Answered step by step

Verified Expert Solution

Question

1 Approved Answer

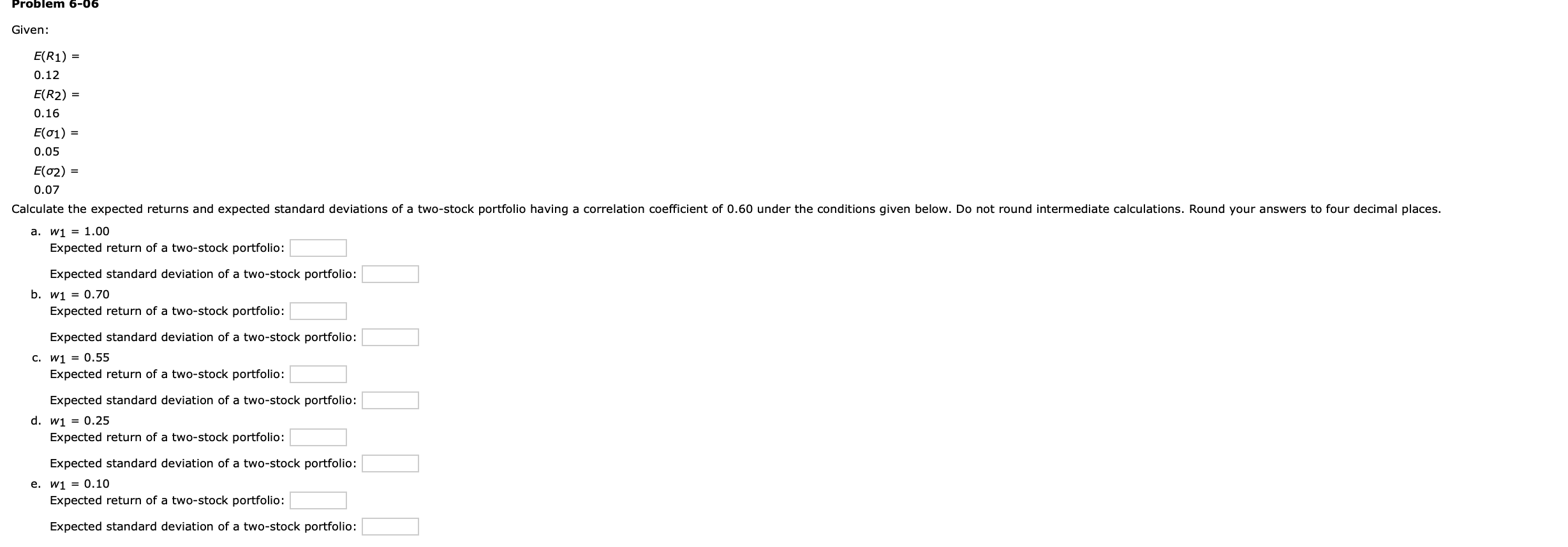

Problem 6-06 Given: E(R1) = 0.12 E(R2) = 0.16 E(01) = 0.05 E(02) = 0.07 Calculate the expected returns and expected standard deviations of a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Public, Health, And Not-for-Profit Organizations

Authors: Steven A. Finkler, Daniel L. Smith, Thad D. Calabrese, Robert M. Purtell

6th Edition

150639681X, 978-1506396811