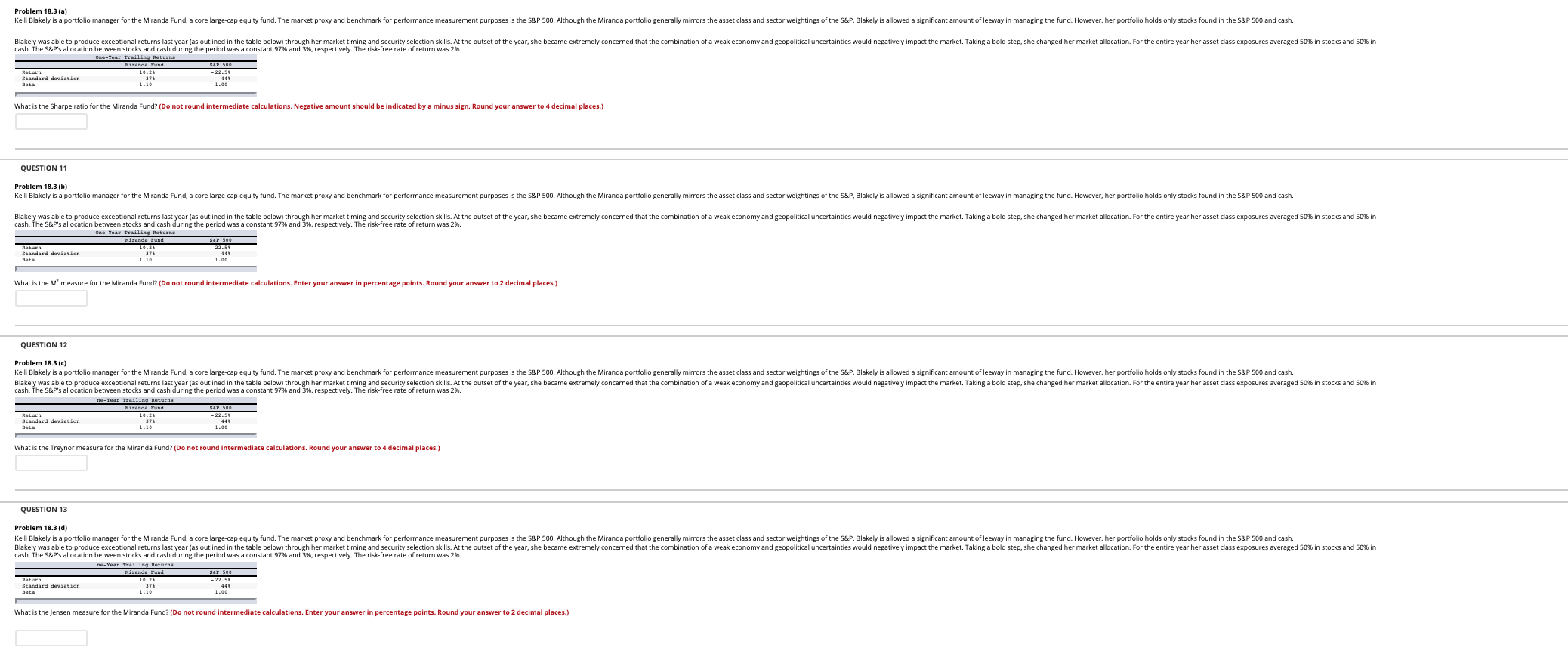

Problem 18.3 (a) Kelli Blakely is a portfolio Manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. One-Year Tralling Returns Miranda Pund Return 44 Beta SET 500 - 22.50 Standard deviation 374 1.10 What is the Sharpe ratio for the Miranda Fund? (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answer to 4 decimal places.) QUESTION 11 Problem 18.3 (b) Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset dass exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. One-Year Tralling Returns Miranda Pund SEP 500 Return Standard deviation 10.2 - 22.50 1.10 What is the measure for the Miranda Fund? (Do not round intermediate calculations. Enter your answer in percentage points. Round your answer to 2 decimal places.) QUESTION 12 Problem 18.3 (C) Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. ne-Year Tralli laturna Miranda Fund SEF 500 Return 10.21 - 22.5 Standard deviation 1.10 What is the Treynor measure for the Miranda Fund? (Do not round intermediate calculations. Round your answer to 4 decimal places.) QUESTION 13 Problem 18.3 (d) Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2% ne-Year Trailing Miranda Fund SET 500 10.26 Standard deviation Beta 1.10 1.00 What is the Jensen measure for the Miranda Fund? (Do not round intermediate calculations. Enter your answer in percentage points. Round your answer to 2 decimal places.) Problem 18.3 (a) Kelli Blakely is a portfolio Manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. One-Year Tralling Returns Miranda Pund Return 44 Beta SET 500 - 22.50 Standard deviation 374 1.10 What is the Sharpe ratio for the Miranda Fund? (Do not round intermediate calculations. Negative amount should be indicated by a minus sign. Round your answer to 4 decimal places.) QUESTION 11 Problem 18.3 (b) Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset dass exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. One-Year Tralling Returns Miranda Pund SEP 500 Return Standard deviation 10.2 - 22.50 1.10 What is the measure for the Miranda Fund? (Do not round intermediate calculations. Enter your answer in percentage points. Round your answer to 2 decimal places.) QUESTION 12 Problem 18.3 (C) Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2%. ne-Year Tralli laturna Miranda Fund SEF 500 Return 10.21 - 22.5 Standard deviation 1.10 What is the Treynor measure for the Miranda Fund? (Do not round intermediate calculations. Round your answer to 4 decimal places.) QUESTION 13 Problem 18.3 (d) Kelli Blakely is a portfolio manager for the Miranda Fund, a core large-cap equity fund. The market proxy and benchmark for performance measurement purposes is the S&P 500. Although the Miranda portfolio generally mirrors the asset class and sector weightings of the S&P, Blakely is allowed a significant amount of leeway in managing the fund. However, her portfolio holds only stocks found in the S&P 500 and cash. Blakely was able to produce exceptional returns last year (as outlined in the table below) through her market timing and security selection skills. At the outset of the year, she became extremely concerned that the combination of a weak economy and geopolitical uncertainties would negatively impact the market. Taking a bold step, she changed her market allocation. For the entire year her asset class exposures averaged 50% in stocks and 50% in cash. The S&P's allocation between stocks and cash during the period was a constant 97% and 3%, respectively. The risk-free rate of return was 2% ne-Year Trailing Miranda Fund SET 500 10.26 Standard deviation Beta 1.10 1.00 What is the Jensen measure for the Miranda Fund? (Do not round intermediate calculations. Enter your answer in percentage points. Round your answer to 2 decimal places.)