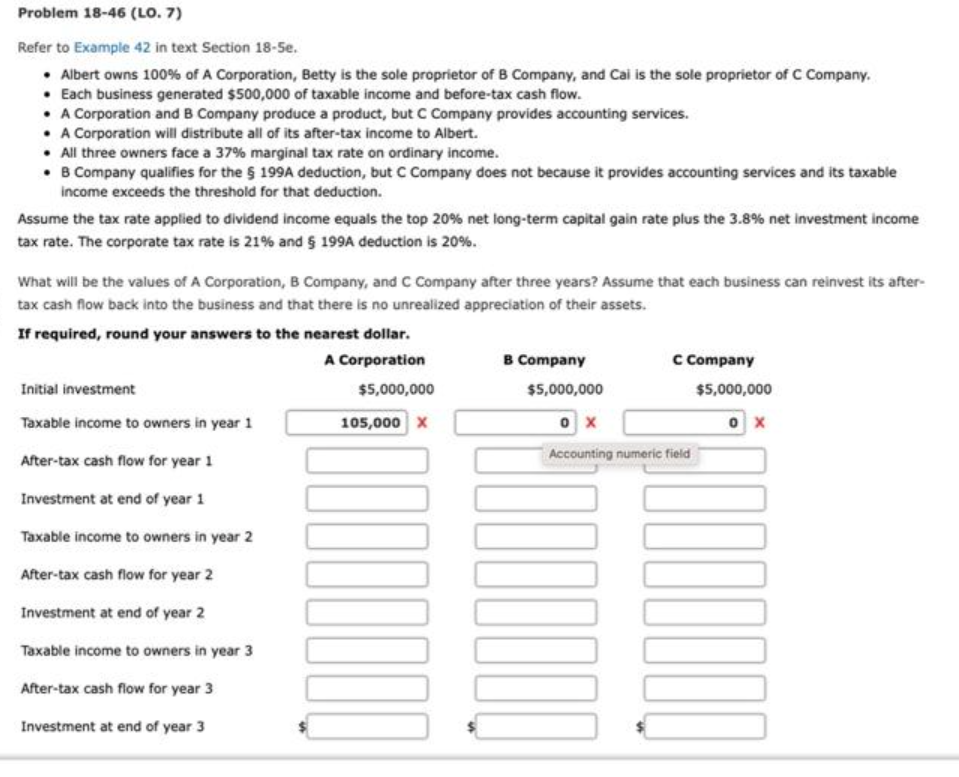

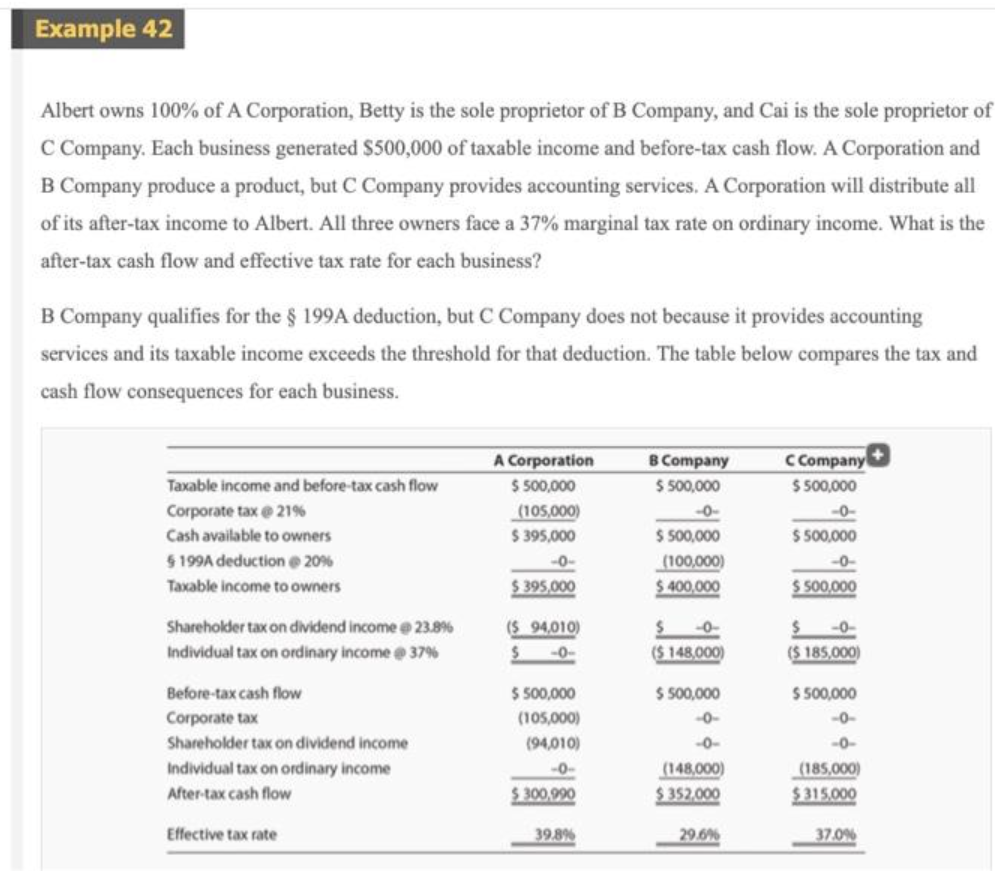

Problem 18-46 (LO. 7) Refer to Example 42 in text Section 18-5e. Albert owns 100% of A Corporation, Betty is the sole proprietor of B Company, and Cai is the sole proprietor of C Company. Each business generated $500,000 of taxable income and before-tax cash flow. A Corporation and B Company produce a product, but c Company provides accounting services. A Corporation will distribute all of its after-tax income to Albert. All three owners face a 37% marginal tax rate on ordinary income. B Company qualifies for the $ 199A deduction, but c Company does not because it provides accounting services and its taxable income exceeds the threshold for that deduction. Assume the tax rate applied to dividend income equals the top 20% net long-term capital gain rate plus the 3.8% net investment income tax rate. The corporate tax rate is 21% and $ 199A deduction is 20%. What will be the values of A Corporation, B Company, and C Company after three years? Assume that each business can reinvest its after- tax cash flow back into the business and that there is no unrealized appreciation of their assets. If required, round your answers to the nearest dollar. A Corporation B Company c Company Initial investment $5,000,000 $5,000,000 $5,000,000 Taxable income to owners in year 1 105,000 x 0 x After-tax cash flow for year 1 Accounting numeric field Investment at end of year 1 Taxable income to owners in year 2 After-tax cash flow for year 2 Investment at end of year 2 ILLIMITI Taxable income to owners in year 3 After-tax cash flow for year 3 Investment at end of year 3 KI Example 42 Albert owns 100% of A Corporation, Betty is the sole proprietor of B Company, and Cai is the sole proprietor of C Company. Each business generated $500,000 of taxable income and before-tax cash flow. A Corporation and B Company produce a product, but C Company provides accounting services, A Corporation will distribute all of its after-tax income to Albert. All three owners face a 37% marginal tax rate on ordinary income. What is the after-tax cash flow and effective tax rate for each business? B Company qualifies for the $ 199A deduction, but c Company does not because it provides accounting services and its taxable income exceeds the threshold for that deduction. The table below compares the tax and cash flow consequences for each business. B Company $ 500,000 A Corporation $ 500,000 (105,000) $395.000 C Company $ 500,000 -0- $ 500,000 -0- $ 500.000 $ 500,000 (100,000) $ 400,000 $ 395,000 Taxable income and before tax cash flow Corporate tax 21% Cash available to owners 6 199A deduction 20% Taxable income to owners Shareholder tax on dividend income 23.8% Individual tax on ordinary income 37% Before-tax cash flow Corporate tax Shareholder tax on dividend income Individual tax on ordinary income After-tax cash flow (5 94,010 $ -0- $ ($ 148,000) $ (5 185,000) $ 500,000 (105,000) 194,010) -0- $300,990 $ 500,000 0- -0- (148,000) $ 352.000 S 500,000 -0- -0- (185,000) $315.000 Effective tax rate 39.89 29.6% 3709 Problem 18-46 (LO. 7) Refer to Example 42 in text Section 18-5e. Albert owns 100% of A Corporation, Betty is the sole proprietor of B Company, and Cai is the sole proprietor of C Company. Each business generated $500,000 of taxable income and before-tax cash flow. A Corporation and B Company produce a product, but c Company provides accounting services. A Corporation will distribute all of its after-tax income to Albert. All three owners face a 37% marginal tax rate on ordinary income. B Company qualifies for the $ 199A deduction, but c Company does not because it provides accounting services and its taxable income exceeds the threshold for that deduction. Assume the tax rate applied to dividend income equals the top 20% net long-term capital gain rate plus the 3.8% net investment income tax rate. The corporate tax rate is 21% and $ 199A deduction is 20%. What will be the values of A Corporation, B Company, and C Company after three years? Assume that each business can reinvest its after- tax cash flow back into the business and that there is no unrealized appreciation of their assets. If required, round your answers to the nearest dollar. A Corporation B Company c Company Initial investment $5,000,000 $5,000,000 $5,000,000 Taxable income to owners in year 1 105,000 x 0 x After-tax cash flow for year 1 Accounting numeric field Investment at end of year 1 Taxable income to owners in year 2 After-tax cash flow for year 2 Investment at end of year 2 ILLIMITI Taxable income to owners in year 3 After-tax cash flow for year 3 Investment at end of year 3 KI Example 42 Albert owns 100% of A Corporation, Betty is the sole proprietor of B Company, and Cai is the sole proprietor of C Company. Each business generated $500,000 of taxable income and before-tax cash flow. A Corporation and B Company produce a product, but C Company provides accounting services, A Corporation will distribute all of its after-tax income to Albert. All three owners face a 37% marginal tax rate on ordinary income. What is the after-tax cash flow and effective tax rate for each business? B Company qualifies for the $ 199A deduction, but c Company does not because it provides accounting services and its taxable income exceeds the threshold for that deduction. The table below compares the tax and cash flow consequences for each business. B Company $ 500,000 A Corporation $ 500,000 (105,000) $395.000 C Company $ 500,000 -0- $ 500,000 -0- $ 500.000 $ 500,000 (100,000) $ 400,000 $ 395,000 Taxable income and before tax cash flow Corporate tax 21% Cash available to owners 6 199A deduction 20% Taxable income to owners Shareholder tax on dividend income 23.8% Individual tax on ordinary income 37% Before-tax cash flow Corporate tax Shareholder tax on dividend income Individual tax on ordinary income After-tax cash flow (5 94,010 $ -0- $ ($ 148,000) $ (5 185,000) $ 500,000 (105,000) 194,010) -0- $300,990 $ 500,000 0- -0- (148,000) $ 352.000 S 500,000 -0- -0- (185,000) $315.000 Effective tax rate 39.89 29.6% 3709