Answered step by step

Verified Expert Solution

Question

1 Approved Answer

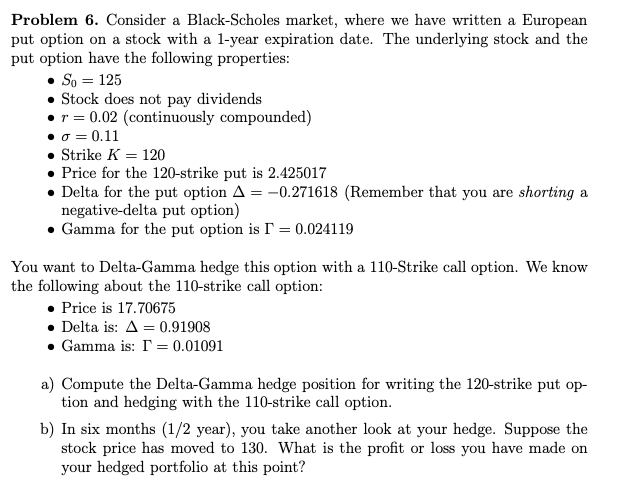

Problem 6. Consider a Black-Scholes market, where we have written a European put option on a stock with a 1-year expiration date. The underlying stock

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Study Guide To Accompany Financial Accounting In An Economic Context

Authors: Jamie Pratt

6th Edition

0471731110, 978-0471731115