Answered step by step

Verified Expert Solution

Question

1 Approved Answer

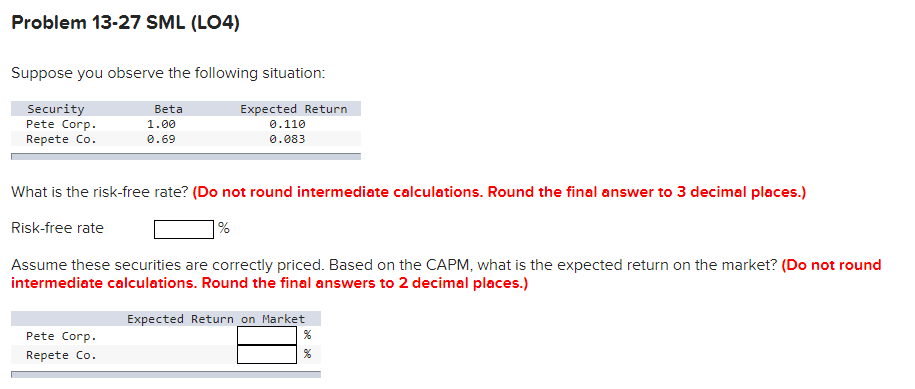

Problem 13-27 SML (LO4) Suppose you observe the following situation: Security Pete Corp. Repete Co. Beta 1.00 0.69 Expected Return 0.110 0.083 What is the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Hedge Funds

Authors: Douglas Cumming, Sofia Johan, Geoffrey Wood

1st Edition

0198840950, 978-0198840954