Answered step by step

Verified Expert Solution

Question

1 Approved Answer

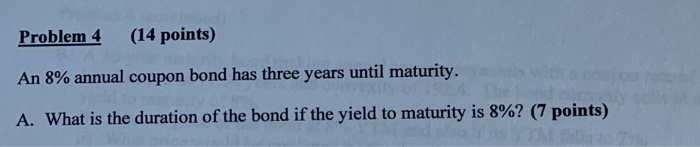

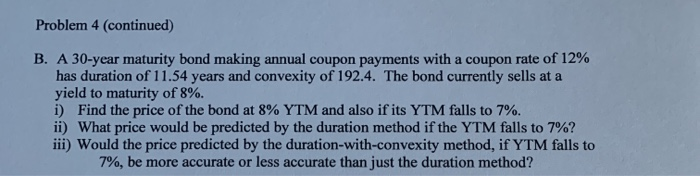

Problem 4 (14 points) An 8% annual coupon bond has three years until maturity. A. What is the duration of the bond if the yield

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance Exchange Rates And Financial Flows In The International Financial System

Authors: Heather D. Gibson

1st Edition

0582218128, 978-0582218123