Answered step by step

Verified Expert Solution

Question

1 Approved Answer

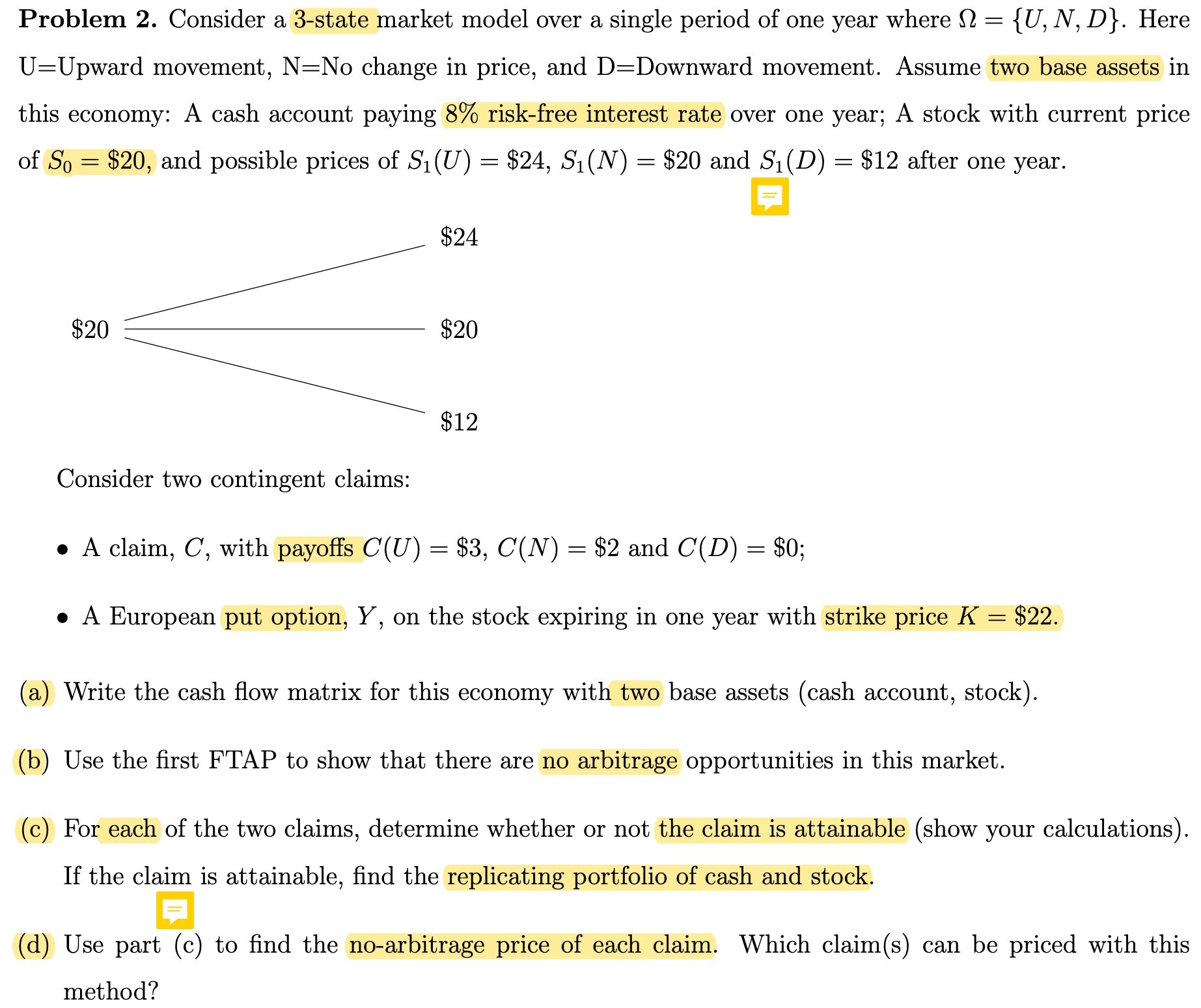

Problem 2. Consider a 3-state market model over a single period of one year Where (2 = {U, N, D}. Here U=Upward movement, N=No change

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Differential Equations A Maple™ Supplement

Authors: Robert P Gilbert, George C Hsiao, Robert J Ronkese

2nd Edition

1000402525, 9781000402520