Answered step by step

Verified Expert Solution

Question

1 Approved Answer

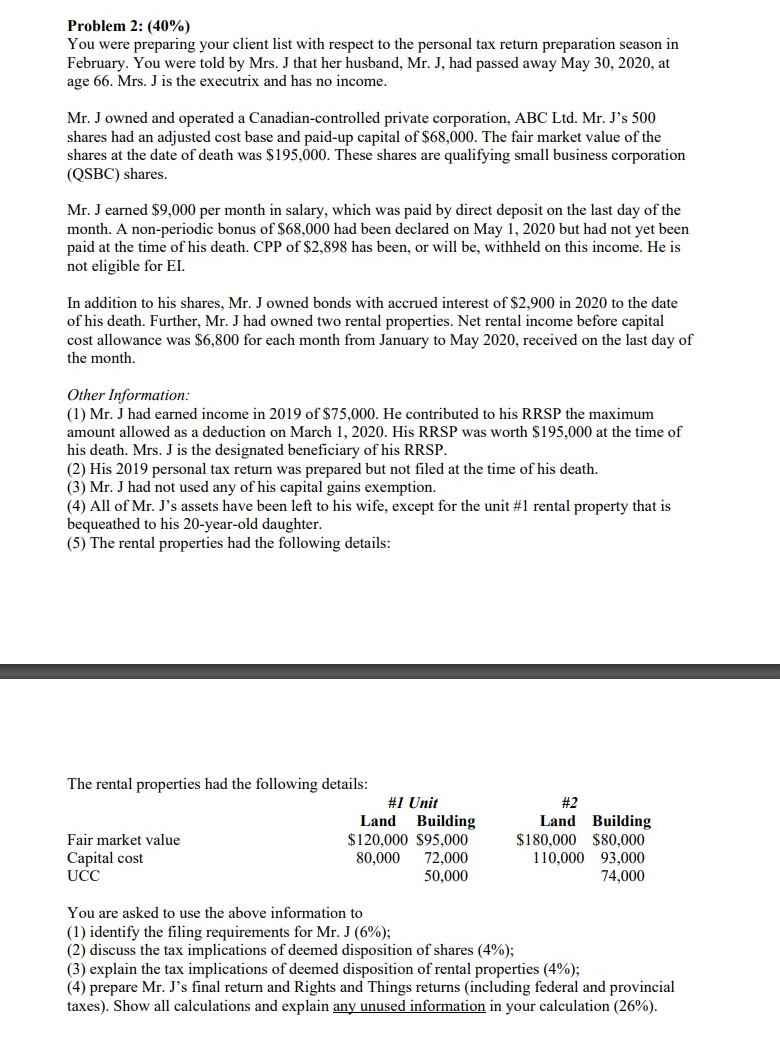

Problem 2: (40 /o) You were preparing your client list with mspect to the personal tax return preparation season in February. You were told by

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Criminal Law And Its Processes Cases And Materials

Authors: Sanford H. Kadish, Stephen Schulhofer, Rachel E. Barkow

11th Edition

1543810772, 978-1543810776