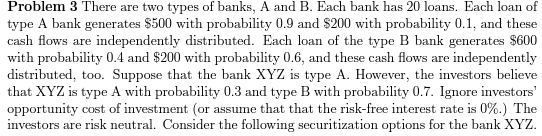

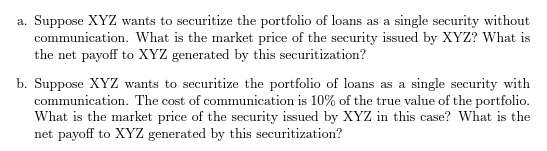

Problem 3 There are two types of banks, A and B. Each bank has 20 loans. Each loan of type A bank generates $500 with probability 0.9 and $200 with probability 0.1, and these cash flows are independently distributed. Each loan of the type B bank generates $600 with probability 0.4 and $200 with probability 0.6, and these cash flows are independently distributed, too. Suppose that the bank XYZ is type A. However, the investors believe that XYZ is type A with probability 0.3 and type B with probability 0.7. Ignore investors' opportunity cost of investment (or assume that that the risk-free interest rate is 0%.) The investors are risk neutral. Consider the following securitization options for the bank XYZ. a. Suppose XYZ wants to securitize the portfolio of loans as a single security without communication. What is the market price of the security issued by XYZ? What is the net payoff to XYZ generated by this securitization? b. Suppose XYZ wants to securitize the portfolio of loans as a single security with communication. The cost of communication is 10% of the true value of the portfolio. What is the market price of the security issued by XYZ in this case? What is the net payoff to XYZ generated by this securitization? Problem 3 There are two types of banks, A and B. Each bank has 20 loans. Each loan of type A bank generates $500 with probability 0.9 and $200 with probability 0.1, and these cash flows are independently distributed. Each loan of the type B bank generates $600 with probability 0.4 and $200 with probability 0.6, and these cash flows are independently distributed, too. Suppose that the bank XYZ is type A. However, the investors believe that XYZ is type A with probability 0.3 and type B with probability 0.7. Ignore investors' opportunity cost of investment (or assume that that the risk-free interest rate is 0%.) The investors are risk neutral. Consider the following securitization options for the bank XYZ. a. Suppose XYZ wants to securitize the portfolio of loans as a single security without communication. What is the market price of the security issued by XYZ? What is the net payoff to XYZ generated by this securitization? b. Suppose XYZ wants to securitize the portfolio of loans as a single security with communication. The cost of communication is 10% of the true value of the portfolio. What is the market price of the security issued by XYZ in this case? What is the net payoff to XYZ generated by this securitization