Answered step by step

Verified Expert Solution

Question

1 Approved Answer

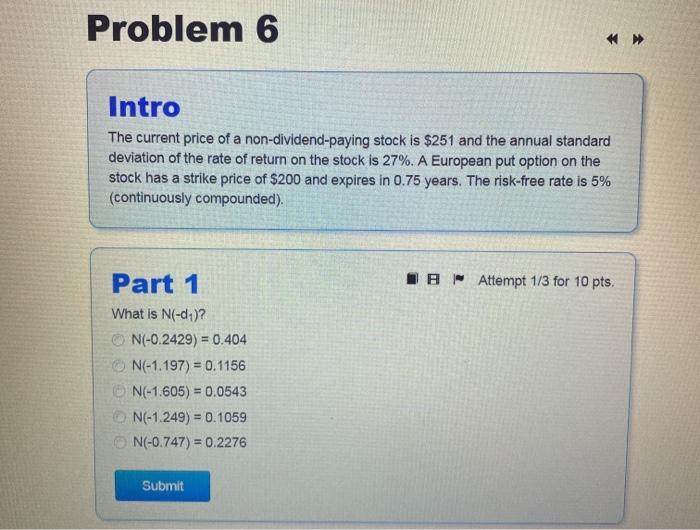

Problem 6 >> Intro The current price of a non-dividend-paying stock is $251 and the annual standard deviation of the rate of return on the

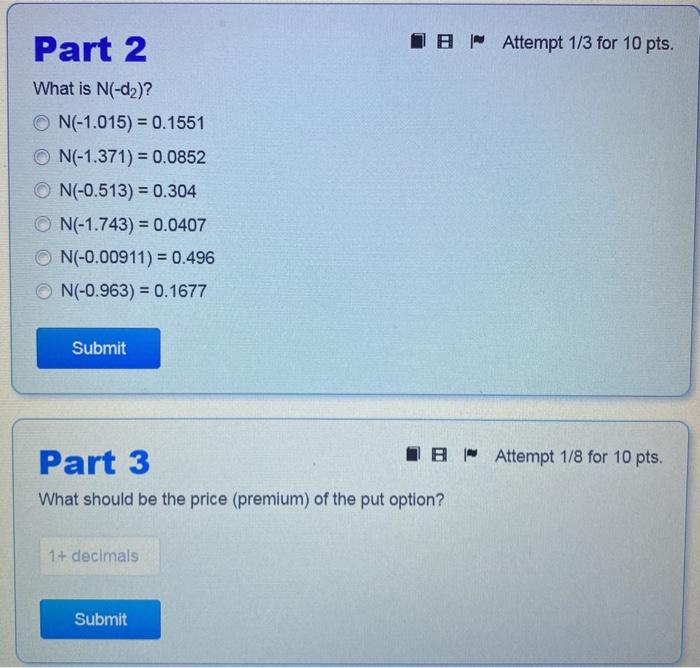

Problem 6 >> Intro The current price of a non-dividend-paying stock is $251 and the annual standard deviation of the rate of return on the stock is 27%. A European put option on the stock has a strike price of $200 and expires in 0.75 years. The risk-free rate is 5% (continuously compounded). JB Attempt 1/3 for 10 pts. Part 1 What is N(-d)? N(-0.2429) = 0.404 N(-1.197) = 0.1156 N(-1.605) = 0.0543 N(-1.249) = 0.1059 N(-0.747) = 0.2276 Submit Io Attempt 1/3 for 10 pts. Part 2 What is N(-d2)? ON(-1.015) = 0.1551 ON(-1.371) = 0.0852 ON(-0.513) = 0.304 N(-1.743) = 0.0407 ON(-0.00911) = 0.496 ON(-0.963) = 0.1677 Submit Part 3 IB Attempt 1/8 for 10 pts. What should be the price (premium) of the put option? 1+ decimals Submit

Problem 6 >> Intro The current price of a non-dividend-paying stock is $251 and the annual standard deviation of the rate of return on the stock is 27%. A European put option on the stock has a strike price of $200 and expires in 0.75 years. The risk-free rate is 5% (continuously compounded). JB Attempt 1/3 for 10 pts. Part 1 What is N(-d)? N(-0.2429) = 0.404 N(-1.197) = 0.1156 N(-1.605) = 0.0543 N(-1.249) = 0.1059 N(-0.747) = 0.2276 Submit Io Attempt 1/3 for 10 pts. Part 2 What is N(-d2)? ON(-1.015) = 0.1551 ON(-1.371) = 0.0852 ON(-0.513) = 0.304 N(-1.743) = 0.0407 ON(-0.00911) = 0.496 ON(-0.963) = 0.1677 Submit Part 3 IB Attempt 1/8 for 10 pts. What should be the price (premium) of the put option? 1+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Brigham, Daves

10th Edition

978-1439051764, 1111783659, 9780324594690, 1439051763, 9781111783655, 324594690, 978-1111021573