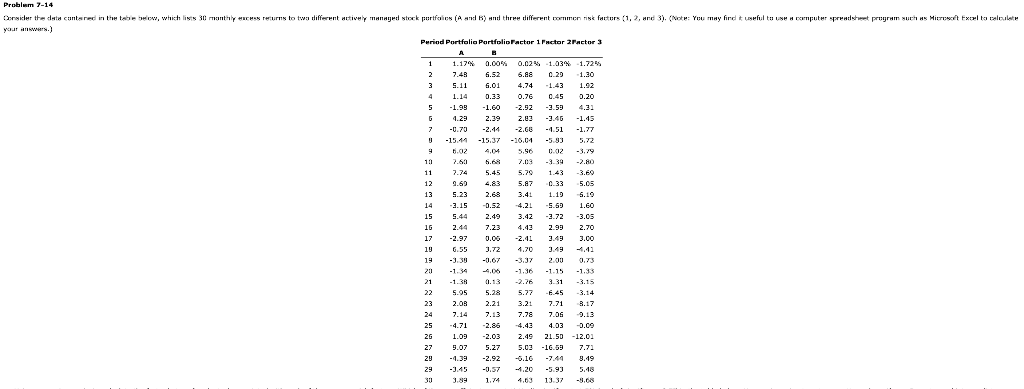

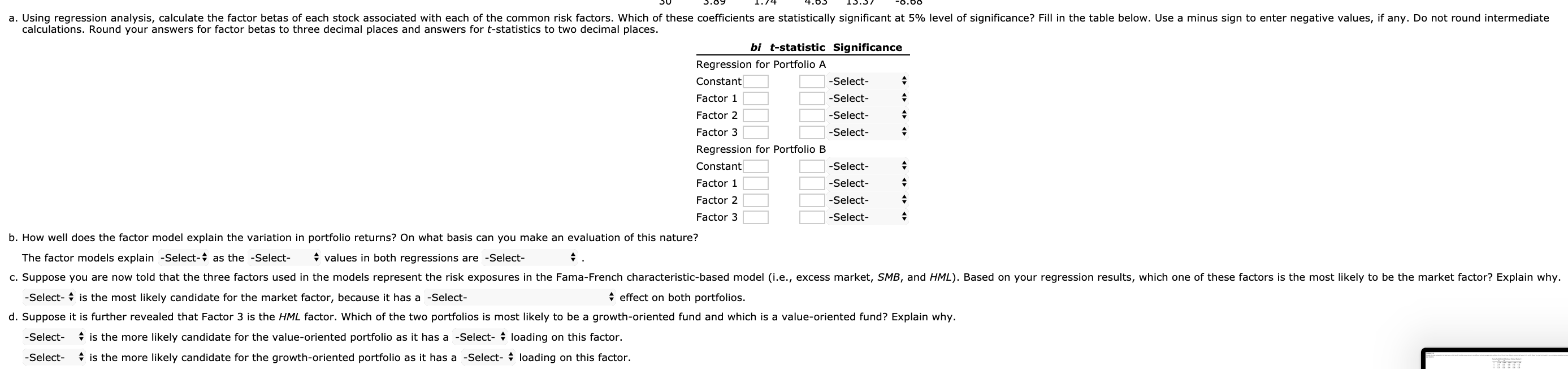

Problem 7-14 conter the ter , which I 111 to two different actively managed sterk pertfales ( A B ) had three different mo r nisk farturs {1, 2, and 3). (Note: You may find it useful to us het program ur HS HIETICE Kur the your w .) Period Portfolio PortfolioFactor 1 Factor 2Pactor 3 1 2 3 4 5 1.17% 0.00% 7 .436 .52 5.11 5.01 1.14 0.33 -1.99 -1.60 4 .29 2.39 -0.75 -2.14 -15.44 -15.37 0.02% 6.88 4.74 0.76 2.52 2.23 2.GB -10.04 1.03% 0.20 1.43 0.45 -3.59 -3.45 -4.51 -5.93 1.7295 1.30 1.92 0.20 4.31 -1.45 -1.77 5.72 5 7 9 10 7 .63 5.68 117.745 .45 12 9 .60 4.83 13 5.23 2.68 14 2 .15 -0.52 155 .44 2.49 15 2.44 7.23 17 -2.97 0.00 19 6.55 3 .72 19 -1.39 -0.67 21 -1.34 4.06 21 -1.38 0.13 22 5.05 5.28 232.082.21 24 7.14 7.13 25 -4.71 2.85 26 1.09 -2.03 27 9.07 5.27 29 -4.39 -2.92 29 -.45 -0.57 30 3.89 1.74 7.09 -3.39 -2.80 5.70 1.43 -3.60 5.87 0.33 5.05 3.41 1.10 5.19 4.21 5.59 1.60 3.422.72 -3.05 4.43 2.99 2.70 -2.41 3 .49 3.00 1.70 3.49 -1.11 -3.37 2 .00 0.73 -1.6 -1.25 -1.33 -2.76 3.31 -3.15 5.77 6.45 3.14 3.217 .71 3.17 7.78 7.05 9.13 4.42 4.03 0.09 2.49 21.50 -12.03 5.02 -16.59 7.72 -6.16 -7.44 9.19 1.20 -5.93 5.18 4.63 13.37 -3.68 50 5.09 1.74 4.65 15.57 -0.08 a. Using regression analysis, calculate the factor betas of each stock associated with each of the common risk factors. Which of these coefficients are statistically significant at 5% level of significance? Fill in the table below. Use a minus sign to enter negative values, if any. Do not round intermediate calculations. Round your answers for factor betas to three decimal places and answers for t-statistics to two decimal places. bi t-statistic Significance Regression for Portfolio A Constant -Select- Factor 1 -Select- Factor 2 -Select- Factor 3 -Select- Regression for Portfolio B Constant -Select- Factor 1 -Select- Factor 2 -Select- Factor 3 -Select- b. How well does the factor model explain the variation in portfolio returns? On what basis can you make an evaluation of this nature? The factor models explain -Select-4 as the -Select- values in both regressions are -Select- 4. c. Suppose you are now told that the three factors used in the models represent the risk exposures in the Fama-French characteristic-based model (i.e., excess market, SMB, and HML). Based on your regression results, which one of these factors is the most likely to be the market factor? Explain why. -Select- is the most likely candidate for the market factor, because it has a -Select- effect on both portfolios. d. Suppose it is further revealed that Factor 3 is the HML factor. Which of the two portfolios is most likely to be a growth-oriented fund and which is a value-oriented fund? Explain why. -Select- is the more likely candidate for the value-oriented portfolio as it has a -Select- loading on this factor. -Select- is the more likely candidate for the growth-oriented portfolio as it has a -Select- loading on this factor. Problem 7-14 conter the ter , which I 111 to two different actively managed sterk pertfales ( A B ) had three different mo r nisk farturs {1, 2, and 3). (Note: You may find it useful to us het program ur HS HIETICE Kur the your w .) Period Portfolio PortfolioFactor 1 Factor 2Pactor 3 1 2 3 4 5 1.17% 0.00% 7 .436 .52 5.11 5.01 1.14 0.33 -1.99 -1.60 4 .29 2.39 -0.75 -2.14 -15.44 -15.37 0.02% 6.88 4.74 0.76 2.52 2.23 2.GB -10.04 1.03% 0.20 1.43 0.45 -3.59 -3.45 -4.51 -5.93 1.7295 1.30 1.92 0.20 4.31 -1.45 -1.77 5.72 5 7 9 10 7 .63 5.68 117.745 .45 12 9 .60 4.83 13 5.23 2.68 14 2 .15 -0.52 155 .44 2.49 15 2.44 7.23 17 -2.97 0.00 19 6.55 3 .72 19 -1.39 -0.67 21 -1.34 4.06 21 -1.38 0.13 22 5.05 5.28 232.082.21 24 7.14 7.13 25 -4.71 2.85 26 1.09 -2.03 27 9.07 5.27 29 -4.39 -2.92 29 -.45 -0.57 30 3.89 1.74 7.09 -3.39 -2.80 5.70 1.43 -3.60 5.87 0.33 5.05 3.41 1.10 5.19 4.21 5.59 1.60 3.422.72 -3.05 4.43 2.99 2.70 -2.41 3 .49 3.00 1.70 3.49 -1.11 -3.37 2 .00 0.73 -1.6 -1.25 -1.33 -2.76 3.31 -3.15 5.77 6.45 3.14 3.217 .71 3.17 7.78 7.05 9.13 4.42 4.03 0.09 2.49 21.50 -12.03 5.02 -16.59 7.72 -6.16 -7.44 9.19 1.20 -5.93 5.18 4.63 13.37 -3.68 50 5.09 1.74 4.65 15.57 -0.08 a. Using regression analysis, calculate the factor betas of each stock associated with each of the common risk factors. Which of these coefficients are statistically significant at 5% level of significance? Fill in the table below. Use a minus sign to enter negative values, if any. Do not round intermediate calculations. Round your answers for factor betas to three decimal places and answers for t-statistics to two decimal places. bi t-statistic Significance Regression for Portfolio A Constant -Select- Factor 1 -Select- Factor 2 -Select- Factor 3 -Select- Regression for Portfolio B Constant -Select- Factor 1 -Select- Factor 2 -Select- Factor 3 -Select- b. How well does the factor model explain the variation in portfolio returns? On what basis can you make an evaluation of this nature? The factor models explain -Select-4 as the -Select- values in both regressions are -Select- 4. c. Suppose you are now told that the three factors used in the models represent the risk exposures in the Fama-French characteristic-based model (i.e., excess market, SMB, and HML). Based on your regression results, which one of these factors is the most likely to be the market factor? Explain why. -Select- is the most likely candidate for the market factor, because it has a -Select- effect on both portfolios. d. Suppose it is further revealed that Factor 3 is the HML factor. Which of the two portfolios is most likely to be a growth-oriented fund and which is a value-oriented fund? Explain why. -Select- is the more likely candidate for the value-oriented portfolio as it has a -Select- loading on this factor. -Select- is the more likely candidate for the growth-oriented portfolio as it has a -Select- loading on this factor