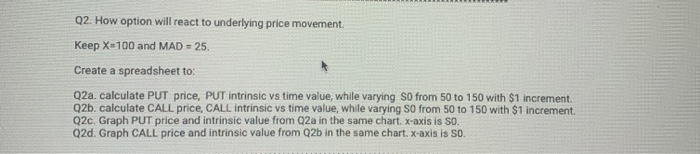

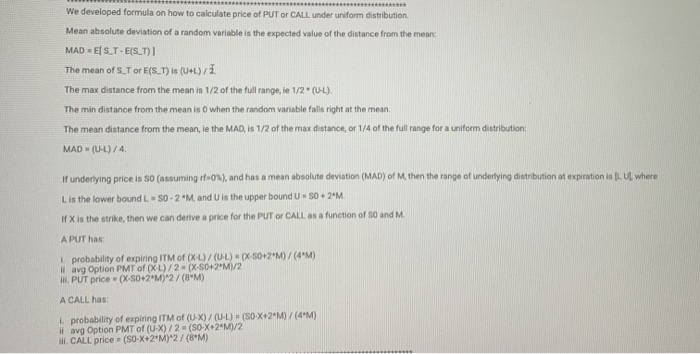

Q2. How option will react to underlying price movement. Keep X=100 and MAD = 25. Create a spreadsheet to: Q2a. calculate PUT price, PUT intrinsic vs time value, while varying so from 50 to 150 with $1 increment Q2b. calculate CALL price, CALL intrinsic vs time value, while varying so from 50 to 150 with $1 increment. Q2c. Graph PUT price and intrinsic value from 02a in the same chart. x-axis is so. Q2d. Graph CALL price and intrinsic value from Q2b in the same chart. x-axis is SO. We developed formula on how to calculate price of PUT or CALL under uniform distribution Mean absolute deviation of a random variable is the expected value of the distance from the mean: MAD = EST. E(S_T) The mean of S. Tor E(S. 1) 18 (U+L)/ The max distance from the mean is 1/2 of the full range, ie 1/2" (U-L). The min distance from the mean is o when the random variable falls right at the mean The mean distance from the mean, le the MAD, is 1/2 of the max distance, or 1/4 of the full range for a uniform distribution: MAD - (UL)/4 If underlying price is so (assuming r=0x), and has a mean absolute deviation (MAD) of M, then the range of underlying distribution at expiration is (LU) where L is the lower bound L-SO-2 *M, and is the upper bound U-S0 + 2M if X is the strike, then we can derive a price for the PUT O CALL as a function of 50 and M A PUT has probability of expiring ITM of (x-1)/(UL)(X-50+2*M)/(4"M) avg Option PMT of (XL)/2 = (X-50*2*M)/2 I. PUT price - (X-S0+2M) 2/(M) A CALL has probability of expiring ITM of (U-X)/(U-L) + (SOX+2*M)/(4M) il avg Option PMT of (U-X)/2 = (SO-X+2*M)/2 I. CALL price. (S0-X+2M)*2 / (BM) Q2. How option will react to underlying price movement. Keep X=100 and MAD = 25. Create a spreadsheet to: Q2a. calculate PUT price, PUT intrinsic vs time value, while varying so from 50 to 150 with $1 increment Q2b. calculate CALL price, CALL intrinsic vs time value, while varying so from 50 to 150 with $1 increment. Q2c. Graph PUT price and intrinsic value from 02a in the same chart. x-axis is so. Q2d. Graph CALL price and intrinsic value from Q2b in the same chart. x-axis is SO. We developed formula on how to calculate price of PUT or CALL under uniform distribution Mean absolute deviation of a random variable is the expected value of the distance from the mean: MAD = EST. E(S_T) The mean of S. Tor E(S. 1) 18 (U+L)/ The max distance from the mean is 1/2 of the full range, ie 1/2" (U-L). The min distance from the mean is o when the random variable falls right at the mean The mean distance from the mean, le the MAD, is 1/2 of the max distance, or 1/4 of the full range for a uniform distribution: MAD - (UL)/4 If underlying price is so (assuming r=0x), and has a mean absolute deviation (MAD) of M, then the range of underlying distribution at expiration is (LU) where L is the lower bound L-SO-2 *M, and is the upper bound U-S0 + 2M if X is the strike, then we can derive a price for the PUT O CALL as a function of 50 and M A PUT has probability of expiring ITM of (x-1)/(UL)(X-50+2*M)/(4"M) avg Option PMT of (XL)/2 = (X-50*2*M)/2 I. PUT price - (X-S0+2M) 2/(M) A CALL has probability of expiring ITM of (U-X)/(U-L) + (SOX+2*M)/(4M) il avg Option PMT of (U-X)/2 = (SO-X+2*M)/2 I. CALL price. (S0-X+2M)*2 / (BM)