0.18 Marginal tax rate for ownert) -0.37 and 0.8tp -0.296 Corporate tax rate it. ) - 0.21 Capital gains ratet,-0.238 for regular capital gains, including the 3.8% tax on net investment income Investment horizon (n) -2,5, or 30 years A pass-throughentity distributes only enough cash each year for the owner to pay his or her taxes. Also, the shareholder claims the qualified business income (QBI) deduction. The corporation pays no dividends. The shareholder sells his or her stock at the end of the investment horizon, and the shareholder's gain is taxed at capital gains rate. See Chapter 1:18 of the Indianiduals volume for a detailed explanation of these models.) Required. What is the after tax accumulation if each business form is operated for the investment horizon and then sold for the amount of the accumulation which entity form is best for each investment horizon? For the corporation alternative, do the analysis with and without the 100% Sec. 1202 exclusion. ON OG he Mas eu TAX FORM/RETURN PREPARATION PROBLEMS C11-61 Bottle-Up, Inc., was organized on January 8, 2010, and made its Selection on January 24, 2010. The necessary consent to the election were filed in a timely manner. Its ad- dress is 1234 Hill Street, City, ST 33333. Hottle-Up uses the calendar year as its tax year, Page of 2 0 ZOOM + 11-52 Corporations Chapter 11 the accrual method of accounting, and the first-in, first-out (FIFO) inventory method. Bottle-Up manufactures ornamental glass bottles. It made no changes to its inventory costing methods this year. It uses the specific identification method for bad debts for book and tax purposes. Herman Hiebert and Melvin Jones own 500 shares each. Both individu als materially participate in Bottle-Up's single activity. Herman Hiebert is the tax matters person. Financial statements for Bottle-Lip for the current year are shown in Tables C.11-2 through C:11-4. Prepare a 2019 S corporation tax return for Bottle-Up, showing yourself as the paid prepare C:11-62 Refer to the facts in Tax Form Return Preparation Problem C9-58. Now assume the com- pany is an corporation rather than a partnership. Additional facts are as follows Drs. Bailey and Firth formed the corporation on January 1, 2018, and the corporation immediately elected Scorporation status effective at the beginning of 2018. . Upon formation of the corporation, De Bailey received common stock worth $1.2 million, and Dr. Firth received common stock worth $2.8 million The balance sheet information is the same as in Table C:9-3 except the equity section is as follows Janary 1, 2019 December 31, 2019 Common stock $4,000,000 $4,000,000 Retained earnings 171,360 283,420 The $200,000 paid to Dr. Bailey is salary constituting W-2 wages (instead of a guaran teed payment). Ignore employment taxes Social Security, etc.) on Dr. Bailey's salary. Use book numbers for Schedule Land Schedule M-1 in Form 1120-. See page C:11.54 for additional information. TABLE C:11-2 Bottle-Up, Inc Income Statement for the Year Ended December 31 of the Current Year (Problem C:11-61) $2,500,000 115,000 $2,485,000 DO Sales Returns and allowances Net sales Beginning inventory Purchases Labor (W-2 wages) Supplies Utilities Other manufacturing costs Goods available for sale Ending inventory Gross profit Salaries Utilities expense Depreciation (MACRS depreciation is 536,311 Automobile and truck expense Office supplies expense Advertising expense Bad debts expense $ 102,000 900,000 200,000 80,000 100,000 188,000 $1,570,000 (96.000 smatraka@rauldu 1,474,000 $1,011,000 Rent espere $ 451,020 54,000 11,782 25,000 9,602 105,000 620 30,000 1,500 12,500 108,500 38.000 4,500 9,000 Meals and entertainment expense Selling expenses Repairs and maintenance expense Accounting and legal expense Charitable contribution > of 2 0 - ZOOM + s Corporations Corporation Naation January 1 December 31 DO matrakalau.edu Page of 2 0 ZOOM + 11-54 Corporations Chapter 11 TABLE C11-4 Bottle-Up, Inc Statement of Change in Retained Earnings, for the Current Year Ended December 31 (Problem C11-61) $330,000 Balance, January 1 Plus. Net income Minus: Dividends $133.362 (70.000 53,362 Balance, December 31 3393,362 *The January 1 accumulated adjustments account balance is $274300 Required: Prepare the 2019 S corporation tax return Form 1120-5), including the fol- lowing additional schedules and forme: Schedule D, Form 4562, and Schedule K 1. Optional: (1) Complete Schedule M-2 in Form 1120 5 even though the company never been a corporation. For this purpose, the accumulated adjustments account at the beginning of 2019 is $171,360. (2) Prepare a schedule for each shareholder's basis in his or her corporation stock. For this purpose, Hailey's stock basis at the beginning of 2019 is $1,251,468 and Firth's is $2,535,952 C11-63 Short Tex Form. Refer to the facts in Problem C:11-36, and prepare Form 1120-5, Schedule K based on these facts. su CASE STUDY PROBLEM 6:11-64 Debra has operated a family counseling practice for a number of years as a sole proprietor, She owns the condominium office space that she occupies in addition to her professional library and office furniture. She has a limited amount of working capital and little need to accumulate additional business assets. Her total business acts are about $150,000, with an $80,000 mortgage on the office space being her only liability. Typically, she has withdrawn any unneeded assets at the end of the year. Tebra las used her personal car for business travel and charged the business for the mileage at the appropriate mileage rate provided by the IRS. Over the last three years, Debral practice has grown so that she now forecasts $80,000 of income being earned this year. Debra has contributed small amounts to an Individual Retirement Account (RA) each you, but her contributions have never reached the annual limits. Although she has never been sued, Debra recently has become concerned about legal liability. An attomey friend of hers has suggested that she incorpo- rate her business to protect herself against being sued and to save taxes. Required: You are a good friend of Debrals and a CPA; she asks your opinion on incorpo- . rating her business. You are to meet with Dehra tomorrow for lunch. Prepare a draft af the points you feel should be discussed over lunch about incorporating the family counsel- ing practice. DO ma TAX RESEARCH PROBLEMS C:11-65 Cato Corporation incorporated six years ago in California, with Tim and Elesa, husband and wife, owning all the Gato stock. Immediately thereafter, Cato made an Selection of fective for that year. Tim and Elesa filed the necessary consent to the election. On March 10 of last year, Tim and Elesa transferred 15% of the Cato stock to the Reid and Susan Trust, an irrevocable trust created three years earlier for the benefit of their two minor children. Early in the current year, Tim and Elesa's tax accountant learns about the trans- fer and advises the couple that the transfer of the stock to the trust may have terminated Cato's Selection. Prepare a memorandum for your tax manager indicating any action Tim and Elesa can take that will permit Cato to retain its Selection Research sources sug- gested by the tax manager include Secs. 1361(c)2), 13621d1(2), and 13621)