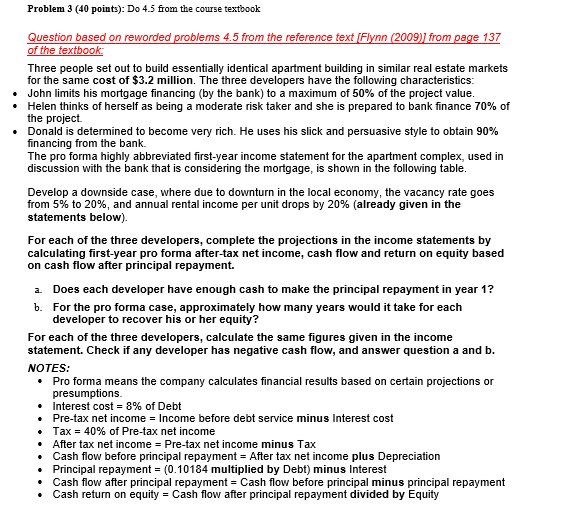

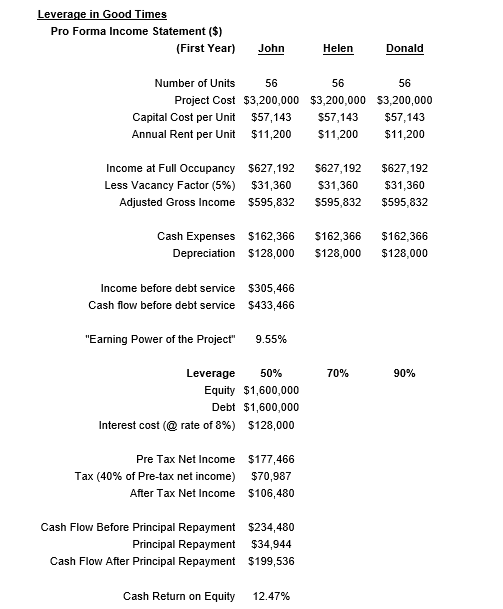

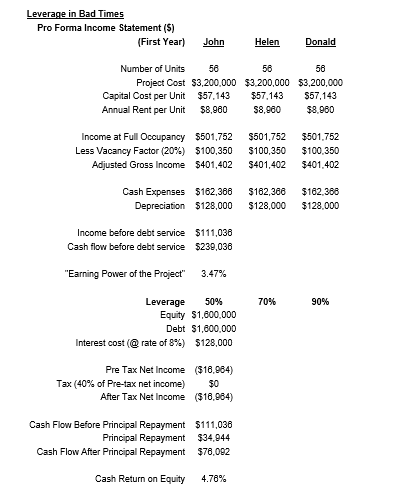

Problem 3 (40 points): Do 4.5 from the course textbook Question based on reworded problems 4.5 from the reference text [Flynn (2009)] from page 137 of the textbook Three people set out to build essentially identical apartment building in similar real estate markets for the same cost of $3.2 million. The three developers have the following characteristics John limits his mortgage financing (by the bank) to a maximum of 50% of the project value Helen thinks of herself as being a moderate risk taker and she is prepared to bank finance 70% of the project Donald is determined to become very rich. He uses his slick and persuasive style to obtain 90% financing from the bank. The pro forma highly abbreviated first-year income statement for the apartment complex, used in discussion with the bank that is considering the mortgage, is shown in the following table. Develop a downside case, where due to downturn in the local economy, the vacancy rate goes from 5% to 20%, and annual rental income per unit drops by 20% (already given in the statements below) For each of the three developers, complete the projections in the income statements by calculating first-year pro forma after-tax net income, cash flow and return on equity based on cash flow after principal repayment Does each developer have enough cash to make the principal repayment in year 1? a b. For the pro forma case, approximately how many years would it take for each developer to recover his or her equity? For each of the three developers, calculate the same figures given in the income statement. Check if any developer has negative cash flow, and answer question a and b. NOTES: Pro forma means the company calculates financial results based on certain projections or presumptions. Interest cost 8% of Debt Pre-tax net income Income before debt service minus Interest cost Tax 40% of Pre-tax net income After tax net income Pre-tax net income minus Tax Cash flow before principal repayment After tax net income plus Depreciation Principal repayment (0.10184 multiplied by Debt) minus Interest Cash flow after principal repayment Cash flow before principal minus principal repayment Cash return on equity Cash flow after principal repayment divided by Equity Leverage in Good Times Pro Forma Income Statement ($) (First Year) John Helen Donald Number of Units 56 56 56 Project Cost $3,200,000 $3,200,000 $3,200,000 Capital Cost per Unit $57,143 $57,143 $57,143 Annual Rent per Unit $11,200 $11,200 $11,200 Income at Full Occupancy $627,192 $627,192 $627,192 Less Vacancy Factor (5%) $31,360 $31,360 $31,360 Adjusted Gross Income $595,832 $595,832 $595,832 Cash Expenses $162,366 $162,366 $162,366 $128,000 Depreciation $128,000 $128,000 Income before debt service $305,466 Cash flow before debt service $433,466 "Earning Power of the Project 9.55% Leverage 50% 70% 90% Equity $1,600,000 Debt $1,600,000 Interest cost (@ rate of 8 %) $128,000 Pre Tax Net Income $177,466 Tax (40% of Pre-tax net income) $70,987 After Tax Net Income $106,480 Cash Flow Before Principal Repayment $234,480 Principal Repayment $34,944 Cash Flow After Principal Repayment $199,536 Cash Return on Equity 12.47% Leverage in Bad Times Pro Forma Income Statement (S) (First Year) John Helen Donald Number of Units 56 56 56 Project Cost $3,200,000 $3,200,000 $3,200,000 $57,143 Capital Cost per Unit $57.143 $57,143 S8,980 S8,060 Annual Rent per Unit $8,980 Income at Full Occupancy $501,752 $501,752 $501.752 Less Vacancy Factor (20 % ) $100,350 $100,350 $100,350 Adjusted Gross Income $401,402 $401,402 $401.402 Cash Expenses $162,366 $162,368 $182,388 Depreciation $128,000 $128,000 $128,000 Income before debt service $111,036 Cash flow before debt service $239,038 "Earning Power of the Project 3.47% Leverage 50% 70% 90% Equity $1,800,000 Debt $1,800,000 Interest cost ( rate of 8 % ) $128,000 Pre Tax Net Income ($16,984) Tax (40 % of Pre-tax net income) $0 After Tax Net Income ($18,984) Cash Flow Before Principal Repayment Principal Repayment Cash Flow After Principal Repayment $111,036 $34,944 $78,092 Cash Return on Equity 4.76% Problem 3 (40 points): Do 4.5 from the course textbook Question based on reworded problems 4.5 from the reference text [Flynn (2009)] from page 137 of the textbook Three people set out to build essentially identical apartment building in similar real estate markets for the same cost of $3.2 million. The three developers have the following characteristics John limits his mortgage financing (by the bank) to a maximum of 50% of the project value Helen thinks of herself as being a moderate risk taker and she is prepared to bank finance 70% of the project Donald is determined to become very rich. He uses his slick and persuasive style to obtain 90% financing from the bank. The pro forma highly abbreviated first-year income statement for the apartment complex, used in discussion with the bank that is considering the mortgage, is shown in the following table. Develop a downside case, where due to downturn in the local economy, the vacancy rate goes from 5% to 20%, and annual rental income per unit drops by 20% (already given in the statements below) For each of the three developers, complete the projections in the income statements by calculating first-year pro forma after-tax net income, cash flow and return on equity based on cash flow after principal repayment Does each developer have enough cash to make the principal repayment in year 1? a b. For the pro forma case, approximately how many years would it take for each developer to recover his or her equity? For each of the three developers, calculate the same figures given in the income statement. Check if any developer has negative cash flow, and answer question a and b. NOTES: Pro forma means the company calculates financial results based on certain projections or presumptions. Interest cost 8% of Debt Pre-tax net income Income before debt service minus Interest cost Tax 40% of Pre-tax net income After tax net income Pre-tax net income minus Tax Cash flow before principal repayment After tax net income plus Depreciation Principal repayment (0.10184 multiplied by Debt) minus Interest Cash flow after principal repayment Cash flow before principal minus principal repayment Cash return on equity Cash flow after principal repayment divided by Equity Leverage in Good Times Pro Forma Income Statement ($) (First Year) John Helen Donald Number of Units 56 56 56 Project Cost $3,200,000 $3,200,000 $3,200,000 Capital Cost per Unit $57,143 $57,143 $57,143 Annual Rent per Unit $11,200 $11,200 $11,200 Income at Full Occupancy $627,192 $627,192 $627,192 Less Vacancy Factor (5%) $31,360 $31,360 $31,360 Adjusted Gross Income $595,832 $595,832 $595,832 Cash Expenses $162,366 $162,366 $162,366 $128,000 Depreciation $128,000 $128,000 Income before debt service $305,466 Cash flow before debt service $433,466 "Earning Power of the Project 9.55% Leverage 50% 70% 90% Equity $1,600,000 Debt $1,600,000 Interest cost (@ rate of 8 %) $128,000 Pre Tax Net Income $177,466 Tax (40% of Pre-tax net income) $70,987 After Tax Net Income $106,480 Cash Flow Before Principal Repayment $234,480 Principal Repayment $34,944 Cash Flow After Principal Repayment $199,536 Cash Return on Equity 12.47% Leverage in Bad Times Pro Forma Income Statement (S) (First Year) John Helen Donald Number of Units 56 56 56 Project Cost $3,200,000 $3,200,000 $3,200,000 $57,143 Capital Cost per Unit $57.143 $57,143 S8,980 S8,060 Annual Rent per Unit $8,980 Income at Full Occupancy $501,752 $501,752 $501.752 Less Vacancy Factor (20 % ) $100,350 $100,350 $100,350 Adjusted Gross Income $401,402 $401,402 $401.402 Cash Expenses $162,366 $162,368 $182,388 Depreciation $128,000 $128,000 $128,000 Income before debt service $111,036 Cash flow before debt service $239,038 "Earning Power of the Project 3.47% Leverage 50% 70% 90% Equity $1,800,000 Debt $1,800,000 Interest cost ( rate of 8 % ) $128,000 Pre Tax Net Income ($16,984) Tax (40 % of Pre-tax net income) $0 After Tax Net Income ($18,984) Cash Flow Before Principal Repayment Principal Repayment Cash Flow After Principal Repayment $111,036 $34,944 $78,092 Cash Return on Equity 4.76%