Answered step by step

Verified Expert Solution

Question

1 Approved Answer

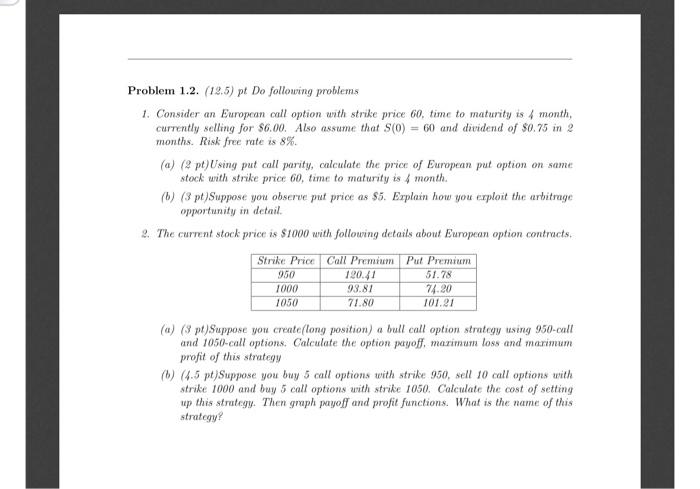

Problem 1.2. (12.5) pl Do following problems 1. Consider an European call option with strike price 60, time to maturity is month, currently selling for

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance And Accounting For High-Tech Companies

Authors: Frank J Fabozzi

1st Edition

0262336901, 9780262336901