Answered step by step

Verified Expert Solution

Question

1 Approved Answer

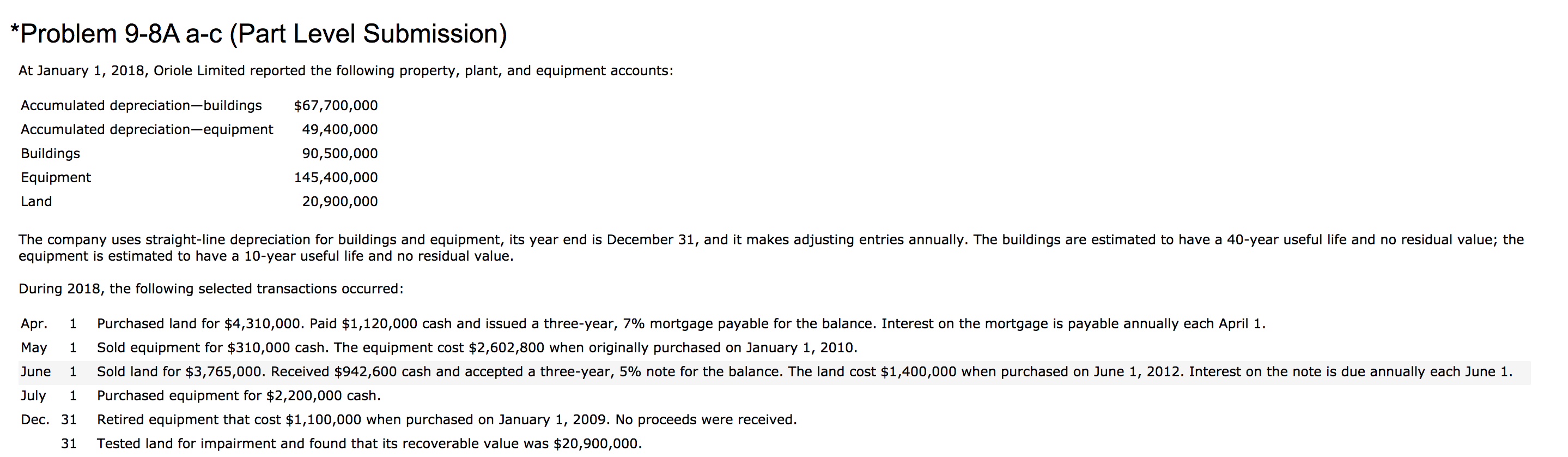

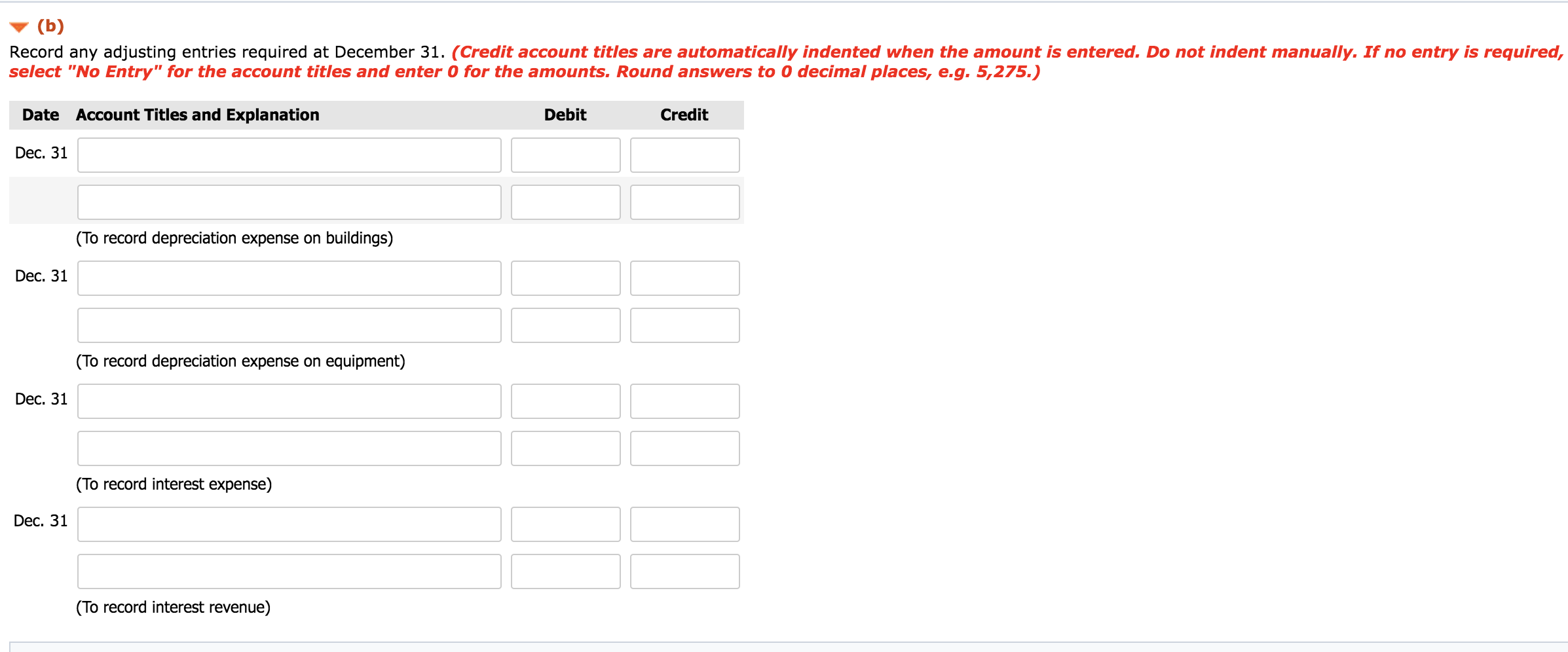

Problem 9-8A a-c (Part Level Submission) At January 1, 2018, Oriole Limited reported the following property, plant, and equipment accounts: Accumulated depreciation-buildings $67,700,000 Accumulated depreciation-equipment

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Charles T. Horngren, Walter T. Harrison Jr., M. Suzanne Oliv

9th Edition

130898414, 9780132997379, 978-0130898418, 132997371, 978-0132569309