Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Process Cost Accounting. Mini practice set two. 1 Process Cost Accounting In this practice set you will apply the techniques and principles of process cost

Process Cost Accounting. Mini practice set two.

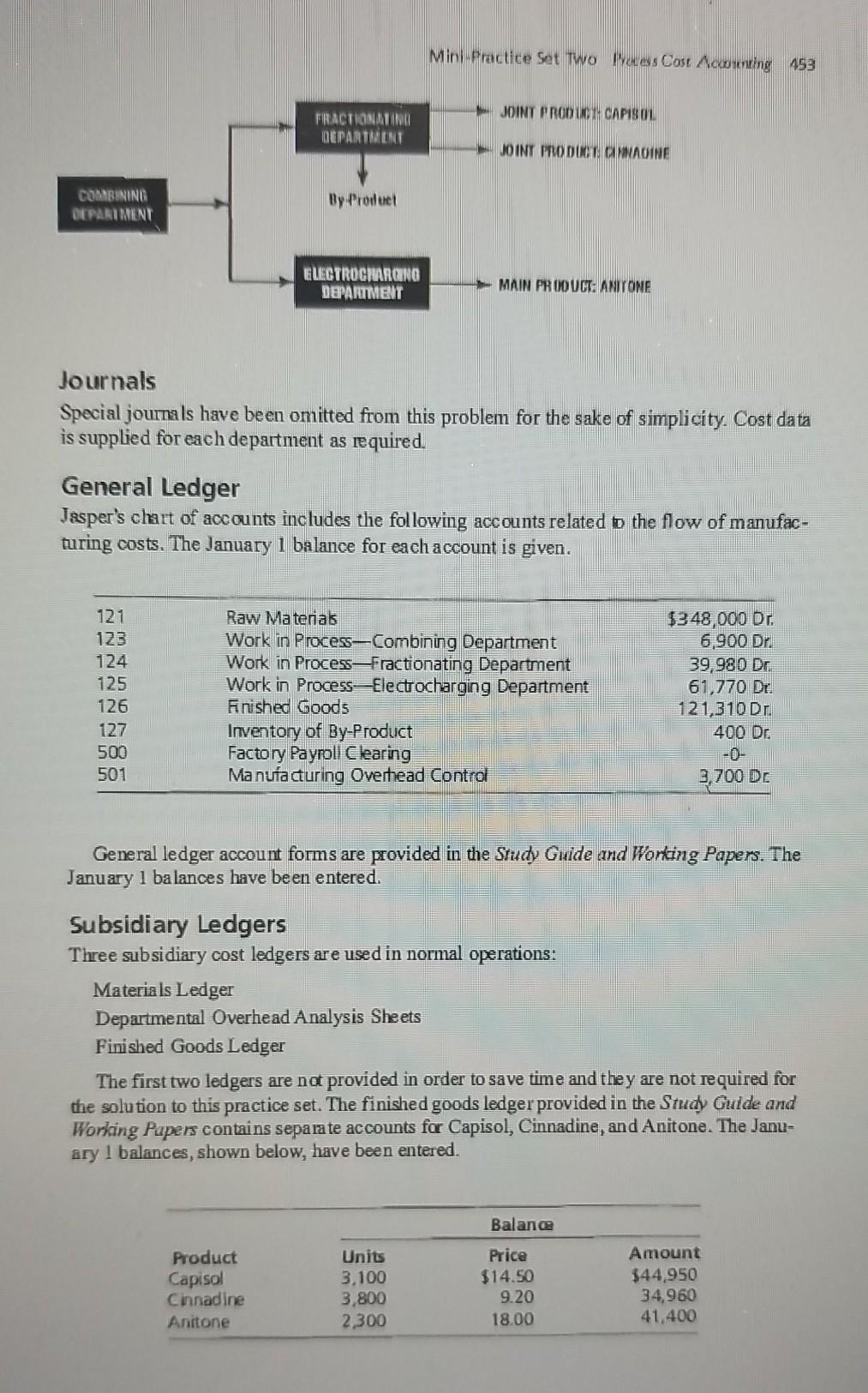

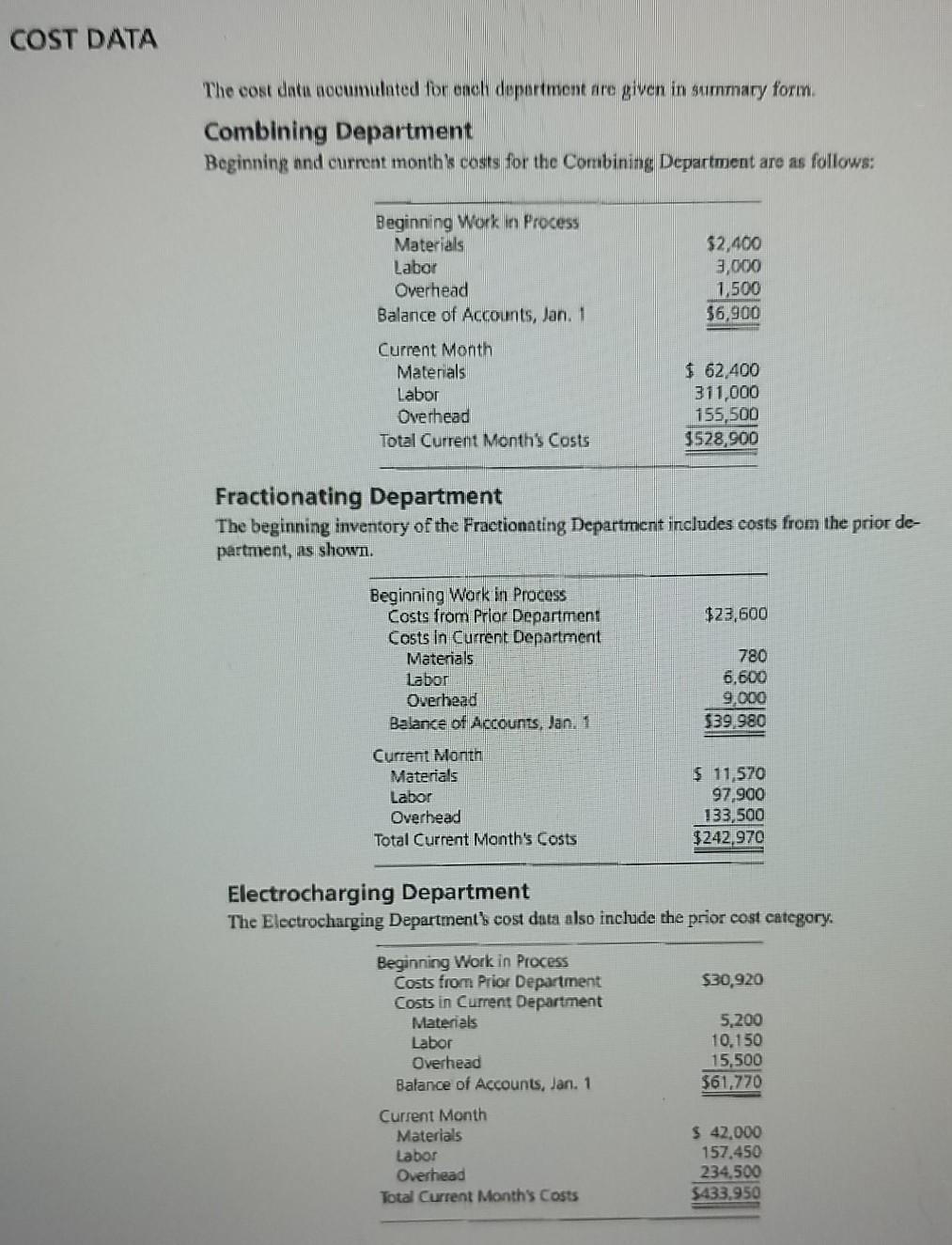

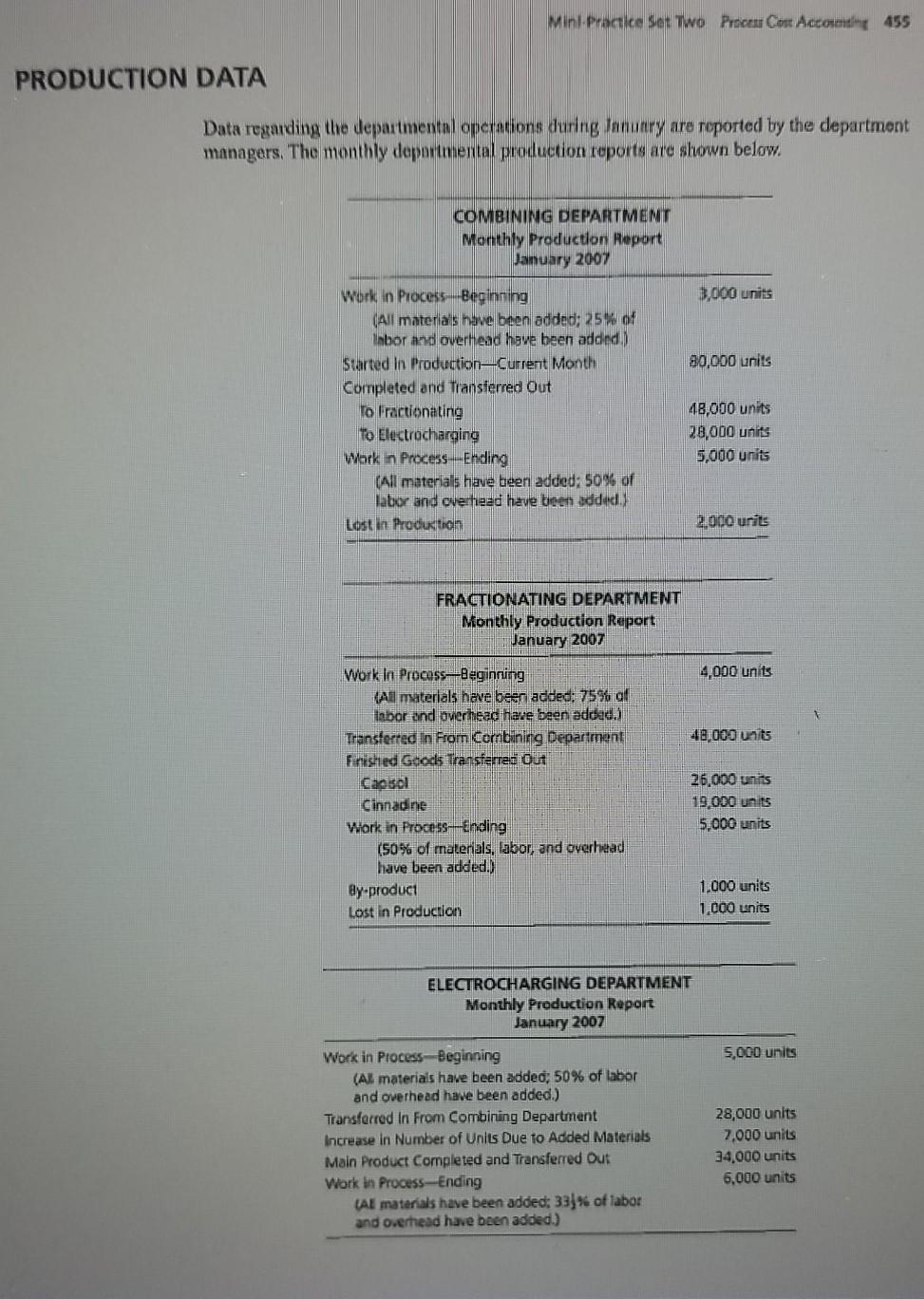

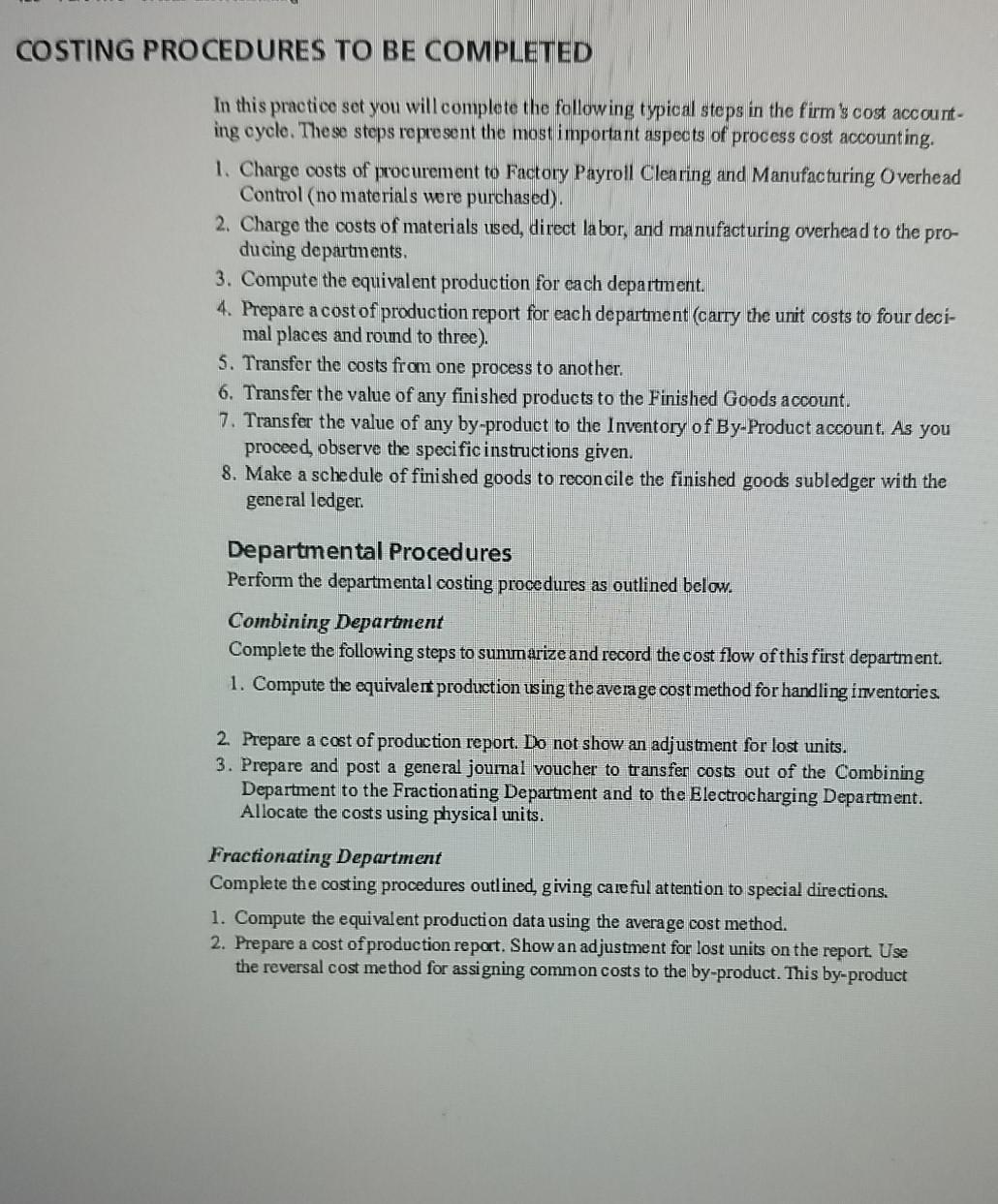

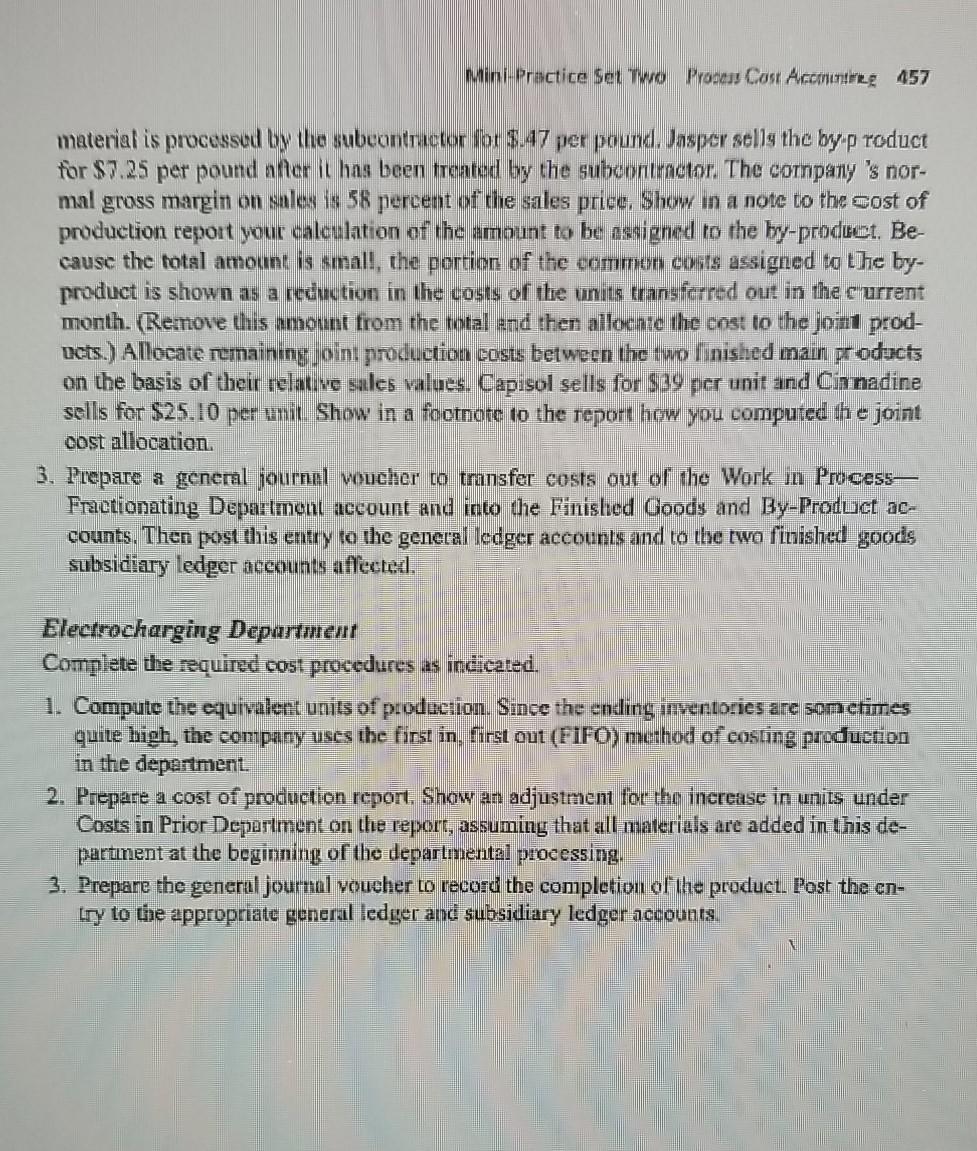

1 Process Cost Accounting In this practice set you will apply the techniques and principles of process cost accounting to record and summarize the flow of costs connected with the Jasper Chemical Corporation for the month of January. In completing the project, you will make postings to the general ledger accounts to record materials used, labor costs incurred, and manufacturing overhead costs. You will also compute equivalent production and complete the cost of production reports for pro- ducing departments. Then you will make entries to record the transfers of costs between de- partments, the recovery of a by-product, and the transfers of finished products from the final work in process inventory accounts to finished goods. However, in the interest of time you will not be required to make many of the routine entries to record costs, which you have learned to do in prior chapters. The practice set is designed to reinforce your knowledge of the essential elements of process cost accounting without the time-consuming work of detailed bookkeep- ing that would be required to record and post entries for many individual transactions. JASPER CHEMICAL CORPORATION Jasper Chemical Corporation manufactures three main products. The continuous produc- tion starts in the Combining Department where chemicals are mixed and processed. Some of the mixture is transferred to the Fractionating Department and the remainder to the Elec- trocharging Department. In the Fractionating Department, materials are added and the mixture is further processed. Two finished products, Capisol and Cinnadine, are obtained and, on completion, are transferred to a refrigerated storeroom. A by-product material is also removed. It is col- lected and stored in bins. Periodically this material is sent to a subcontractor who processes it and returns it to Jasper for sale. The chemicals transferred from the Combining Department to the Electrocharging De- partment also receive additional materials and further processing. In the process, an in- crease in units occurs. The finished product, Anitone, is transferred to a heated storeroom when it is completed. The manufacturing flow is summarized by the diagram on page 453. JASPER'S COST ACCOUNTING SYSTEM 452 Mini Practice Set Two las Cost Auwing 453 JOINT PRODUCT CAPISOL FRACTIONAT DEPARTMENT JOINT PRODUCT CAOINE COLARINING DEPARTMENT By Product ELECTROCHARCINO DEPARTMENT MAIN PRODUCT: ANITONE Journals Special journals have been omitted from this problem for the sake of simplicity. Cost data is supplied for each department as required. General Ledger Jasper's chart of accounts includes the following accounts related o the flow of manufac- turing costs. The January 1 balance for each account is given. 121 123 124 125 126 127 500 501 Raw Materas Work in Process-Combining Department Work in Process Fractionating Department Work in Process Electrocharging Department Finished Goods Inventory of By-Product Factory Payroll Clearing Manufacturing Overhead Control $348,000 Dr. 6,900 Dr. 39.980 Dr. 61,770 Dr. 121,310 Dr. 400 Dr. 3700 DI General ledger account forms are provided in the Study Guide and Working Papers. The January 1 balances have been entered. Subsidiary Ledgers Three subsidiary cost ledgers are used in normal operations: Materia ls Ledger Departmental Overhead Analysis Sheets Finished Goods Ledger The first two ledgers are not provided in order to save time and they are not required for the solution to this practice set. The finished goods ledger provided in the Study Guide and Working Papers contains separate accounts for Capisol, Cinnadine, and Anitone. The Janu- ary 1 balances, shown below, have been entered. Balance Product Capisol Cinnadine Anitone Units 3.100 3,800 2,300 Price $14.50 9.20 18.00 Amount $44,950 34,960 41,400 COST DATA The cost data accumulated for ench department are given in summary form Combining Department Beginning and current month's costs for the Combining Department are as follows: $2,400 3,000 1,500 $6,900 Beginning Work in Process Materials Labor Overhead Balance of Accounts, Jan. 1 Current Month Materials Labor Overhead Total Current Month's Costs $ 62,400 311,000 155,500 $528,900 Fractionating Department The beginning inventory of the Fractionating Department includes costs from the prior de- partment, as shown. $23,600 Beginning Work in Process Costs from Prior Department Cests in Current Department Materials Labor Overhead Balance of Accounts, Jan. 1 780 6.600 9,000 $39,980 Current Month Materials Labor Overhead Total Current Month's Costs $ 11,570 97,900 133,500 $242,970 Electrocharging Department The Electrocharging Departments cost data also include the prior cost category. $30,920 Beginning Work in Process Costs from Prior Department Costs in Current Department Materials Labor Overhead Balance of Accounts, Jan. 1 Current Month Materials Labor Overhead Total Current Month's Costs 5,200 10.150 15,500 $61,770 $ 42,000 157,450 234,500 $433.950 Mini-Practice Set Two Process Cost Accounthe 455 PRODUCTION DATA Data regarding the departmental operations during January are reported by the department managers. The monthly deportmental production reports are shown below. COMBINING DEPARTMENT Monthly Production Report January 2007 3,000 units 80,000 units Work In Process -Beginning (All materials have been added: 25% of Isbor and overhead have been added. Started in Production Current Month Completed and Transferred Out To Fractionating To Electrocharging Work in Process --Ending (All materials have been added: 50% of labor and overhead have been added.) Lost in Produktion 48,000 units 28,000 units 5,000 units 2.000 units FRACTIONATING DEPARTMENT Monthly Production Report January 2007 4,000 units 49,000 units Work In Process Beginning All materials have been added: 7556 al labor and overhead have been added.) Transferred In From Combining Department Finished Goods Transferred Out Caoisol Cinnadine Work in Process Ending (50% of materials, labor, and overhead have been added.) By-product Lost in Production 26,000 units 19,000 units 5,000 units 1.000 units 1.000 units 5,000 units ELECTROCHARGING DEPARTMENT Monthly Production Report January 2007 Work in Process Beginning (Al materials have been added, 50% of labor and overhead have been added.) Transferred In From Combining Department Increase in Number of Units Due to Added Materials Main Product Completed and Transferred Out Work in Process Ending (Al materials have been added: 33% of labor and overhead have been added.) 28,000 units 7,000 units 34,000 units 6,000 units COSTING PROCEDURES TO BE COMPLETED In this practice set you will complete the following typical steps in the firm's cost account ing cycle. These steps represent the most important aspects of process cost accounting. 1. Charge costs of procurement to Factory Payroll Clearing and Manufacturing Overhead Control (no materials were purchased). 2. Charge the costs of materials used, direct labor, and manufacturing overhead to the pro- ducing departments 3. Compute the equivalent production for cach department. 4. Prepare a costof production report for each department (carry the unit costs to four deci- mal places and round to three). 5. Transfer the costs from one process to another. 6. Transfer the value of any finished products to the Finished Goods account. 7. Transfer the value of any by-product to the Inventory of By-Product account. As you proceed, observe the specific instructions given. 8. Make a schedule of finished goods to reconcile the finished goods subledger with the general ledger Departmental Procedures Perform the departmental costing procedures as outlined below. Combining Department Complete the following steps to summarize and record the cost flow of this first department. 1. Compute the equivalent production using the average cost method for handling inventories. 2. Prepare a cost of production report. Do not show an adjustment for lost units. 3. Prepare and post a general journal voucher to transfer costs out of the Combining Department to the Fractionating Department and to the Electrocharging Department. Allocate the costs using physical units. Fractionating Department Complete the costing procedures outlined, giving careful attention to special directions. 1. Compute the equivalent production data using the average cost method. 2. Prepare a cost of production report. Show an adjustment for lost units on the report. Use the reversal cost method for assigning common costs to the by-product. This by-product Mini-Practice Set Two Process Cost Acomtheg 457 material is processed by the subcontractor for $.47 per pound. Jasper sells the by-product for $7.25 per pound after it has been treated by the subcontractor. The company 's nor- mal gross margin on sales is 58 percent of the sales price. Show in a note to the cost of production report your calculation of the amount to be assigned to the by-product. Be cause the total amount is small, the portion of the common costs assigned to the by- product is shown as a reduction in the costs of the units transferred out in the current month. (Remove this amount from the total and then allocate the cost to the joint prod- ucts.) Allocate remaining joini production costs between the two finished main products on the basis of their relative sules values. Capisol sells for $39 per unit and Cinnadine sells for $25.10 per umit Show in a foctrote to the report how you computed the joint cost allocation. 3. Prepare a general journal voucher to transfer costs out of the Work in Process- Fractionating Deparlment account and into the Finished Goods and By-Product ac- counts. Then post this entry to the general ledger accounts and to the two finished goods subsidiary ledger accounts affected. Electrocharging Department Complete the required cost procedures as indicated. 1. Compute the equivalent units of production. Since the ending inventories are sometimes quite high, the company uses the first in, first out (FIFO) method of costing production in the department 2. Prepare a cost of production report. Show an adjustment for the increase in units under Costs in Prior Department on the report, assuming that all materials are added in this de- partiment at the beginning of the departmental processing. 3. Prepare the general journal voucher to record the completion of the product. Post the en- try to the appropriate general ledger and subsidiary ledger accounts. 1 Process Cost Accounting In this practice set you will apply the techniques and principles of process cost accounting to record and summarize the flow of costs connected with the Jasper Chemical Corporation for the month of January. In completing the project, you will make postings to the general ledger accounts to record materials used, labor costs incurred, and manufacturing overhead costs. You will also compute equivalent production and complete the cost of production reports for pro- ducing departments. Then you will make entries to record the transfers of costs between de- partments, the recovery of a by-product, and the transfers of finished products from the final work in process inventory accounts to finished goods. However, in the interest of time you will not be required to make many of the routine entries to record costs, which you have learned to do in prior chapters. The practice set is designed to reinforce your knowledge of the essential elements of process cost accounting without the time-consuming work of detailed bookkeep- ing that would be required to record and post entries for many individual transactions. JASPER CHEMICAL CORPORATION Jasper Chemical Corporation manufactures three main products. The continuous produc- tion starts in the Combining Department where chemicals are mixed and processed. Some of the mixture is transferred to the Fractionating Department and the remainder to the Elec- trocharging Department. In the Fractionating Department, materials are added and the mixture is further processed. Two finished products, Capisol and Cinnadine, are obtained and, on completion, are transferred to a refrigerated storeroom. A by-product material is also removed. It is col- lected and stored in bins. Periodically this material is sent to a subcontractor who processes it and returns it to Jasper for sale. The chemicals transferred from the Combining Department to the Electrocharging De- partment also receive additional materials and further processing. In the process, an in- crease in units occurs. The finished product, Anitone, is transferred to a heated storeroom when it is completed. The manufacturing flow is summarized by the diagram on page 453. JASPER'S COST ACCOUNTING SYSTEM 452 Mini Practice Set Two las Cost Auwing 453 JOINT PRODUCT CAPISOL FRACTIONAT DEPARTMENT JOINT PRODUCT CAOINE COLARINING DEPARTMENT By Product ELECTROCHARCINO DEPARTMENT MAIN PRODUCT: ANITONE Journals Special journals have been omitted from this problem for the sake of simplicity. Cost data is supplied for each department as required. General Ledger Jasper's chart of accounts includes the following accounts related o the flow of manufac- turing costs. The January 1 balance for each account is given. 121 123 124 125 126 127 500 501 Raw Materas Work in Process-Combining Department Work in Process Fractionating Department Work in Process Electrocharging Department Finished Goods Inventory of By-Product Factory Payroll Clearing Manufacturing Overhead Control $348,000 Dr. 6,900 Dr. 39.980 Dr. 61,770 Dr. 121,310 Dr. 400 Dr. 3700 DI General ledger account forms are provided in the Study Guide and Working Papers. The January 1 balances have been entered. Subsidiary Ledgers Three subsidiary cost ledgers are used in normal operations: Materia ls Ledger Departmental Overhead Analysis Sheets Finished Goods Ledger The first two ledgers are not provided in order to save time and they are not required for the solution to this practice set. The finished goods ledger provided in the Study Guide and Working Papers contains separate accounts for Capisol, Cinnadine, and Anitone. The Janu- ary 1 balances, shown below, have been entered. Balance Product Capisol Cinnadine Anitone Units 3.100 3,800 2,300 Price $14.50 9.20 18.00 Amount $44,950 34,960 41,400 COST DATA The cost data accumulated for ench department are given in summary form Combining Department Beginning and current month's costs for the Combining Department are as follows: $2,400 3,000 1,500 $6,900 Beginning Work in Process Materials Labor Overhead Balance of Accounts, Jan. 1 Current Month Materials Labor Overhead Total Current Month's Costs $ 62,400 311,000 155,500 $528,900 Fractionating Department The beginning inventory of the Fractionating Department includes costs from the prior de- partment, as shown. $23,600 Beginning Work in Process Costs from Prior Department Cests in Current Department Materials Labor Overhead Balance of Accounts, Jan. 1 780 6.600 9,000 $39,980 Current Month Materials Labor Overhead Total Current Month's Costs $ 11,570 97,900 133,500 $242,970 Electrocharging Department The Electrocharging Departments cost data also include the prior cost category. $30,920 Beginning Work in Process Costs from Prior Department Costs in Current Department Materials Labor Overhead Balance of Accounts, Jan. 1 Current Month Materials Labor Overhead Total Current Month's Costs 5,200 10.150 15,500 $61,770 $ 42,000 157,450 234,500 $433.950 Mini-Practice Set Two Process Cost Accounthe 455 PRODUCTION DATA Data regarding the departmental operations during January are reported by the department managers. The monthly deportmental production reports are shown below. COMBINING DEPARTMENT Monthly Production Report January 2007 3,000 units 80,000 units Work In Process -Beginning (All materials have been added: 25% of Isbor and overhead have been added. Started in Production Current Month Completed and Transferred Out To Fractionating To Electrocharging Work in Process --Ending (All materials have been added: 50% of labor and overhead have been added.) Lost in Produktion 48,000 units 28,000 units 5,000 units 2.000 units FRACTIONATING DEPARTMENT Monthly Production Report January 2007 4,000 units 49,000 units Work In Process Beginning All materials have been added: 7556 al labor and overhead have been added.) Transferred In From Combining Department Finished Goods Transferred Out Caoisol Cinnadine Work in Process Ending (50% of materials, labor, and overhead have been added.) By-product Lost in Production 26,000 units 19,000 units 5,000 units 1.000 units 1.000 units 5,000 units ELECTROCHARGING DEPARTMENT Monthly Production Report January 2007 Work in Process Beginning (Al materials have been added, 50% of labor and overhead have been added.) Transferred In From Combining Department Increase in Number of Units Due to Added Materials Main Product Completed and Transferred Out Work in Process Ending (Al materials have been added: 33% of labor and overhead have been added.) 28,000 units 7,000 units 34,000 units 6,000 units COSTING PROCEDURES TO BE COMPLETED In this practice set you will complete the following typical steps in the firm's cost account ing cycle. These steps represent the most important aspects of process cost accounting. 1. Charge costs of procurement to Factory Payroll Clearing and Manufacturing Overhead Control (no materials were purchased). 2. Charge the costs of materials used, direct labor, and manufacturing overhead to the pro- ducing departments 3. Compute the equivalent production for cach department. 4. Prepare a costof production report for each department (carry the unit costs to four deci- mal places and round to three). 5. Transfer the costs from one process to another. 6. Transfer the value of any finished products to the Finished Goods account. 7. Transfer the value of any by-product to the Inventory of By-Product account. As you proceed, observe the specific instructions given. 8. Make a schedule of finished goods to reconcile the finished goods subledger with the general ledger Departmental Procedures Perform the departmental costing procedures as outlined below. Combining Department Complete the following steps to summarize and record the cost flow of this first department. 1. Compute the equivalent production using the average cost method for handling inventories. 2. Prepare a cost of production report. Do not show an adjustment for lost units. 3. Prepare and post a general journal voucher to transfer costs out of the Combining Department to the Fractionating Department and to the Electrocharging Department. Allocate the costs using physical units. Fractionating Department Complete the costing procedures outlined, giving careful attention to special directions. 1. Compute the equivalent production data using the average cost method. 2. Prepare a cost of production report. Show an adjustment for lost units on the report. Use the reversal cost method for assigning common costs to the by-product. This by-product Mini-Practice Set Two Process Cost Acomtheg 457 material is processed by the subcontractor for $.47 per pound. Jasper sells the by-product for $7.25 per pound after it has been treated by the subcontractor. The company 's nor- mal gross margin on sales is 58 percent of the sales price. Show in a note to the cost of production report your calculation of the amount to be assigned to the by-product. Be cause the total amount is small, the portion of the common costs assigned to the by- product is shown as a reduction in the costs of the units transferred out in the current month. (Remove this amount from the total and then allocate the cost to the joint prod- ucts.) Allocate remaining joini production costs between the two finished main products on the basis of their relative sules values. Capisol sells for $39 per unit and Cinnadine sells for $25.10 per umit Show in a foctrote to the report how you computed the joint cost allocation. 3. Prepare a general journal voucher to transfer costs out of the Work in Process- Fractionating Deparlment account and into the Finished Goods and By-Product ac- counts. Then post this entry to the general ledger accounts and to the two finished goods subsidiary ledger accounts affected. Electrocharging Department Complete the required cost procedures as indicated. 1. Compute the equivalent units of production. Since the ending inventories are sometimes quite high, the company uses the first in, first out (FIFO) method of costing production in the department 2. Prepare a cost of production report. Show an adjustment for the increase in units under Costs in Prior Department on the report, assuming that all materials are added in this de- partiment at the beginning of the departmental processing. 3. Prepare the general journal voucher to record the completion of the product. Post the en- try to the appropriate general ledger and subsidiary ledger accountsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Practitioners Guide To Edp Auditing

Authors: Jack Mullen

1st Edition

0136912621, 978-0136912620