Answered step by step

Verified Expert Solution

Question

1 Approved Answer

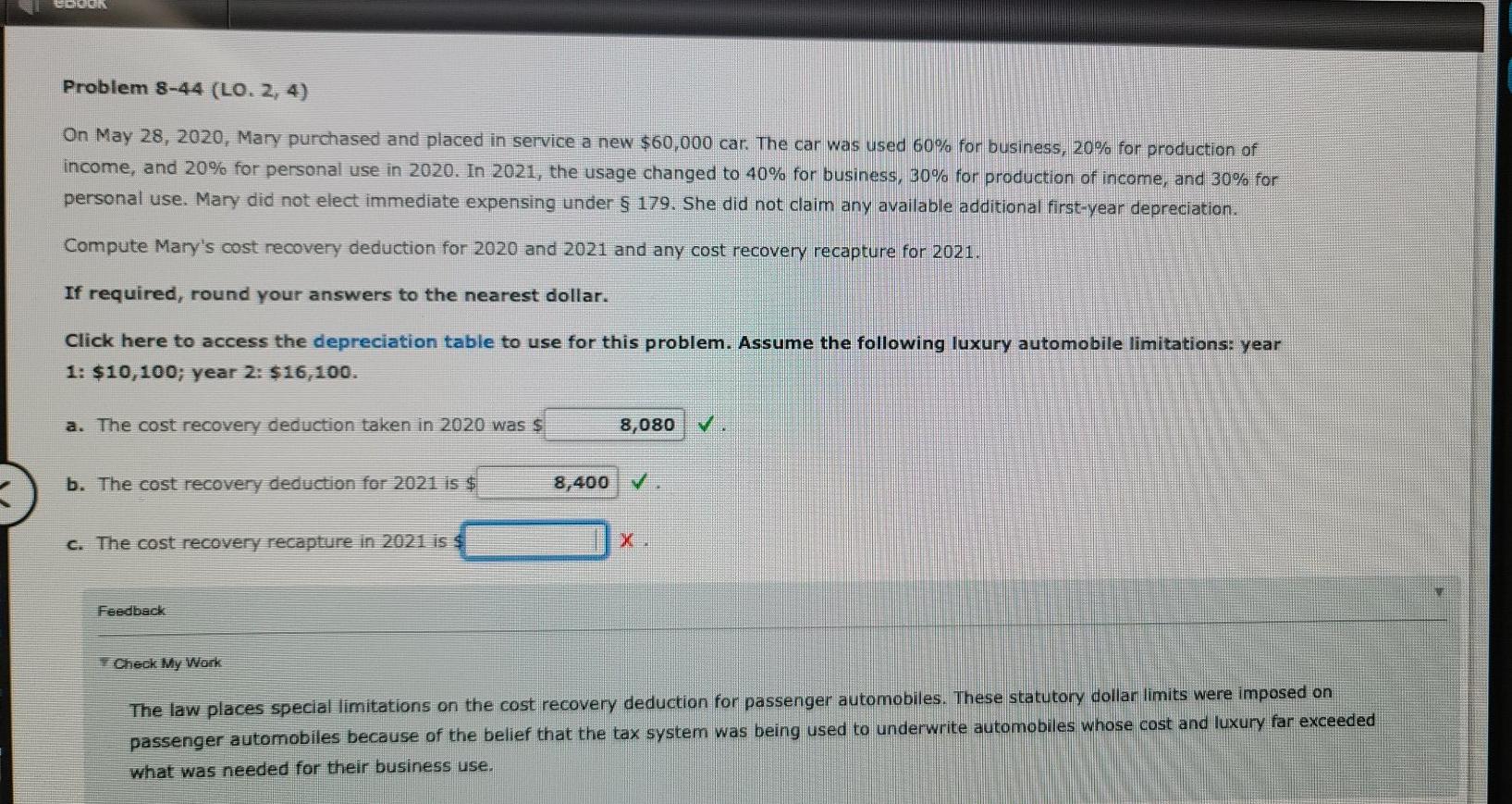

Problem 8-44 (LO. 2, 4) On May 28, 2020, Mary purchased and placed in service a new $60,000 car. The car was used 60% for

Problem 8-44 (LO. 2, 4) On May 28, 2020, Mary purchased and placed in service a new $60,000 car. The car was used 60% for business, 20% for production of income, and 20% for personal use in 2020. In 2021, the usage changed to 40% for business, 30% for production of income, and 30% for personal use. Mary did not elect immediate expensing under $ 179. She did not claim any available additional first-year depreciation. Compute Mary's cost recovery deduction for 2020 and 2021 and any cost recovery recapture for 2021. If required, round your answers to the nearest dollar. Click here to access the depreciation table to use for this problem. Assume the following luxury automobile limitations: year 1: $10,100; year 2: $16,100. a. The cost recovery deduction taken in 2020 was $ 8,080 V b. The cost recovery deduction for 2021 is $ 8,400 V C. The cost recovery recapture in 2021 is $ Feedback Check My Work The law places special limitations on the cost recovery deduction for passenger automobiles. These statutory dollar limits were imposed on passenger automobiles because of the belief that the tax system was being used to underwrite automobiles whose cost and luxury far exceeded what was needed for their business use. Problem 8-44 (LO. 2, 4) On May 28, 2020, Mary purchased and placed in service a new $60,000 car. The car was used 60% for business, 20% for production of income, and 20% for personal use in 2020. In 2021, the usage changed to 40% for business, 30% for production of income, and 30% for personal use. Mary did not elect immediate expensing under $ 179. She did not claim any available additional first-year depreciation. Compute Mary's cost recovery deduction for 2020 and 2021 and any cost recovery recapture for 2021. If required, round your answers to the nearest dollar. Click here to access the depreciation table to use for this problem. Assume the following luxury automobile limitations: year 1: $10,100; year 2: $16,100. a. The cost recovery deduction taken in 2020 was $ 8,080 V b. The cost recovery deduction for 2021 is $ 8,400 V C. The cost recovery recapture in 2021 is $ Feedback Check My Work The law places special limitations on the cost recovery deduction for passenger automobiles. These statutory dollar limits were imposed on passenger automobiles because of the belief that the tax system was being used to underwrite automobiles whose cost and luxury far exceeded what was needed for their business use

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

IT Auditing And Sarbanes Oxley Compliance Key Strategies For Business Improvement

Authors: Dimitris N. Chorafas

1st Edition

036738650X, 978-0367386504