Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Problem 2. A European binary (or Digital) option pays $6 if the stock price ends above $55 after 3 months and nothing (pays $0 )

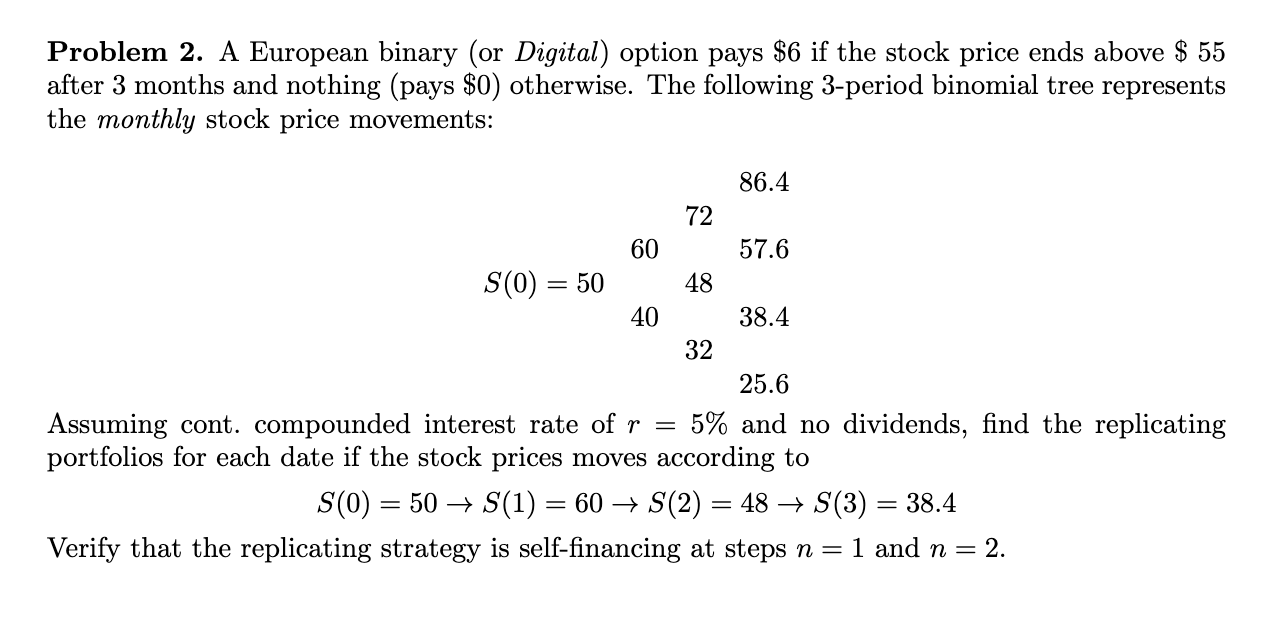

Problem 2. A European binary (or Digital) option pays $6 if the stock price ends above $55 after 3 months and nothing (pays $0 ) otherwise. The following 3-period binomial tree represents the monthly stock price movements: Assuming cont. compounded interest rate of r=5% and no dividends, find the replicating portfolios for each date if the stock prices moves according to S(0)=50S(1)=60S(2)=48S(3)=38.4 Verify that the replicating strategy is self-financing at steps n=1 and n=2

Problem 2. A European binary (or Digital) option pays $6 if the stock price ends above $55 after 3 months and nothing (pays $0 ) otherwise. The following 3-period binomial tree represents the monthly stock price movements: Assuming cont. compounded interest rate of r=5% and no dividends, find the replicating portfolios for each date if the stock prices moves according to S(0)=50S(1)=60S(2)=48S(3)=38.4 Verify that the replicating strategy is self-financing at steps n=1 and n=2 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management In Construction Contracting

Authors: Andrew Ross, Peter Williams

1st Edition

1405125063, 9781405125062