Answered step by step

Verified Expert Solution

Question

1 Approved Answer

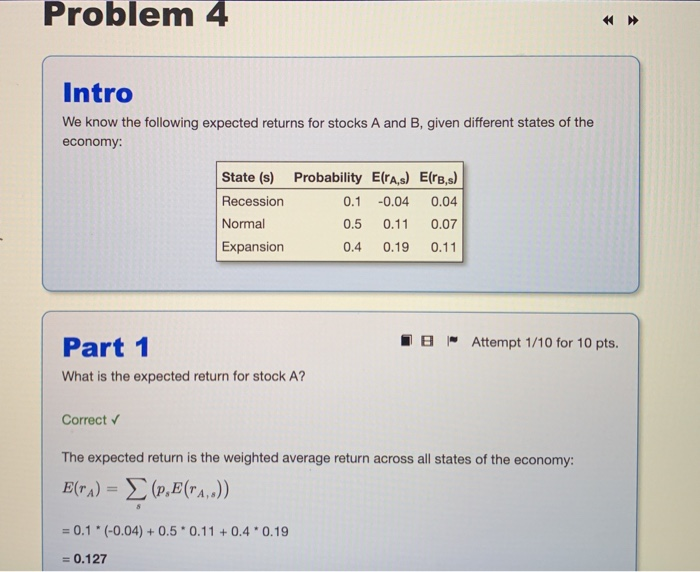

Problem 4 Intro We know the following expected returns for stocks A and B, given different states of the economy: State (s) Probability Eras) E(TB,s)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dividend Policy On Share Price Volatility In Indian Stock Market

Authors: Vijay Deswal

1st Edition

3841859623, 978-3841859624