Answered step by step

Verified Expert Solution

Question

1 Approved Answer

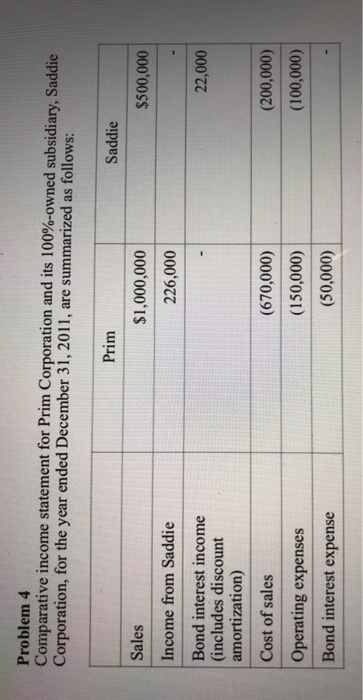

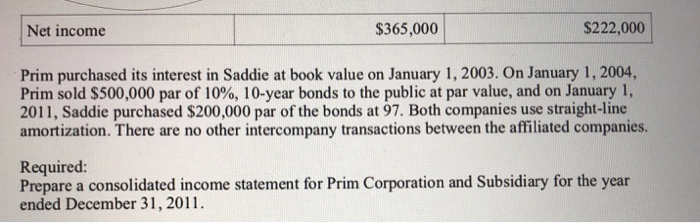

Problem 4 Comparative income statement for Prim Corporation and its 100%-owned subsidiary, Saddie Corporation, for the year ended December 31, 2011, are summarized as follows:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Performance Audit In The Face Of The Financial And Economic Crisis Application Of The Quality Control Appropriate To The Risks

Authors: Laureano Triana Rubio

1st Edition

6203482390, 978-6203482393