Answered step by step

Verified Expert Solution

Question

1 Approved Answer

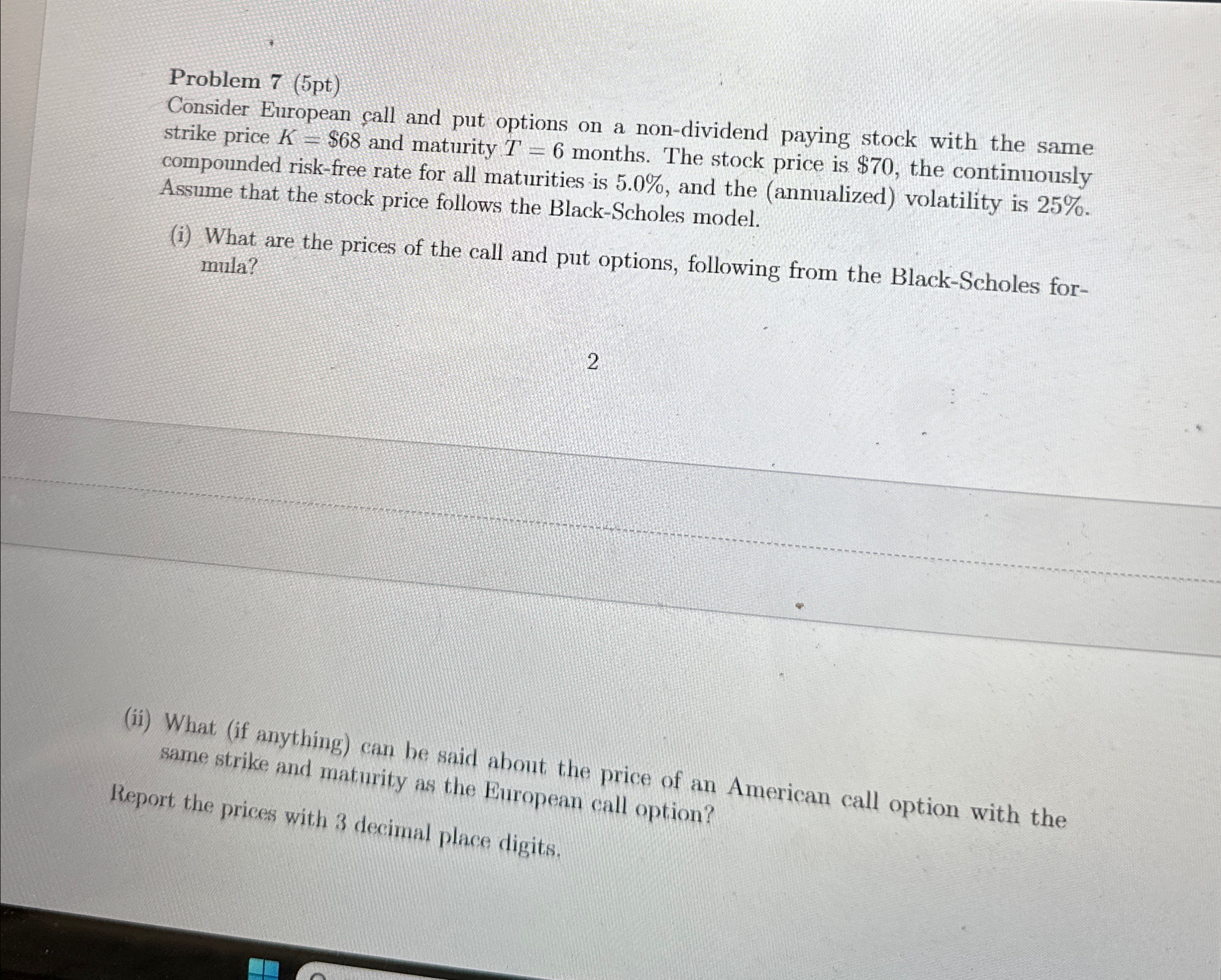

Problem 7 ( 5 pt ) Consider European call and put options on a non - dividend paying stock with the same strike price K

Problem pt

Consider European call and put options on a nondividend paying stock with the same strike price $ and maturity months. The stock price is $ the continuously compounded riskfree rate for all maturities is and the annualized volatility is Assume that the stock price follows the BlackScholes model.

i What are the prices of the call and put options, following from the BlackScholes formula?

ii What if anything can be said about the price of an American call option with the same strike and maturity as the European call option?

Report the prices with decimal place digits.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook On Corporate Governance In Financial Institutions

Authors: Christine A. Mallin

1st Edition

1784711780, 978-1784711788