Answered step by step

Verified Expert Solution

Question

1 Approved Answer

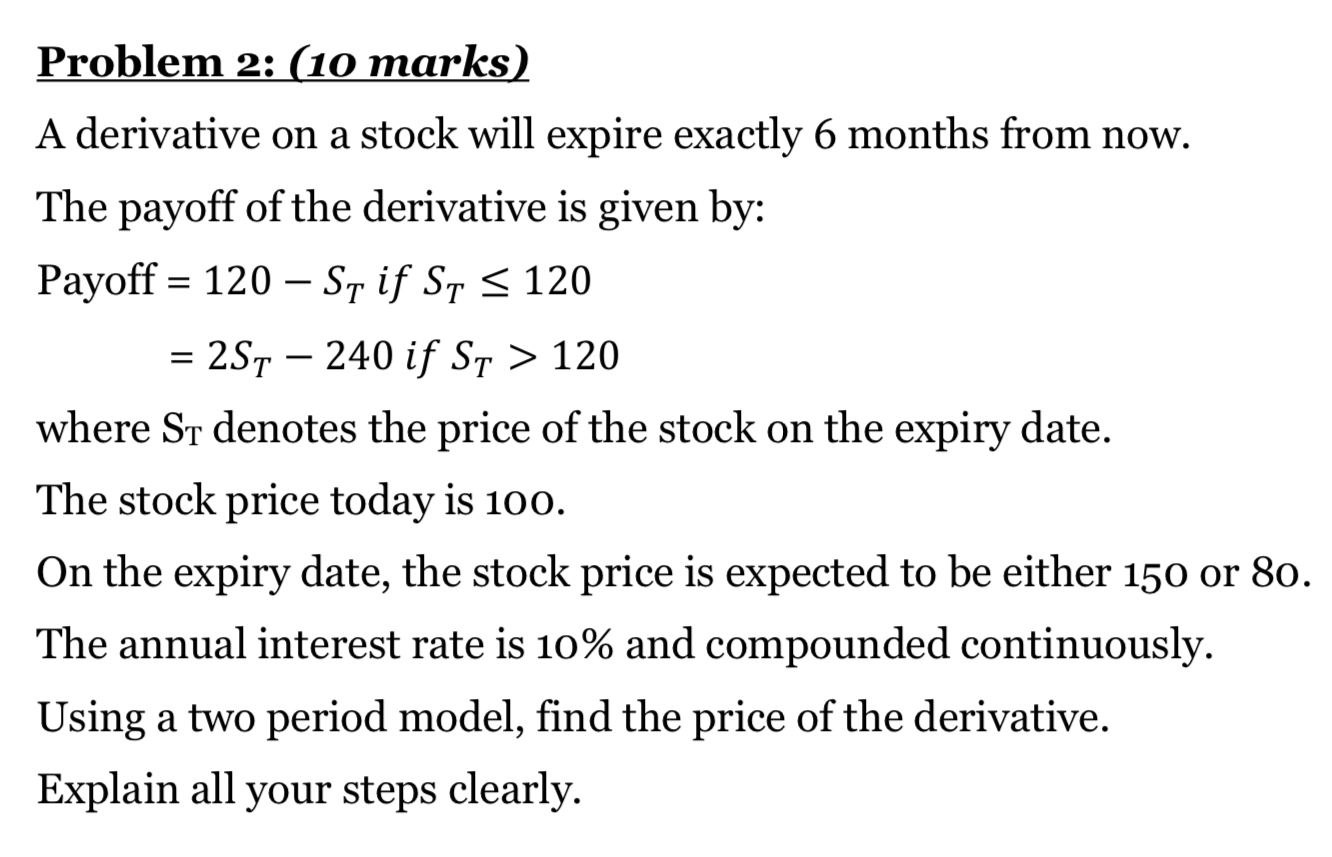

Problem 2: (10 marks) A derivative on a stock will expire exactly 6 months from now. The payoff of the derivative is given by: Payoff=120STifST120=2ST240ifST>120

Problem 2: (10 marks) A derivative on a stock will expire exactly 6 months from now. The payoff of the derivative is given by: Payoff=120STifST120=2ST240ifST>120 where ST denotes the price of the stock on the expiry date. The stock price today is 100 . On the expiry date, the stock price is expected to be either 150 or 80 The annual interest rate is 10% and compounded continuously. Using a two period model, find the price of the derivative. Explain all your steps clearly

Problem 2: (10 marks) A derivative on a stock will expire exactly 6 months from now. The payoff of the derivative is given by: Payoff=120STifST120=2ST240ifST>120 where ST denotes the price of the stock on the expiry date. The stock price today is 100 . On the expiry date, the stock price is expected to be either 150 or 80 The annual interest rate is 10% and compounded continuously. Using a two period model, find the price of the derivative. Explain all your steps clearly Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Re Imagining Offshore Finance

Authors: Christopher M. Bruner

1st Edition

0190466871, 978-0190466879