Question

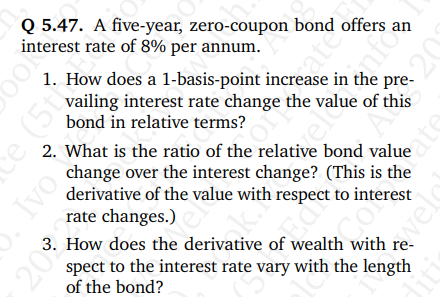

Q 5.47 A five-year, zero-coupon bond offers an interest rate of 8% per annum. 1. How does a 1 basis point increase in the prevailing

Q 5.47 A five-year, zero-coupon bond offers an interest rate of 8% per annum. 1. How does a 1 basis point increase in the prevailing interest rate change the value of this bond in relative terms? 2. what is the ratio of the relative bond value change over the interest change? (this is the derivative of the value with respect to interest rate changes) 3. How does the derivative of wealth with respect to the interest rate vary with the length of the bond?

Q 5.47. A five-year, zero-coupon bond offers an interest rate of 8% per annum. 1. How does a 1-basis-point increase in the prevailing interest rate change the value of this bond in relative terms? 2. What is the ratio of the relative bond value change over the interest change? (This is the derivative of the value with respect to interest rate changes.) 3 . How does the derivative of wealth with respect to the interest rate vary with the length of the bond

Q 5.47. A five-year, zero-coupon bond offers an interest rate of 8% per annum. 1. How does a 1-basis-point increase in the prevailing interest rate change the value of this bond in relative terms? 2. What is the ratio of the relative bond value change over the interest change? (This is the derivative of the value with respect to interest rate changes.) 3 . How does the derivative of wealth with respect to the interest rate vary with the length of the bond Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Smart Supply Chain Finance

Authors: Hua Song

1st Edition

9811659966, 978-9811659966