Answered step by step

Verified Expert Solution

Question

1 Approved Answer

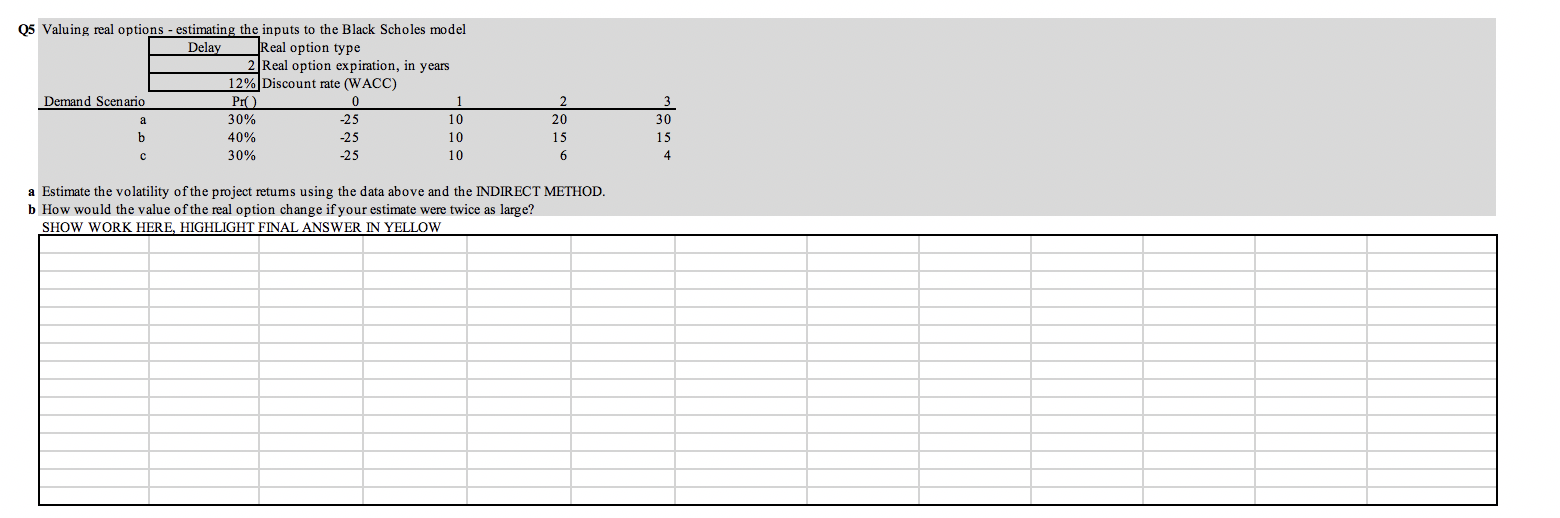

Q5 Valuing real options - estimating the inputs to the Black Scholes model Delay Real option type Real option expiration, in years 12% Discount rate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

U.S. Mergers And Acquisitions Legal And Financial Aspects

Authors: Felix Lessambo

1st Edition

3030857344,3030857352