Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q1.Explain each of the following concepts as they relate to call options. a. Rho ( 1 Mark) b. Theta ( 1 Mark) c. Vega (1

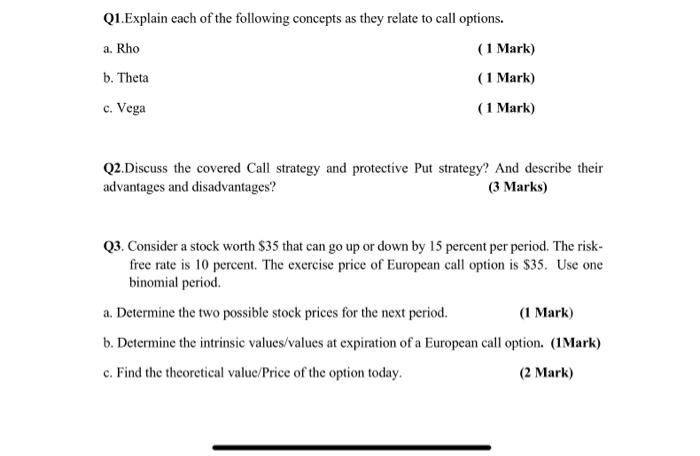

Q1.Explain each of the following concepts as they relate to call options. a. Rho ( 1 Mark) b. Theta ( 1 Mark) c. Vega (1 Mark) Q2.Discuss the covered Call strategy and protective Put strategy? And describe their advantages and disadvantages? (3 Marks) Q3. Consider a stock worth $35 that can go up or down by 15 percent per period. The riskfree rate is 10 percent. The exercise price of European call option is $35. Use one binomial period. a. Determine the two possible stock prices for the next period. (1 Mark) b. Determine the intrinsic values/values at expiration of a European call option. (1Mark) c. Find the theoretical value/Price of the option today. (2 Mark) Q1.Explain each of the following concepts as they relate to call options. a. Rho ( 1 Mark) b. Theta ( 1 Mark) c. Vega (1 Mark) Q2.Discuss the covered Call strategy and protective Put strategy? And describe their advantages and disadvantages? (3 Marks) Q3. Consider a stock worth $35 that can go up or down by 15 percent per period. The riskfree rate is 10 percent. The exercise price of European call option is $35. Use one binomial period. a. Determine the two possible stock prices for the next period. (1 Mark) b. Determine the intrinsic values/values at expiration of a European call option. (1Mark) c. Find the theoretical value/Price of the option today. (2 Mark)

Q1.Explain each of the following concepts as they relate to call options. a. Rho ( 1 Mark) b. Theta ( 1 Mark) c. Vega (1 Mark) Q2.Discuss the covered Call strategy and protective Put strategy? And describe their advantages and disadvantages? (3 Marks) Q3. Consider a stock worth $35 that can go up or down by 15 percent per period. The riskfree rate is 10 percent. The exercise price of European call option is $35. Use one binomial period. a. Determine the two possible stock prices for the next period. (1 Mark) b. Determine the intrinsic values/values at expiration of a European call option. (1Mark) c. Find the theoretical value/Price of the option today. (2 Mark) Q1.Explain each of the following concepts as they relate to call options. a. Rho ( 1 Mark) b. Theta ( 1 Mark) c. Vega (1 Mark) Q2.Discuss the covered Call strategy and protective Put strategy? And describe their advantages and disadvantages? (3 Marks) Q3. Consider a stock worth $35 that can go up or down by 15 percent per period. The riskfree rate is 10 percent. The exercise price of European call option is $35. Use one binomial period. a. Determine the two possible stock prices for the next period. (1 Mark) b. Determine the intrinsic values/values at expiration of a European call option. (1Mark) c. Find the theoretical value/Price of the option today. (2 Mark)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Palgrave International Handbook Of Basic Income

Authors: Malcolm Torry

1st Edition

3030236137, 978-3030236137