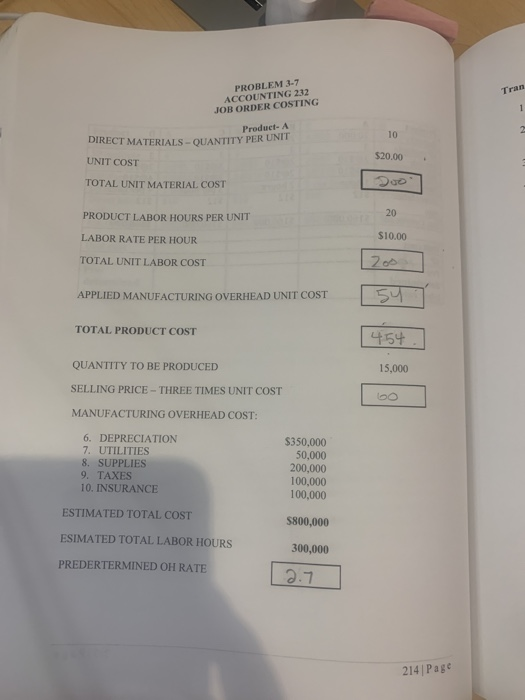

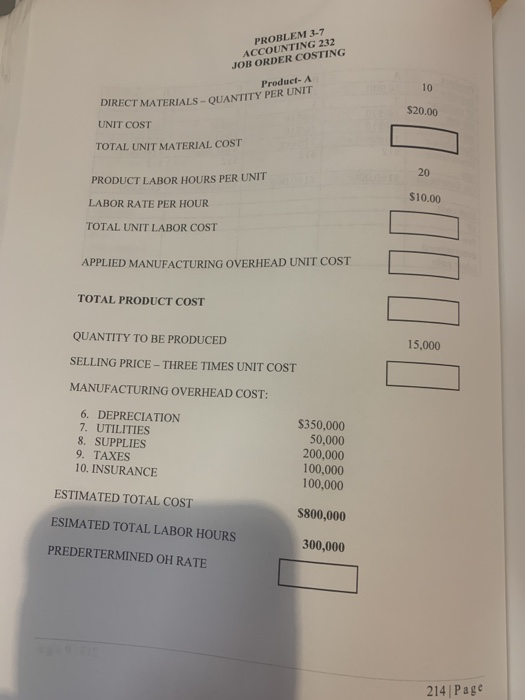

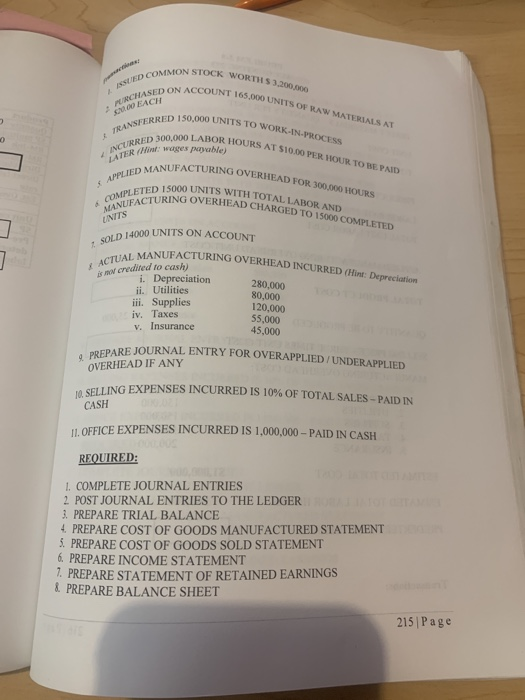

PROBLEM 3-7 ACCOUNTING 232 JOB ORDER COSTING Product- A DIRECT MATERIALS - QUANTITY PER UNIT $20.00 UNIT COST TOTAL UNIT MATERIAL COST PRODUCT LABOR HOURS PER UNIT 20 LABOR RATE PER HOUR $10.00 TOTAL UNIT LABOR COST APPLIED MANUFACTURING OVERHEAD UNIT COST TOTAL PRODUCT COST 15,000 QUANTITY TO BE PRODUCED SELLING PRICE - THREE TIMES UNIT COST MANUFACTURING OVERHEAD COST: 6. DEPRECIATION 7. UTILITIES 8. SUPPLIES 9. TAXES 10. INSURANCE $350,000 50,000 200,000 100,000 100,000 ESTIMATED TOTAL COST S800,000 ESIMATED TOTAL LABOR HOURS PREDERTERMINED OH RATE 300,000 214| Page COMMON STOCK WORTHS 3.20 ISSUED COM ACCOUNT 165.000 UNITS OF RAW MATERIALS AT CHASED ON A EACH TRANSFERRED 150,000 UNITS TO WORK-IN-PROCESS D 300,000 LABOR HOURS AT OR HOURS AT 510.00 PER HOUR TO BE PAID INCURRED 300 INTER (Hin wages puble) NUFACTURING OVERHEAD FOR 300.000 HOURS APPLIED MANUE ETED 15000 UNITS WITH TOTA ITS WITH TOTAL LABOR AND COMPLEZ URING OVERHEAD CHARGED TO 15000 COMPLETED MANUFACTURING UNITS 4000 UNITS ON ACCOUNT IANUFACTURING OVERHEAD INCURRED (Hint: Depreciation ACTUAL MANUFAC credited to cash) i. Depreciation ii. Utilities iii. Supplies iv. Taxes y Insurance 280.000 80,000 120,000 55,000 45,000 PARE JOURNAL ENTRY FOR OVERAPPLIED/UNDERAPPLIED PREPARE JOUR OVERHEAD IF ANY SELLING EXPENSES INCURRED IS 10% OF TOTAL SALES - PAID IN CASH 11. OFFICE EXPENSES INCURRED IS 1,000,000 - PAID IN CASH REQUIRED: 1. COMPLETE JOURNAL ENTRIES 2. POST JOURNAL ENTRIES TO THE LEDGER 3. PREPARE TRIAL BALANCE 4. PREPARE COST OF GOODS MANUFACTURED STATEMENT S PREPARE COST OF GOODS SOLD STATEMENT 6. PREPARE INCOME STATEMENT 7. PREPARE STATEMENT OF RETAINED EARNINGS & PREPARE BALANCE SHEET 215 Page Tran PROBLEM 3-7 ACCOUNTING 232 JOB ORDER COSTING 10 Product- A DIRECT MATERIALS - QUANTITY PER UNIT UNIT COST $20.00 TOTAL UNIT MATERIAL COST DO PRODUCT LABOR HOURS PER UNIT LABOR RATE PER HOUR $10.00 Zoo TOTAL UNIT LABOR COST APPLIED MANUFACTURING OVERHEAD UNIT COST TOTAL PRODUCT COST | 454 . 15,000 QUANTITY TO BE PRODUCED SELLING PRICE - THREE TIMES UNIT COST MANUFACTURING OVERHEAD COST: 6. DEPRECIATION 7. UTILITIES 8. SUPPLIES 9. TAXES 10. INSURANCE $350,000 50,000 200,000 100,000 100,000 ESTIMATED TOTAL COST ESIMATED TOTAL LABOR HOURS $800,000 300,000 PREDERTERMINED OH RATE 12.7 214 | Page PROBLEM 3-7 ACCOUNTING 232 JOB ORDER COSTING Product- A DIRECT MATERIALS - QUANTITY PER UNIT $20.00 UNIT COST TOTAL UNIT MATERIAL COST PRODUCT LABOR HOURS PER UNIT 20 LABOR RATE PER HOUR $10.00 TOTAL UNIT LABOR COST APPLIED MANUFACTURING OVERHEAD UNIT COST TOTAL PRODUCT COST 15,000 QUANTITY TO BE PRODUCED SELLING PRICE - THREE TIMES UNIT COST MANUFACTURING OVERHEAD COST: 6. DEPRECIATION 7. UTILITIES 8. SUPPLIES 9. TAXES 10. INSURANCE $350,000 50,000 200,000 100,000 100,000 ESTIMATED TOTAL COST S800,000 ESIMATED TOTAL LABOR HOURS PREDERTERMINED OH RATE 300,000 214| Page COMMON STOCK WORTHS 3.20 ISSUED COM ACCOUNT 165.000 UNITS OF RAW MATERIALS AT CHASED ON A EACH TRANSFERRED 150,000 UNITS TO WORK-IN-PROCESS D 300,000 LABOR HOURS AT OR HOURS AT 510.00 PER HOUR TO BE PAID INCURRED 300 INTER (Hin wages puble) NUFACTURING OVERHEAD FOR 300.000 HOURS APPLIED MANUE ETED 15000 UNITS WITH TOTA ITS WITH TOTAL LABOR AND COMPLEZ URING OVERHEAD CHARGED TO 15000 COMPLETED MANUFACTURING UNITS 4000 UNITS ON ACCOUNT IANUFACTURING OVERHEAD INCURRED (Hint: Depreciation ACTUAL MANUFAC credited to cash) i. Depreciation ii. Utilities iii. Supplies iv. Taxes y Insurance 280.000 80,000 120,000 55,000 45,000 PARE JOURNAL ENTRY FOR OVERAPPLIED/UNDERAPPLIED PREPARE JOUR OVERHEAD IF ANY SELLING EXPENSES INCURRED IS 10% OF TOTAL SALES - PAID IN CASH 11. OFFICE EXPENSES INCURRED IS 1,000,000 - PAID IN CASH REQUIRED: 1. COMPLETE JOURNAL ENTRIES 2. POST JOURNAL ENTRIES TO THE LEDGER 3. PREPARE TRIAL BALANCE 4. PREPARE COST OF GOODS MANUFACTURED STATEMENT S PREPARE COST OF GOODS SOLD STATEMENT 6. PREPARE INCOME STATEMENT 7. PREPARE STATEMENT OF RETAINED EARNINGS & PREPARE BALANCE SHEET 215 Page Tran PROBLEM 3-7 ACCOUNTING 232 JOB ORDER COSTING 10 Product- A DIRECT MATERIALS - QUANTITY PER UNIT UNIT COST $20.00 TOTAL UNIT MATERIAL COST DO PRODUCT LABOR HOURS PER UNIT LABOR RATE PER HOUR $10.00 Zoo TOTAL UNIT LABOR COST APPLIED MANUFACTURING OVERHEAD UNIT COST TOTAL PRODUCT COST | 454 . 15,000 QUANTITY TO BE PRODUCED SELLING PRICE - THREE TIMES UNIT COST MANUFACTURING OVERHEAD COST: 6. DEPRECIATION 7. UTILITIES 8. SUPPLIES 9. TAXES 10. INSURANCE $350,000 50,000 200,000 100,000 100,000 ESTIMATED TOTAL COST ESIMATED TOTAL LABOR HOURS $800,000 300,000 PREDERTERMINED OH RATE 12.7 214 | Page