Answered step by step

Verified Expert Solution

Question

1 Approved Answer

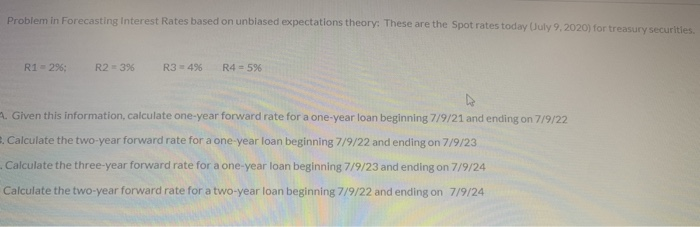

Problem in Forecasting Interest Rates based on unblased expectations theory: These are the Spot rates today (July 9, 2020) for treasury securities. R1 - 296;

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Managerial Accounting Working Papers Volume 1

Authors: Belverd E. Needles

6th Edition

0618102337, 978-0618102334