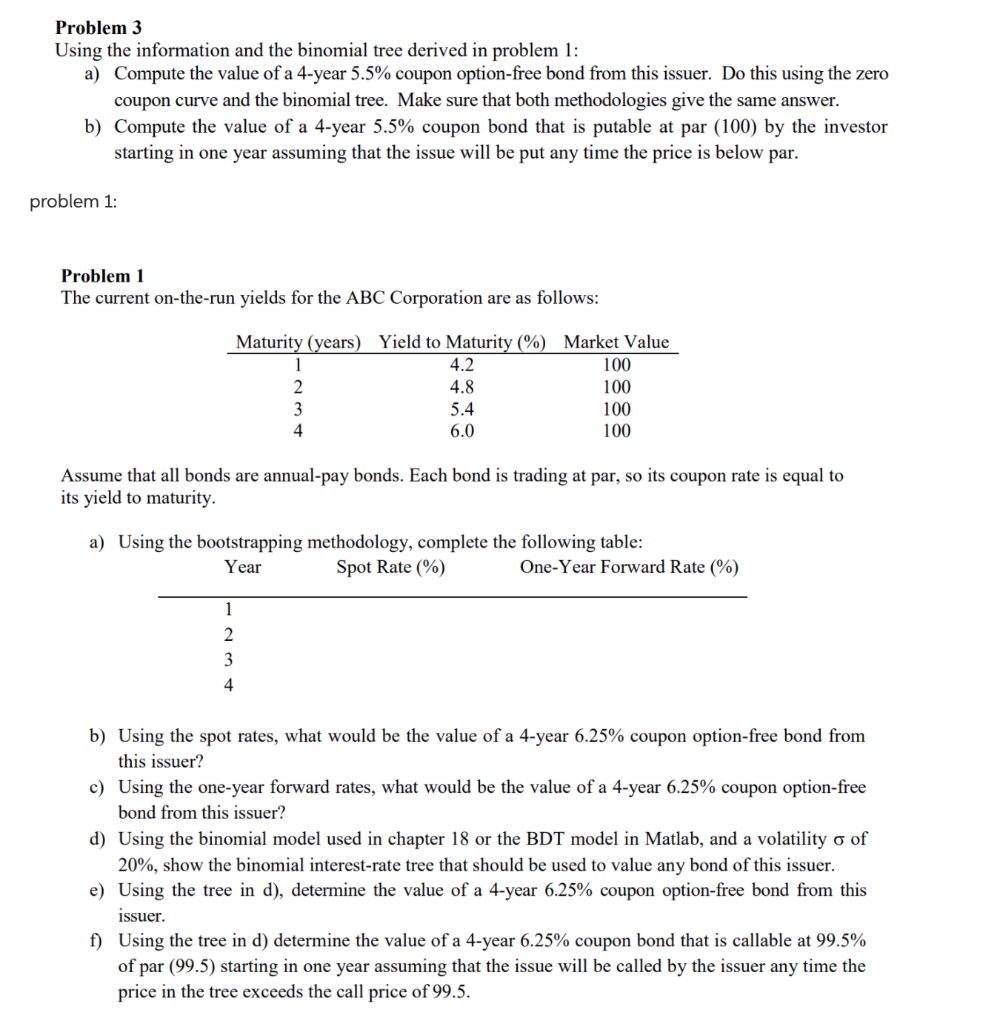

Problem 3 Using the information and the binomial tree derived in problem 1: a) Compute the value of a 4-year 5.5% coupon option-free bond from this issuer. Do this using the zero coupon curve and the binomial tree. Make sure that both methodologies give the same answer. b) Compute the value of a 4-year 5.5% coupon bond that is putable at par (100) by the investor starting in one year assuming that the issue will be put any time the price is below par. problem 1: Problem 1 The current on-the-run yields for the ABC Corporation are as follows: Maturity (years) Yield to Maturity (%) Market Value 1 4.2 100 2 4.8 100 3 5.4 100 4 6.0 100 Assume that all bonds are annual-pay bonds. Each bond is trading at par, so its coupon rate is equal to its yield to maturity. a) Using the bootstrapping methodology, complete the following table: Year Spot Rate (%) One-Year Forward Rate (%) 1 2 3 4 b) Using the spot rates, what would be the value of a 4-year 6.25% coupon option-free bond from this issuer? c) Using the one-year forward rates, what would be the value of a 4-year 6.25% coupon option-free bond from this issuer? d) Using the binomial model used in chapter 18 or the BDT model in Matlab, and a volatility o of 20%, show the binomial interest-rate tree that should be used to value any bond of this issuer. e) Using the tree in d), determine the value of a 4-year 6.25% coupon option-free bond from this issuer. f) Using the tree in d) determine the value of a 4-year 6.25% coupon bond that is callable at 99.5% of par (99.5) starting in one year assuming that the issue will be called by the issuer any time the price in the tree exceeds the call price of 99.5. Problem 3 Using the information and the binomial tree derived in problem 1: a) Compute the value of a 4-year 5.5% coupon option-free bond from this issuer. Do this using the zero coupon curve and the binomial tree. Make sure that both methodologies give the same answer. b) Compute the value of a 4-year 5.5% coupon bond that is putable at par (100) by the investor starting in one year assuming that the issue will be put any time the price is below par. problem 1: Problem 1 The current on-the-run yields for the ABC Corporation are as follows: Maturity (years) Yield to Maturity (%) Market Value 1 4.2 100 2 4.8 100 3 5.4 100 4 6.0 100 Assume that all bonds are annual-pay bonds. Each bond is trading at par, so its coupon rate is equal to its yield to maturity. a) Using the bootstrapping methodology, complete the following table: Year Spot Rate (%) One-Year Forward Rate (%) 1 2 3 4 b) Using the spot rates, what would be the value of a 4-year 6.25% coupon option-free bond from this issuer? c) Using the one-year forward rates, what would be the value of a 4-year 6.25% coupon option-free bond from this issuer? d) Using the binomial model used in chapter 18 or the BDT model in Matlab, and a volatility o of 20%, show the binomial interest-rate tree that should be used to value any bond of this issuer. e) Using the tree in d), determine the value of a 4-year 6.25% coupon option-free bond from this issuer. f) Using the tree in d) determine the value of a 4-year 6.25% coupon bond that is callable at 99.5% of par (99.5) starting in one year assuming that the issue will be called by the issuer any time the price in the tree exceeds the call price of 99.5