Answered step by step

Verified Expert Solution

Question

1 Approved Answer

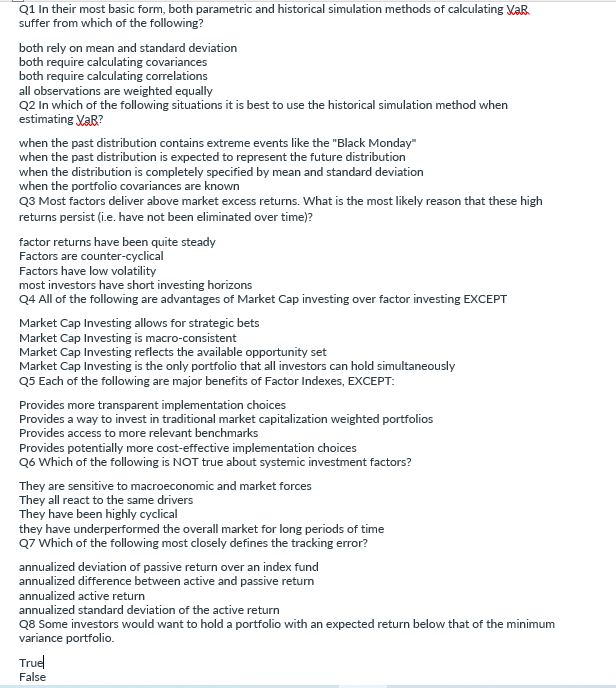

Q 1 In their most basic form, both parametric and historical simulation methods of calculating XaR. suffer from which of the following? both rely on

Q In their most basic form, both parametric and historical simulation methods of calculating XaR.

suffer from which of the following?

both rely on mean and standard deviation

both require calculating covariances

both require calculating correlations

all observations are weighted equally

Q In which of the following situations it is best to use the historical simulation method when

estimating XaR?

when the past distribution contains extreme events like the "Black Monday"

when the past distribution is expected to represent the future distribution

when the distribution is completely specified by mean and standard deviation

when the portfolio covariances are known

Q Most factors deliver above market excess returns. What is the most likely reason that these high

returns persist ie have not been eliminated over time

factor returns have been quite steady

Factors are countercyclical

Factors have low volatility

most investors have short investing horizons

Q All of the following are advantages of Market Cap investing over factor investing EXCEPT

Market Cap Investing allows for strategic bets

Market Cap Investing is macroconsistent

Market Cap Investing reflects the available opportunity set

Market Cap Investing is the only portfolio that all investors can hold simultaneously

Q Each of the following are major benefits of Factor Indexes, EXCEPT:

Provides more transparent implementation choices

Provides a way to invest in traditional market capitalization weighted portfolios

Provides access to more relevant benchmarks

Provides potentially more costeffective implementation choices

Q Which of the following is NOT true about systemic investment factors?

They are sensitive to macroeconomic and market forces

They all react to the same drivers

They have been highly cyclical

they have underperformed the overall market for long periods of time

Q Which of the following most closely defines the tracking error?

annualized deviation of passive return over an index fund

annualized difference between active and passive return

annualized active return

annualized standard deviation of the active return

Q Some investors would want to hold a portfolio with an expected return below that of the minimum

variance portfolio.

True

False

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol Eun, Bruce Resnick

7th Edition

0077861604, 9780077861605