Answered step by step

Verified Expert Solution

Question

1 Approved Answer

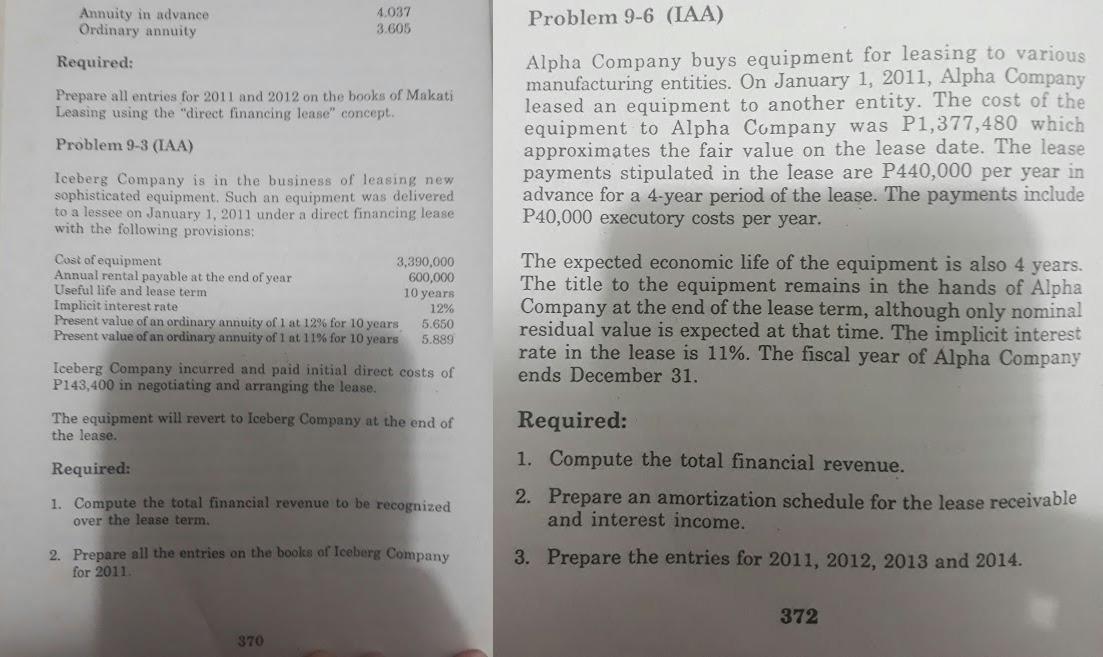

Problems 9-3 and 9-6 Annuity in advance 4,037 Problem 9-6 (LAA) Ordinary annuity 3.605 Required: Alpha Company buys equipment for leasing to various manufacturing entities.

Problems 9-3 and 9-6

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting And Analysis

Authors: Lawrence Revsine, Daniel Collins

4th Edition

0073527092, 978-0073527093