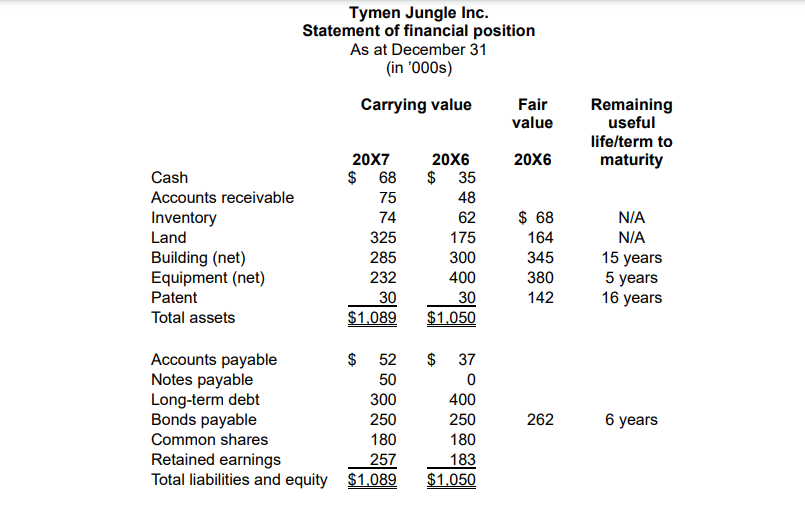

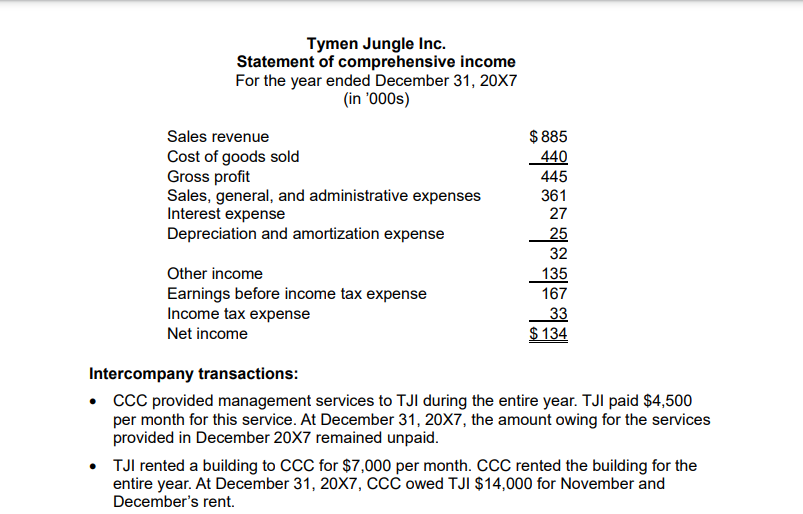

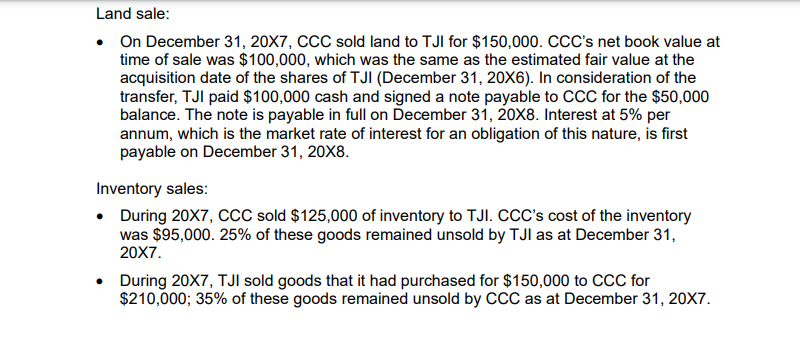

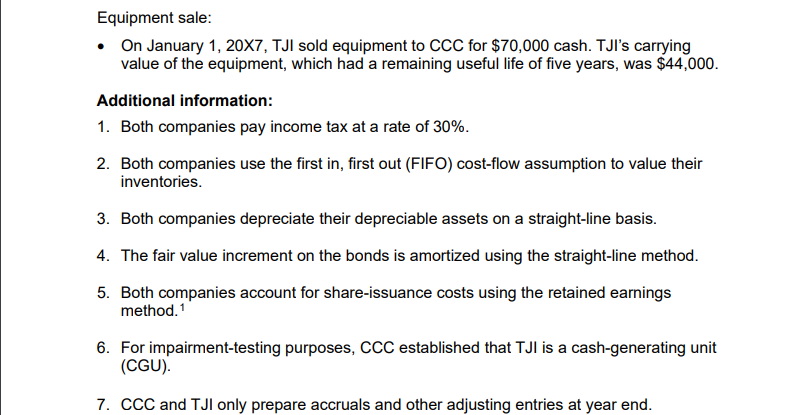

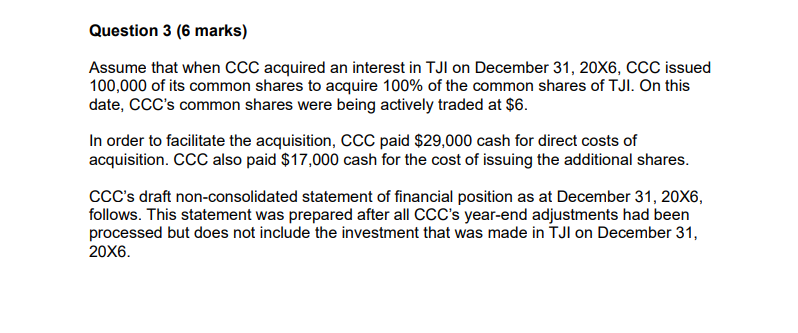

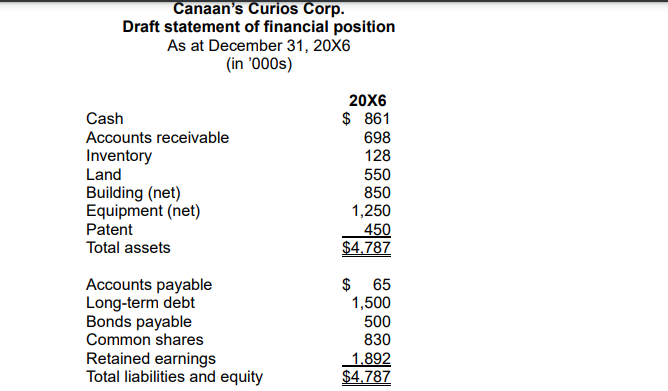

PROJECT 1 (42 MARKS) Advanced Financial Reporting has two projects. Project 1 is due at the end of Week 3 and covers material from Weeks 1 to 3. Project 2 is due at the end of Week 5 and focuses on material from Weeks 4 and 5. Before beginning work on the project, refer to the Project Formatting document for instructions on formatting and submitting the required work. Project 1 consists of four independent questions based on a common set of case facts. As this is a comprehensive case, it is recommended that you work on it as you read through the Student Notes and study materials for each week. Do not wait until the week in which this project is due to begin working on your submission. As you read through the Student Notes, make note of any relevant material that pertains to specific events or transactions in the case. Working through the project will assist you in preparing for the final exam. As a general rule, record the journal entries pertaining to the identified transactions in the same order as they arise in the supporting narrative. Support the journal entries with a brief explanation as to their nature. At the end of Week 3, you will be required to create and submit one Excel file for your answers to Questions 1 to 4. It should contain eight worksheets named as follows: 1. Q1(a) JEs and calcs 2. Q1(b) JEs and calcs 3. Q2 AD schedule 4. Q3 Consol. SFP 20X6 5 04 AD schedules 7. Q4 Consol. SCI & RE 8. Q4 Consol. SFP & NCI The Project Data file provided for you contains information that you may use to help you complete certain questions. You will be directed to this file as required in the questions below. Canaan's Curios Corp. Canaan's Curios Corp. (CCC) is a company located in Western Canada that reports its financial results in accordance with IFRS. On December 31, 20X6, CCC acquired common shares of Tymen Jungle Inc. (TJI). Four independent questions based on different quantities of shares acquired, but using the same financial results for TJI, are set out below. Tymen Jungle Inc. Statement of financial position As at December 31 (in '000s) Carrying value Fair value Remaining useful life/term to maturity 20X6 Cash Accounts receivable Inventory Land Building (net) Equipment (net) Patent Total assets 20x7 $ 68 75 74 325 285 232 30 $1,089 20X6 $ 35 48 62 175 300 400 30 $1,050 $ 68 164 345 380 142 N/A N/A 15 years 5 years 16 years Accounts payable $ 52 Notes payable 50 Long-term debt 300 Bonds payable 250 Common shares 180 Retained earnings 257 Total liabilities and equity $1,089 $ 37 0 400 250 180 183 $1.050 262 6 years Tymen Jungle Inc. Statement of comprehensive income For the year ended December 31, 20x7 (in '000s) Sales revenue Cost of goods sold Gross profit Sales, general, and administrative expenses Interest expense Depreciation and amortization expense $ 885 440 445 361 27 25 Other income Earnings before income tax expense Income tax expense Net income 32 135 167 33 $ 134 Intercompany transactions: CCC provided management services to TJI during the entire year. TJI paid $4,500 per month for this service. At December 31, 20X7, the amount owing for the services provided in December 20X7 remained unpaid. TJI rented a building to CCC for $7,000 per month. CCC rented the building for the entire year. At December 31, 20X7, CCC owed TJI $14,000 for November and December's rent. Land sale: On December 31, 20X7, CCC sold land to TJI for $150,000. CCC's net book value at time of sale was $100,000, which was the same as the estimated fair value at the acquisition date of the shares of TJI (December 31, 20X6). In consideration of the transfer, TJI paid $100,000 cash and signed a note payable to CCC for the $50,000 balance. The note is payable in full on December 31, 20X8. Interest at 5% per annum, which is the market rate of interest for an obligation of this nature, is first payable on December 31, 20X8. Inventory sales: During 20X7, CCC sold $125,000 of inventory to TJI. CCC's cost of the inventory was $95,000. 25% of these goods remained unsold by TJI as at December 31, 20X7. During 20X7, TJI sold goods that it had purchased for $150,000 to CCC for $210,000; 35% of these goods remained unsold by CCC as at December 31, 20x7. Equipment sale: On January 1, 20X7, TJI sold equipment to CCC for $70,000 cash. TJI's carrying value of the equipment, which had a remaining useful life of five years, was $44,000. Additional information: 1. Both companies pay income tax at a rate of 30%. 2. Both companies use the first in, first out (FIFO) cost-flow assumption to value their inventories. 3. Both companies depreciate their depreciable assets on a straight-line basis. 4. The fair value increment on the bonds is amortized using the straight-line method. 5. Both companies account for share-issuance costs using the retained earnings method.1 6. For impairment-testing purposes, CCC established that TJI is a cash-generating unit (CGU). 7. CCC and TJI only prepare accruals and other adjusting entries at year end. Question 3 (6 marks) Assume that when CCC acquired an interest in TJI on December 31, 20X6, CCC issued 100,000 of its common shares to acquire 100% of the common shares of TJI. On this date, CCC's common shares were being actively traded at $6. In order to facilitate the acquisition, CCC paid $29,000 cash for direct costs of acquisition. CCC also paid $17,000 cash for the cost of issuing the additional shares. CCC's draft non-consolidated statement of financial position as at December 31, 20X6, follows. This statement was prepared after all CCC's year-end adjustments had been processed but does not include the investment that was made in TJI on December 31, 20X6. Canaan's Curios Corp. Draft statement of financial position As at December 31, 20X6 (in '000s) Cash Accounts receivable Inventory Land Building (net) Equipment (net) Patent Total assets 20X6 $ 861 698 128 550 850 1,250 450 $4,787 Accounts payable Long-term debt Bonds payable Common shares Retained earnings Total liabilities and equity $ 65 1,500 500 830 1.892 $4,787 Required: In worksheet Q3 Consol. SFP 20X6 Prepare CCC's consolidated statement of financial position at the December 31, 20X6, acquisition date. (Refer back to the acquisition differential allocation schedule that you prepared in Question 2, but complete your work in Worksheet Q3.) Provide a brief explanation of all adjustments made to arrive at the consolidated SFP figures. For sake of clarity, these are the adjustments made while preparing the consolidated SFP, rather than adjusting journal entries. Note: From the Project Data file, copy and paste the template in the worksheet titled "Q3 Consolidated SFP 20X6" into your project submission file. Do not show your work in the Project Data file. PROJECT 1 (42 MARKS) Advanced Financial Reporting has two projects. Project 1 is due at the end of Week 3 and covers material from Weeks 1 to 3. Project 2 is due at the end of Week 5 and focuses on material from Weeks 4 and 5. Before beginning work on the project, refer to the Project Formatting document for instructions on formatting and submitting the required work. Project 1 consists of four independent questions based on a common set of case facts. As this is a comprehensive case, it is recommended that you work on it as you read through the Student Notes and study materials for each week. Do not wait until the week in which this project is due to begin working on your submission. As you read through the Student Notes, make note of any relevant material that pertains to specific events or transactions in the case. Working through the project will assist you in preparing for the final exam. As a general rule, record the journal entries pertaining to the identified transactions in the same order as they arise in the supporting narrative. Support the journal entries with a brief explanation as to their nature. At the end of Week 3, you will be required to create and submit one Excel file for your answers to Questions 1 to 4. It should contain eight worksheets named as follows: 1. Q1(a) JEs and calcs 2. Q1(b) JEs and calcs 3. Q2 AD schedule 4. Q3 Consol. SFP 20X6 5 04 AD schedules 7. Q4 Consol. SCI & RE 8. Q4 Consol. SFP & NCI The Project Data file provided for you contains information that you may use to help you complete certain questions. You will be directed to this file as required in the questions below. Canaan's Curios Corp. Canaan's Curios Corp. (CCC) is a company located in Western Canada that reports its financial results in accordance with IFRS. On December 31, 20X6, CCC acquired common shares of Tymen Jungle Inc. (TJI). Four independent questions based on different quantities of shares acquired, but using the same financial results for TJI, are set out below. Tymen Jungle Inc. Statement of financial position As at December 31 (in '000s) Carrying value Fair value Remaining useful life/term to maturity 20X6 Cash Accounts receivable Inventory Land Building (net) Equipment (net) Patent Total assets 20x7 $ 68 75 74 325 285 232 30 $1,089 20X6 $ 35 48 62 175 300 400 30 $1,050 $ 68 164 345 380 142 N/A N/A 15 years 5 years 16 years Accounts payable $ 52 Notes payable 50 Long-term debt 300 Bonds payable 250 Common shares 180 Retained earnings 257 Total liabilities and equity $1,089 $ 37 0 400 250 180 183 $1.050 262 6 years Tymen Jungle Inc. Statement of comprehensive income For the year ended December 31, 20x7 (in '000s) Sales revenue Cost of goods sold Gross profit Sales, general, and administrative expenses Interest expense Depreciation and amortization expense $ 885 440 445 361 27 25 Other income Earnings before income tax expense Income tax expense Net income 32 135 167 33 $ 134 Intercompany transactions: CCC provided management services to TJI during the entire year. TJI paid $4,500 per month for this service. At December 31, 20X7, the amount owing for the services provided in December 20X7 remained unpaid. TJI rented a building to CCC for $7,000 per month. CCC rented the building for the entire year. At December 31, 20X7, CCC owed TJI $14,000 for November and December's rent. Land sale: On December 31, 20X7, CCC sold land to TJI for $150,000. CCC's net book value at time of sale was $100,000, which was the same as the estimated fair value at the acquisition date of the shares of TJI (December 31, 20X6). In consideration of the transfer, TJI paid $100,000 cash and signed a note payable to CCC for the $50,000 balance. The note is payable in full on December 31, 20X8. Interest at 5% per annum, which is the market rate of interest for an obligation of this nature, is first payable on December 31, 20X8. Inventory sales: During 20X7, CCC sold $125,000 of inventory to TJI. CCC's cost of the inventory was $95,000. 25% of these goods remained unsold by TJI as at December 31, 20X7. During 20X7, TJI sold goods that it had purchased for $150,000 to CCC for $210,000; 35% of these goods remained unsold by CCC as at December 31, 20x7. Equipment sale: On January 1, 20X7, TJI sold equipment to CCC for $70,000 cash. TJI's carrying value of the equipment, which had a remaining useful life of five years, was $44,000. Additional information: 1. Both companies pay income tax at a rate of 30%. 2. Both companies use the first in, first out (FIFO) cost-flow assumption to value their inventories. 3. Both companies depreciate their depreciable assets on a straight-line basis. 4. The fair value increment on the bonds is amortized using the straight-line method. 5. Both companies account for share-issuance costs using the retained earnings method.1 6. For impairment-testing purposes, CCC established that TJI is a cash-generating unit (CGU). 7. CCC and TJI only prepare accruals and other adjusting entries at year end. Question 3 (6 marks) Assume that when CCC acquired an interest in TJI on December 31, 20X6, CCC issued 100,000 of its common shares to acquire 100% of the common shares of TJI. On this date, CCC's common shares were being actively traded at $6. In order to facilitate the acquisition, CCC paid $29,000 cash for direct costs of acquisition. CCC also paid $17,000 cash for the cost of issuing the additional shares. CCC's draft non-consolidated statement of financial position as at December 31, 20X6, follows. This statement was prepared after all CCC's year-end adjustments had been processed but does not include the investment that was made in TJI on December 31, 20X6. Canaan's Curios Corp. Draft statement of financial position As at December 31, 20X6 (in '000s) Cash Accounts receivable Inventory Land Building (net) Equipment (net) Patent Total assets 20X6 $ 861 698 128 550 850 1,250 450 $4,787 Accounts payable Long-term debt Bonds payable Common shares Retained earnings Total liabilities and equity $ 65 1,500 500 830 1.892 $4,787 Required: In worksheet Q3 Consol. SFP 20X6 Prepare CCC's consolidated statement of financial position at the December 31, 20X6, acquisition date. (Refer back to the acquisition differential allocation schedule that you prepared in Question 2, but complete your work in Worksheet Q3.) Provide a brief explanation of all adjustments made to arrive at the consolidated SFP figures. For sake of clarity, these are the adjustments made while preparing the consolidated SFP, rather than adjusting journal entries. Note: From the Project Data file, copy and paste the template in the worksheet titled "Q3 Consolidated SFP 20X6" into your project submission file. Do not show your work in the Project Data file