Answered step by step

Verified Expert Solution

Question

1 Approved Answer

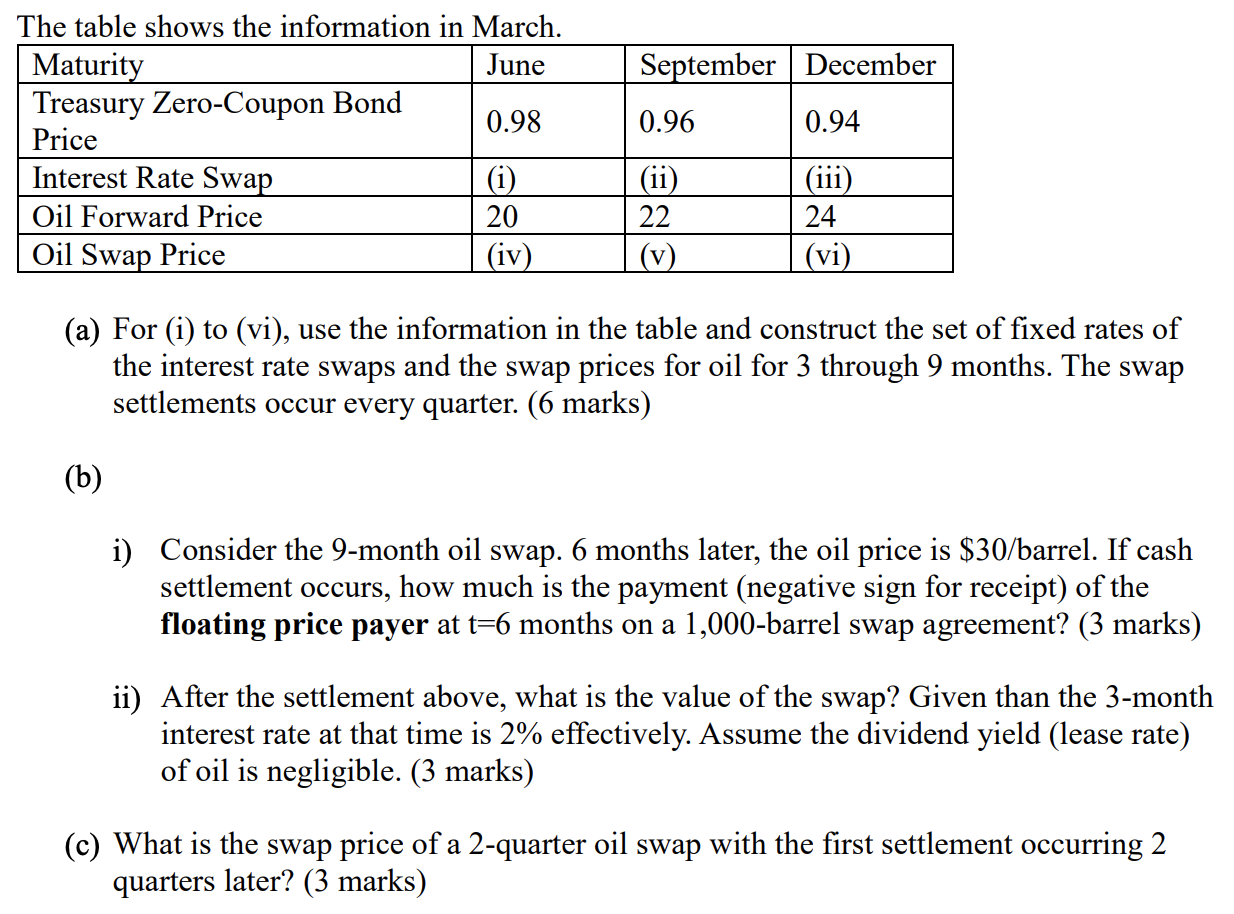

Q5 September December 0.96 0.94 The table shows the information in March. Maturity June Treasury Zero-Coupon Bond 0.98 Price Interest Rate Swap (i) Oil Forward

Q5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Computer Accounting With QuickBooks Pro 2010

Authors: Donna UlmerDonna Kay

12th Edition

0077408756, 9780077408756