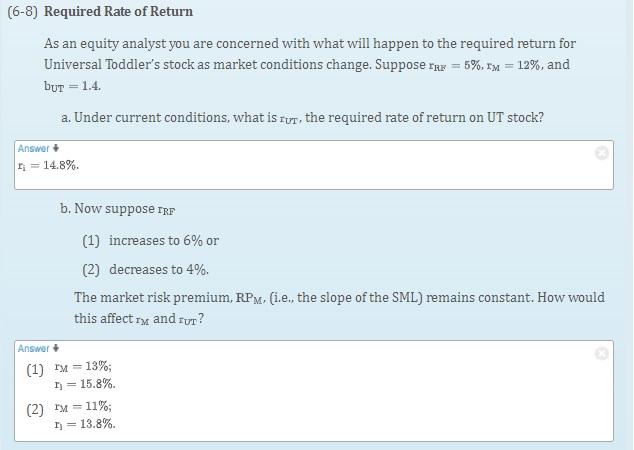

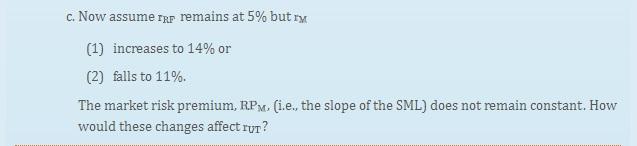

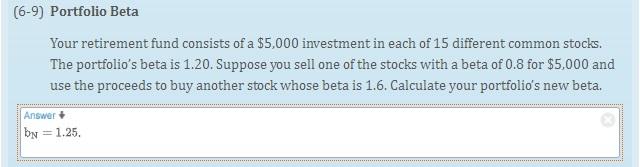

Question

Problem 6-9: You don't need to try to find a formula in the book; this is a problem of logic and proportion. You are given

- Problem 6-9: You don't need to try to find a formula in the book; this is a problem of logic and proportion. You are given three beta numbers. First set up an algebraic equation to determine the beta of the larger portion of the old portfolio (excluding the $5,000 portion sold at beta of 0.8); you will need to include the data on the sale of the $5,000 investment. Second, once you know the beta on the larger segment of the portfolio, you can calculate that weighted element and add the weighted element of the new stock with beta of 1.6. The result should be 1.25. You need to show the math.

Quantitative solutions can be used to check your work. But, you are expected to develop and show Excel formulas for these solutions. The path to the solution is where you will be evaluated. It is not acceptable to simply copy the answers.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management And Financial Institutions

Authors: John C. Hull

3rd Edition

1118269039, 9781118269039