Question

Problem 18-61 (Static) Contribution Income Statement for Profit Centers [LO 18-3] Skip to question [The following information applies to the questions displayed below.] Cardio World

Problem 18-61 (Static) Contribution Income Statement for Profit Centers [LO 18-3]

Skip to question

[The following information applies to the questions displayed below.]

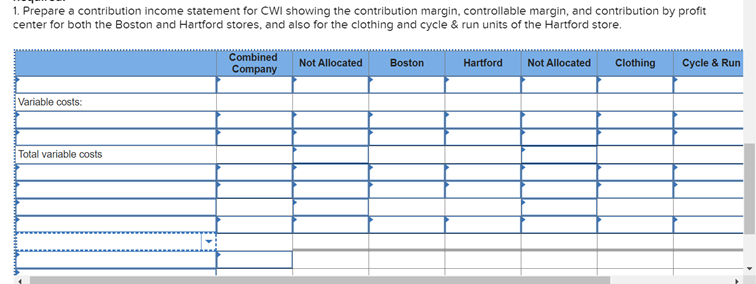

Cardio World Incorporated (CWI) is a sporting goods retailer that specializes in bicycles, running shoes, and related clothing. The firm has become successful by careful attention to trends in cycling, running, and changes in the technology and fashion of sport clothing. In recent years, however, the profit margins have begun to fall, and CWI has decided to employ a contribution income statement to further analyze the companys profitability. The company has two stores, one in Hartford, Connecticut, and the other in Boston, Massachusetts. The total sales for the two stores for the most recent year are $7,025,000 and $5,875,000 for the Hartford and Boston stores, respectively. Both stores are considered profit centers, and within each store are two profit centers: one for clothing and the other for cycle and running shoes (called "cycle & run" below). The breakdown of sales within the two stores is approximately 50% clothing and 50% cycle & run for Boston but is estimated to be 60%/40% for Hartford due to the greater interest in cycling in the Boston area. CWI is interested in finding the profit contribution of clothing and cycle & run at the Hartford store but not at the Boston store.

Cost of purchases for resale averages 60% of retail value at Boston; at Hartford, the cost is 70% for clothing and 50% for cycle & run. Variable operating costs at each store are similar: 30% of retail sales at Boston, and at Hartford, variable operating costs are 25% of retail sales for the clothing unit and 35% for the cycle & run unit. CWI estimates it has a total of $1,175,000 fixed cost, of which $325,000 cannot be traced to either store; of the remaining $850,000, $475,000 is traceable to the stores and controllable by store managers, and $375,000 can be traced to the stores but cannot be controlled in the short term by the store managers. These fixed costs are estimated to be traceable to the stores as follows:

| Fixed Controllable Costs | Percent of Total Cost |

|---|---|

| Boston | 45% |

| Hartford total | 45 |

| Clothing | 50 |

| Cycle & run | 30 |

| Could not be traced to clothing or cycling at Hartford | 20 |

| Could not be traced to Boston or Hartford | 10 |

| Fixed Noncontrollable Costs | Percent of Total Cost |

|---|---|

| Boston | 40% |

| Hartford total | 50 |

| Clothing | 55 |

| Cycle & run | 35 |

| Could not be traced to clothing or cycling at Hartford | 10 |

| Could not be traced to Boston or Hartford | 10 |

Part 1 (Static)

Required:

1. Prepare a contribution income statement for CWI showing the contribution margin, controllable margin, and contribution by profit center for both the Boston and Hartford stores, and also for the clothing and cycle & run units of the Hartford store.

1. Prepare a contribution income statement for CWI showing the contribution margin, controllable margin, and contribution by profit center for both the Boston and Hartford stores, and also for the clothing and cycle \& run units of the Hartford store

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISO 27001 Controls A Guide To Implementing And Auditing

Authors: IT Governance

1st Edition

1787781445, 978-1787781443