Answered step by step

Verified Expert Solution

Question

1 Approved Answer

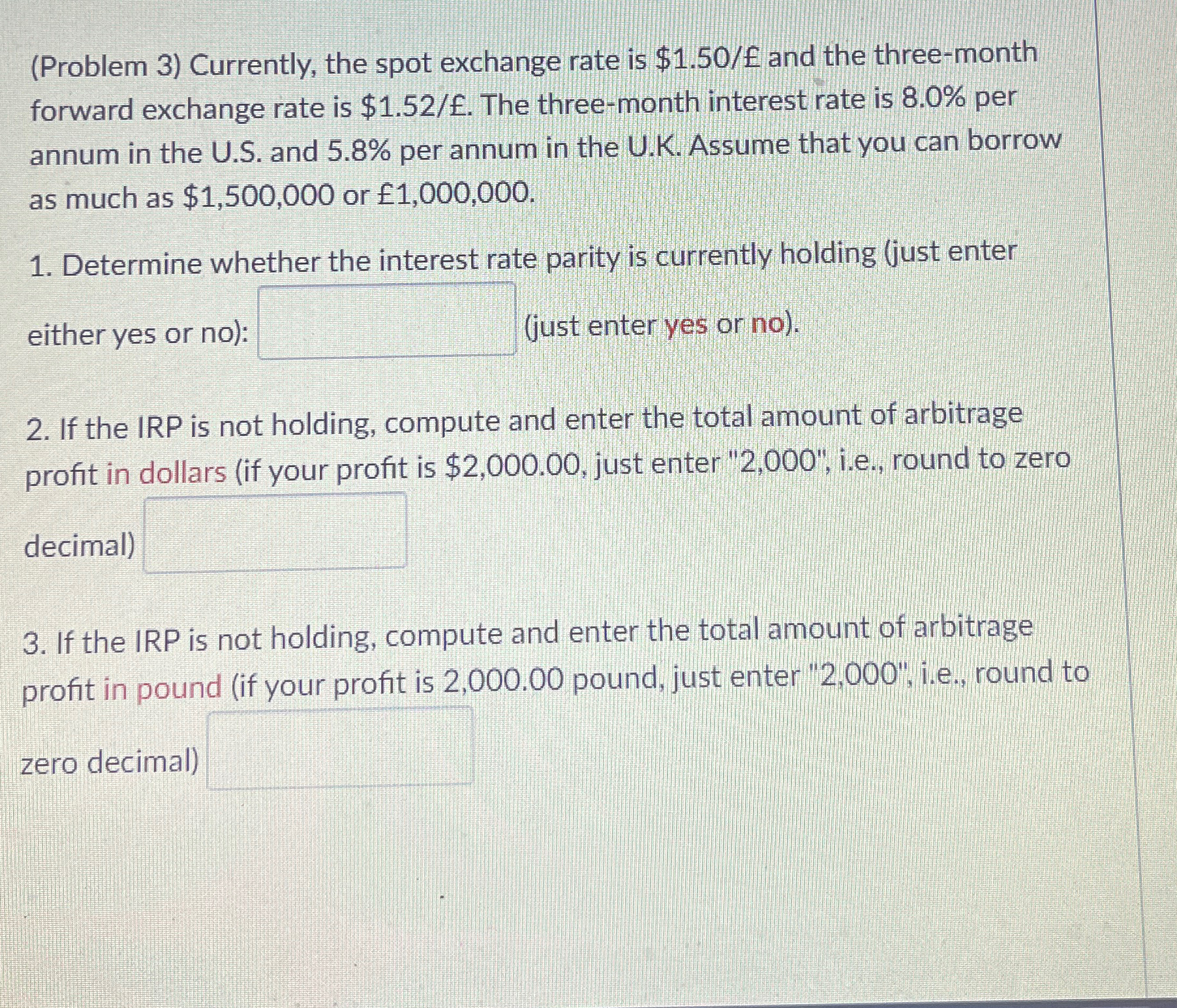

( Problem 3 ) Currently, the spot exchange rate is $ 1 . 5 0 and the three - month forward exchange rate is $

Problem Currently, the spot exchange rate is $ and the threemonth forward exchange rate is $ The threemonth interest rate is per annum in the US and per annum in the UK Assume that you can borrow as much as $ or

Determine whether the interest rate parity is currently holding just enter either yes or no: just enter yes or no

If the IRP is not holding, compute and enter the total amount of arbitrage profit in dollars if your profit is $ just enter ie round to zero decimal

If the IRP is not holding, compute and enter the total amount of arbitrage profit in pound if your profit is pound, just enter ie round to zero decimal

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Master Forex Market Basics A Step By Step Guide To Successful Trading

Authors: Jodi Six

1st Edition

979-8388680884