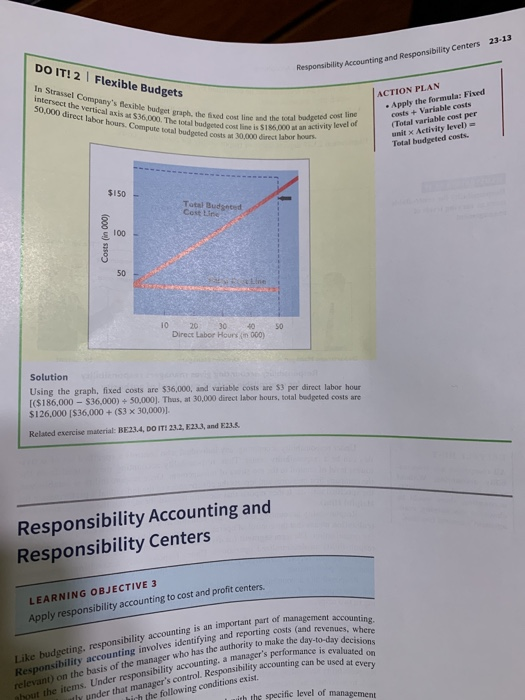

Project 2: Flexible Budget and Budget Report (10 points) Upload your file to Moodle by the deadline specified. Do NOT email your file! Halloween Supplies, Inc. estimates that 120,000 direct labor hours will be worked during 2019 in the Packaging Department. Based on this estimate, the following budget was developed for manufacturing overhead costs. Variable Overhead Costs Indirect labor $45,000 Indirect materials 28,500 Repairs 27,600 Utilities 17,400 Lubricants 6,600 $125,100 Fixed Overhead Costs Supervision $84,000 Depreciation 24,000 Insurance 15,000 Rent 10,800 Property taxes 7,200 $141,000 It is estimated that direct labor hours worked each month will range from 8,000 to 12,000 hours. During January, 10,000 direct labor hours were worked and the following overhead costs were incurred. Variable Overhead Costs Indirect labor $4,100 Indirect materials 2,300 Repairs 2,200 Utilities 1,500 Lubricants 600 $10,700 Fixed Overhead Costs Supervision $7,000 Depreciation 2,000 Insurance 1,250 Rent 900 Property taxes 600 $11,750 Instructions for Project 2: 1. Using Excel, prepare a monthly flexible manufacturing overhead budget for each increment of 1,000 direct labor hours over the relevant range for the year ending December 31, 2019. Refer to Illustration 23-13 in the chapter for an example. 2. Using Excel, prepare a manufacturing overhead budget report for January in good form. Refer to Illustration 23-16 in the chapter as a guide. 23-13 Responsibility Accounting and Responsibility Centers DO IT! 2 | Flexible Budgets In Strassel Company's flexible budget graph, intersect the vertical is $36,000. The total bod 50,000 direct direct labor hours. Computer et graph, the fixed cost line and the total budgeted cost line 000. The local bu s tan activity ACTION PLAN Apply the formula: Fixed costs + Variable costs (Total variable cost per unit x Activity level) Total budgeted costs. s 10.000 direct labe Total Budget Costa Costs (in 000) 10 20 30 50 Direct Labor Hours in 000) 50 Solution Using the graph, fixed costs are $36,000, and variable costs are $3 per direct labor hour ($186,000 - $36,000) + 50,000). Thus, at 30,000 direct labor hours, total budgeted costs are $126.000 [$36,000+ (53 x 30,000). Related exercise material: BE 234, DO IT! 23.2, E22.3, and E... Responsibility Accounting and Responsibility Centers LEARNING OBJECTIVE 3 Apply responsibility accounting to cost and profit centers, countin time is an important part of management acco Like budgeting, responsibility accounting is an important part of mana Responsibility accounting involves identifying and reporting costs relevant on the basis of the manager who has the authority to make the hout the items. Under responsibility accounting a manager's perform wly under that manager's control. Responsibility accounting canh hich the following conditions exist. ests and revenues, where make the day-to-day decisions s performance is evaluated on dibility assis of the mannlity accounting inting can be used at every Resport on the basiser responsibility control. Responsi h the specific level of management 25-16 CHAPTER 23 Budgetary Control and Responsibility Accounting wamen we have to love teily is only express y set the percentage di c e will investigate all Gences there wet budget warm investito de Materiality. Without quantitative guidelines. hudest difference regardless of the amount. Materi difference from budget. For example, management important items and 10% for other items. Managers under budset by the specified percentage. Costs mine why they were not controlled. Likewise, co mine whether costs critical to profitability are he costs are budgeted at $80,000 but only $40,000 is spene productive facilities may occur in the future. Alternatively might be under budget due to budgetary slack. Alternatively, a company may specify a single percentage items and supplement this guideline with a minimum dollari criteria may be stated at 5% of budget or more than $10,000 ise, costs under budget merivestigation are being curtailed. For example, mais is spent major unexpected breakdown natively, as discussed in Chapter 22.com tage difference from bolig dollar limit. For ample, the exception Controllability of the item. Exception guidelines are more restrictive items than for items the manager cannot control. In fact, there may be controllable items. For example, a large unfavorable difference between actual property tax expense may not be flagged for investigation because the only an unexpected increase in the tax rate or in the assessed value of the property into the difference would be useless: The manager cannot control either cause. ines are more restrictive for controllable ct, there may be no guidelines for me wable difference between actual and budgeted because the only possible cose he assessed value of the property. An investigation Behavioral Principles The human factor is critical in evaluating performance. Behavioral principles include the following 1. Managers of responsibility centers should have direct input into the process of establishing budget goals of their area of responsibility. Without such input, managers may view the goals as unrealistic or arbitrarily set by top management. Such views adversely affect the managers' motivation to meet the targeted objectives. 2. The evaluation of performance should be based entirely on matters that are controllable by the manager being evaluated. Criticism of a manager on matters outside his or her control reduces the effectiveness of the evaluation process. It can to negative reactions by a manager and to doubts about the fairness of the companys evaluation policies 3. Top management should support the evaluation process. As explained earlier, the tion process begins at the lowest level of responsibility and extends upward to the high level of management Managers quickly lose faith in the pagess when top mana ignores, overrules, or bypasses established procedures for evaluating a manager's park 4. The evaluation process must allow managers to respond to their Evaluation is not a one-way street. Managers should have the opportunity to performance. Evaluation without feedback is both impersonal and ineffective 5. The evaluation should identify both good and poor performance. Praise to performance is a powerful motivating factor for a manger. This is especially manager's compensation includes rewards for meeting budget goals Reporting Principles Performance evaluation under responsibility assuntine should be based on certa principles. These principles pertain primarily to the internal reports that provo evaluating performance. Performance reports should: 1. Contain only data that are controllable by the manager of the responsibility con 2. Provide accurate and reliable budget data to measure performance 3. Highlight significant differences between actual results and budget goals. 4. Be tailor-made for the intended evaluation by ensuring only controllable costs are in 5. Be preparat r ah have the opportunity to defend their er. This is especially true when a uld be based on certain reporting internal reports that provide the basis for g only controllable costs are included Project 2: Flexible Budget and Budget Report (10 points) Upload your file to Moodle by the deadline specified. Do NOT email your file! Halloween Supplies, Inc. estimates that 120,000 direct labor hours will be worked during 2019 in the Packaging Department. Based on this estimate, the following budget was developed for manufacturing overhead costs. Variable Overhead Costs Indirect labor $45,000 Indirect materials 28,500 Repairs 27,600 Utilities 17,400 Lubricants 6,600 $125,100 Fixed Overhead Costs Supervision $84,000 Depreciation 24,000 Insurance 15,000 Rent 10,800 Property taxes 7,200 $141,000 It is estimated that direct labor hours worked each month will range from 8,000 to 12,000 hours. During January, 10,000 direct labor hours were worked and the following overhead costs were incurred. Variable Overhead Costs Indirect labor $4,100 Indirect materials 2,300 Repairs 2,200 Utilities 1,500 Lubricants 600 $10,700 Fixed Overhead Costs Supervision $7,000 Depreciation 2,000 Insurance 1,250 Rent 900 Property taxes 600 $11,750 Instructions for Project 2: 1. Using Excel, prepare a monthly flexible manufacturing overhead budget for each increment of 1,000 direct labor hours over the relevant range for the year ending December 31, 2019. Refer to Illustration 23-13 in the chapter for an example. 2. Using Excel, prepare a manufacturing overhead budget report for January in good form. Refer to Illustration 23-16 in the chapter as a guide. 23-13 Responsibility Accounting and Responsibility Centers DO IT! 2 | Flexible Budgets In Strassel Company's flexible budget graph, intersect the vertical is $36,000. The total bod 50,000 direct direct labor hours. Computer et graph, the fixed cost line and the total budgeted cost line 000. The local bu s tan activity ACTION PLAN Apply the formula: Fixed costs + Variable costs (Total variable cost per unit x Activity level) Total budgeted costs. s 10.000 direct labe Total Budget Costa Costs (in 000) 10 20 30 50 Direct Labor Hours in 000) 50 Solution Using the graph, fixed costs are $36,000, and variable costs are $3 per direct labor hour ($186,000 - $36,000) + 50,000). Thus, at 30,000 direct labor hours, total budgeted costs are $126.000 [$36,000+ (53 x 30,000). Related exercise material: BE 234, DO IT! 23.2, E22.3, and E... Responsibility Accounting and Responsibility Centers LEARNING OBJECTIVE 3 Apply responsibility accounting to cost and profit centers, countin time is an important part of management acco Like budgeting, responsibility accounting is an important part of mana Responsibility accounting involves identifying and reporting costs relevant on the basis of the manager who has the authority to make the hout the items. Under responsibility accounting a manager's perform wly under that manager's control. Responsibility accounting canh hich the following conditions exist. ests and revenues, where make the day-to-day decisions s performance is evaluated on dibility assis of the mannlity accounting inting can be used at every Resport on the basiser responsibility control. Responsi h the specific level of management 25-16 CHAPTER 23 Budgetary Control and Responsibility Accounting wamen we have to love teily is only express y set the percentage di c e will investigate all Gences there wet budget warm investito de Materiality. Without quantitative guidelines. hudest difference regardless of the amount. Materi difference from budget. For example, management important items and 10% for other items. Managers under budset by the specified percentage. Costs mine why they were not controlled. Likewise, co mine whether costs critical to profitability are he costs are budgeted at $80,000 but only $40,000 is spene productive facilities may occur in the future. Alternatively might be under budget due to budgetary slack. Alternatively, a company may specify a single percentage items and supplement this guideline with a minimum dollari criteria may be stated at 5% of budget or more than $10,000 ise, costs under budget merivestigation are being curtailed. For example, mais is spent major unexpected breakdown natively, as discussed in Chapter 22.com tage difference from bolig dollar limit. For ample, the exception Controllability of the item. Exception guidelines are more restrictive items than for items the manager cannot control. In fact, there may be controllable items. For example, a large unfavorable difference between actual property tax expense may not be flagged for investigation because the only an unexpected increase in the tax rate or in the assessed value of the property into the difference would be useless: The manager cannot control either cause. ines are more restrictive for controllable ct, there may be no guidelines for me wable difference between actual and budgeted because the only possible cose he assessed value of the property. An investigation Behavioral Principles The human factor is critical in evaluating performance. Behavioral principles include the following 1. Managers of responsibility centers should have direct input into the process of establishing budget goals of their area of responsibility. Without such input, managers may view the goals as unrealistic or arbitrarily set by top management. Such views adversely affect the managers' motivation to meet the targeted objectives. 2. The evaluation of performance should be based entirely on matters that are controllable by the manager being evaluated. Criticism of a manager on matters outside his or her control reduces the effectiveness of the evaluation process. It can to negative reactions by a manager and to doubts about the fairness of the companys evaluation policies 3. Top management should support the evaluation process. As explained earlier, the tion process begins at the lowest level of responsibility and extends upward to the high level of management Managers quickly lose faith in the pagess when top mana ignores, overrules, or bypasses established procedures for evaluating a manager's park 4. The evaluation process must allow managers to respond to their Evaluation is not a one-way street. Managers should have the opportunity to performance. Evaluation without feedback is both impersonal and ineffective 5. The evaluation should identify both good and poor performance. Praise to performance is a powerful motivating factor for a manger. This is especially manager's compensation includes rewards for meeting budget goals Reporting Principles Performance evaluation under responsibility assuntine should be based on certa principles. These principles pertain primarily to the internal reports that provo evaluating performance. Performance reports should: 1. Contain only data that are controllable by the manager of the responsibility con 2. Provide accurate and reliable budget data to measure performance 3. Highlight significant differences between actual results and budget goals. 4. Be tailor-made for the intended evaluation by ensuring only controllable costs are in 5. Be preparat r ah have the opportunity to defend their er. This is especially true when a uld be based on certain reporting internal reports that provide the basis for g only controllable costs are included