Answered step by step

Verified Expert Solution

Question

1 Approved Answer

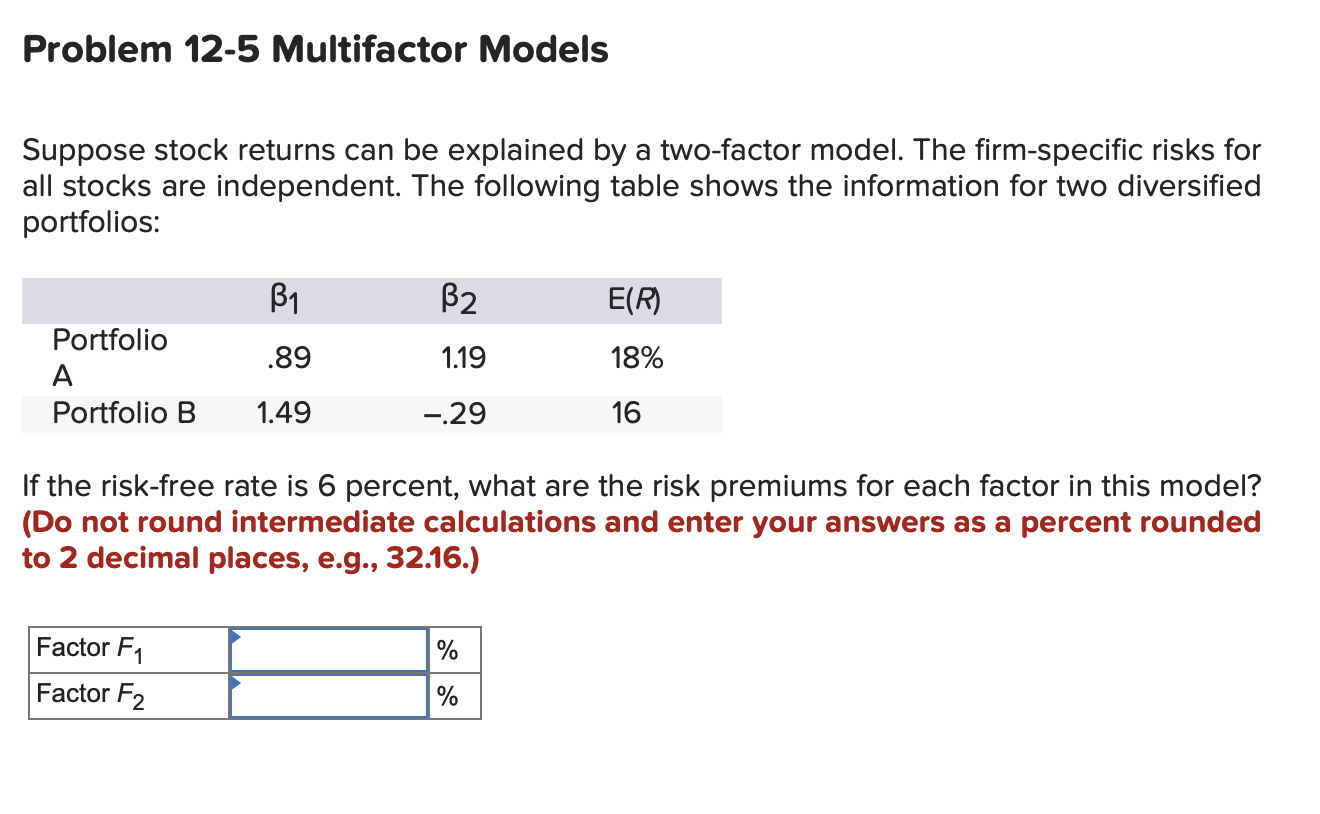

Problem 12-5 Multifactor Models Suppose stock returns can be explained by a two-factor model. The firm-specific risks for all stocks are independent. The following

Problem 12-5 Multifactor Models Suppose stock returns can be explained by a two-factor model. The firm-specific risks for all stocks are independent. The following table shows the information for two diversified portfolios: 1 2 E(R) Portfolio .89 1.19 18% A -.29 16 Portfolio B 1.49 If the risk-free rate is 6 percent, what are the risk premiums for each factor in this model? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) Factor F1 Factor F2 % %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Math

Authors: Cheryl Cleaves, Margie Hobbs, Jeffrey Noble

10th edition

133011208, 978-0321924308, 321924304, 978-0133011203