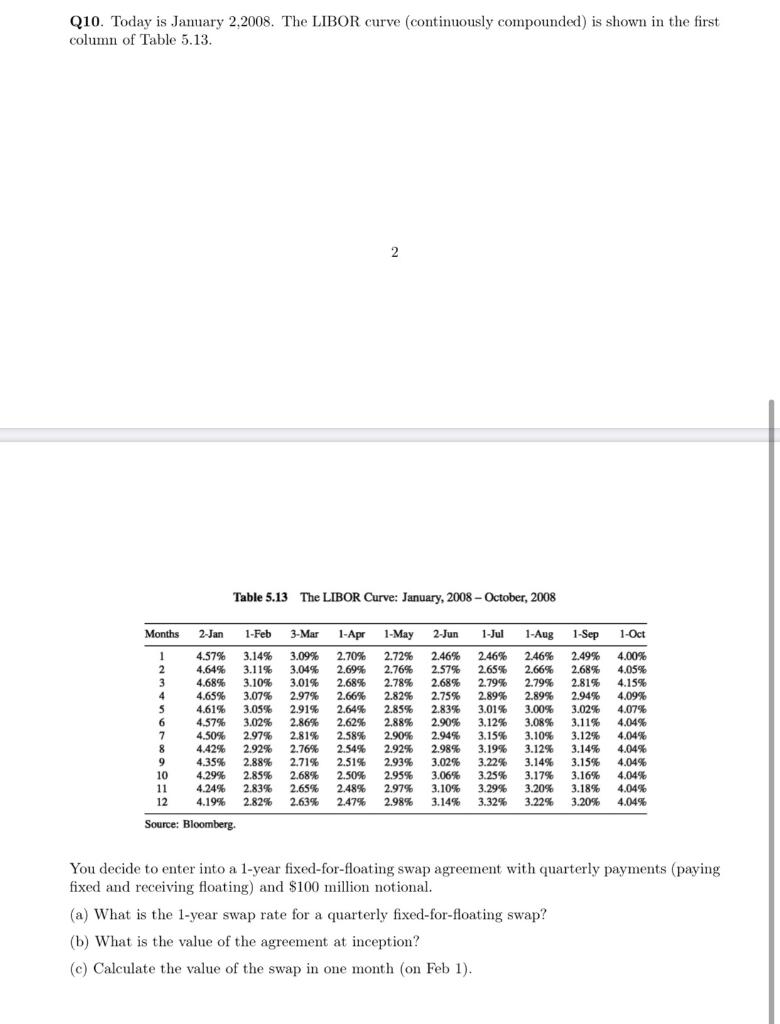

Question: Q10. Today is January 2,2008. The LIBOR curve (continuously compounded) is shown in the first column of Table 5.13. 2 Table 5.13 The LIBOR

Q10. Today is January 2,2008. The LIBOR curve (continuously compounded) is shown in the first column of Table 5.13. 2 Table 5.13 The LIBOR Curve: January, 2008-October, 2008 Months 1 2 3 4 5 2-Jan 1-Feb 3-Mar 1-Apr 1-May 2-Jun 1-Jul 1-Aug 1-Sep 1-Oct 4.57% 3.14% 3.09% 2.70% 2.72% 2.46% 2.46% 2.46% 2.49% 4.00% 4.64% 3.11% 3.04% 2.69% 2.76% 2.57% 2.65% 2.66% 2.68% 4.05% 4.68% 3.10% 3.01% 2.68% 2.78% 2.68% 2.79% 2,79% 2.81% 4.15% 4.65% 3.07% 2.97% 2.66% 2.82% 2.75% 2.89% 2.89% 2.94% 4.09% 4.61% 3.05% 2.91% 2.64% 2.85% 2.83% 3.01% 3.00% 3.02% 4.07% 4.57% 3.02% 2.86% 2.62% 2.88% 2.90% 3.12% 3.08% 3.11% 4.04% 4.50% 2.97% 2.81% 2.58% 2.90% 2.94% 3.15% 3.10% 3.12% 4.04% 4.42% 2.92% 2.76% 2.54% 2.92% 2.98% 3.19% 3.12% 3.14% 4.04% 4.35% 2.88% 2,71% 2.51% 2.93% 3.02% 3.22% 3.14% 3.15% 4.04% 4.29% 2.85% 2.68% 2.50% 2.95% 3.06% 3.25% 3.17 % 3.16% 4.04% 4.24% 2.83% 2.65% 2.48% 2.97% 3.10% 3.29% 3.20% 3.18% 6 7 8 9 10 11 4.04% 12 4.19% 2.82% 2.63% 2.47% 2.98% 3.14% 3.32% 3.22% 3.20% 4.04% Source: Bloomberg. You decide to enter into a 1-year fixed-for-floating swap agreement with quarterly payments (paying fixed and receiving floating) and $100 million notional. (a) What is the 1-year swap rate for a quarterly fixed-for-floating swap? (b) What is the value of the agreement at inception? (c) Calculate the value of the swap in one month (on Feb 1).

Step by Step Solution

3.45 Rating (168 Votes )

There are 3 Steps involved in it

Part a time in months Quarter Spot rate ZCB Discount Factor Read from LIBOR Curve under 2Jan date r ... View full answer

Get step-by-step solutions from verified subject matter experts