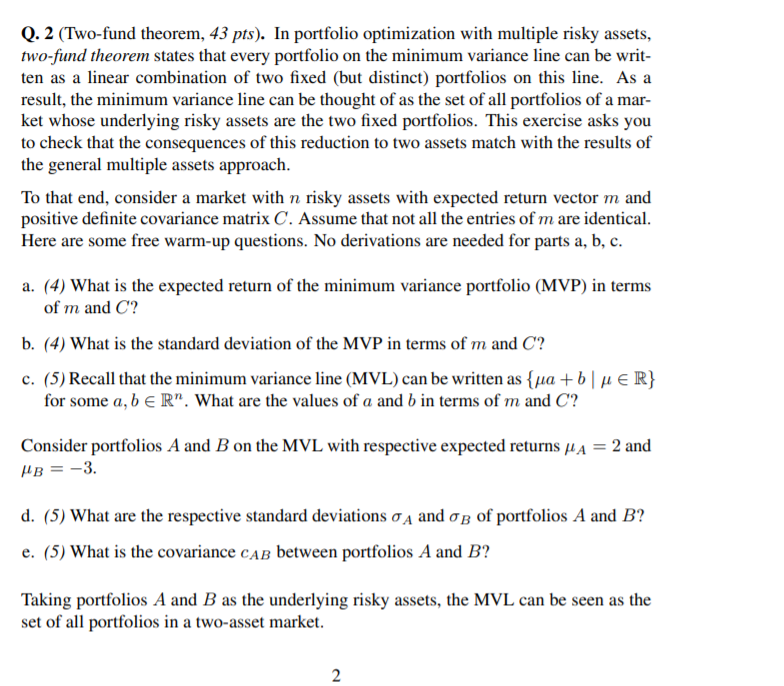

Q. 2 (Two-fund theorem, 43 pts). In portfolio optimization with multiple risky assets, two-fund theorem states that every portfolio on the minimum variance line can be writ- ten as a linear combination of two fixed (but distinct) portfolios on this line. As a result, the minimum variance line can be thought of as the set of all portfolios of a mar- ket whose underlying risky assets are the two fixed portfolios. This exercise asks you to check that the consequences of this reduction to two assets match with the results of the general multiple assets approach. To that end, consider a market with n risky assets with expected return vector m and positive definite covariance matrix C. Assume that not all the entries of m are identical. Here are some free warm-up questions. No derivations are needed for parts a, b, c. a. (4) What is the expected return of the minimum variance portfolio (MVP) in terms of m and C? b. (4) What is the standard deviation of the MVP in terms of m and C? c. (5) Recall that the minimum variance line (MVL) can be written as {ya + b HER} for some a, b e R". What are the values of a and b in terms of m and C? Consider portfolios A and B on the MVL with respective expected returns u A = 2 and HB = -3. d. (5) What are the respective standard deviations o A and o B of portfolios A and B? e. (5) What is the covariance CAB between portfolios A and B? Taking portfolios A and B as the underlying risky assets, the MVL can be seen as the set of all portfolios in a two-asset market. 2 Q. 2 (Two-fund theorem, 43 pts). In portfolio optimization with multiple risky assets, two-fund theorem states that every portfolio on the minimum variance line can be writ- ten as a linear combination of two fixed (but distinct) portfolios on this line. As a result, the minimum variance line can be thought of as the set of all portfolios of a mar- ket whose underlying risky assets are the two fixed portfolios. This exercise asks you to check that the consequences of this reduction to two assets match with the results of the general multiple assets approach. To that end, consider a market with n risky assets with expected return vector m and positive definite covariance matrix C. Assume that not all the entries of m are identical. Here are some free warm-up questions. No derivations are needed for parts a, b, c. a. (4) What is the expected return of the minimum variance portfolio (MVP) in terms of m and C? b. (4) What is the standard deviation of the MVP in terms of m and C? c. (5) Recall that the minimum variance line (MVL) can be written as {ya + b HER} for some a, b e R". What are the values of a and b in terms of m and C? Consider portfolios A and B on the MVL with respective expected returns u A = 2 and HB = -3. d. (5) What are the respective standard deviations o A and o B of portfolios A and B? e. (5) What is the covariance CAB between portfolios A and B? Taking portfolios A and B as the underlying risky assets, the MVL can be seen as the set of all portfolios in a two-asset market. 2