Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q7 A/B 7. A) How does an increase in diversification of assets modify the riskiness of a portfolio? B) Using the diagram below, with a

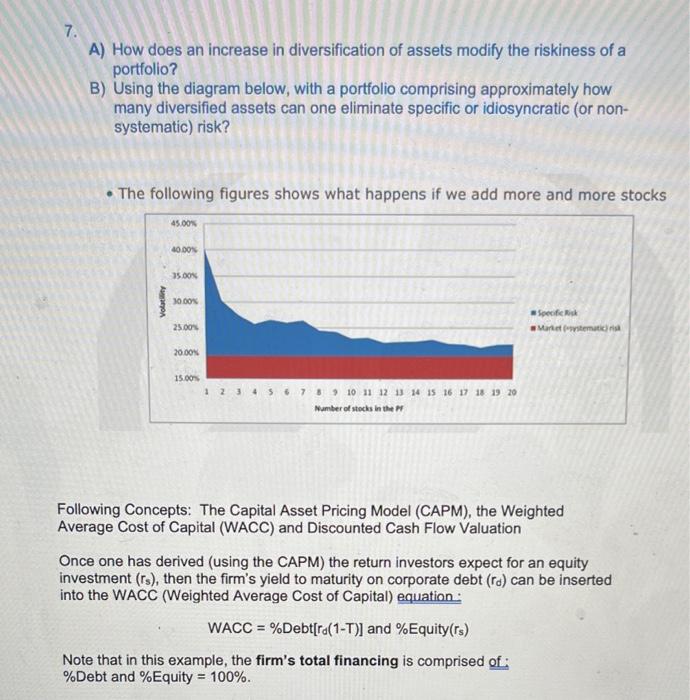

Q7 A/B  7. A) How does an increase in diversification of assets modify the riskiness of a portfolio? B) Using the diagram below, with a portfolio comprising approximately how many diversified assets can one eliminate specific or idiosyncratic (or nonsystematic) risk? - The following figures shows what happens if we add more and more stocks Following Concepts: The Capital Asset Pricing Model (CAPM), the Weighted Average Cost of Capital (WACC) and Discounted Cash Flow Valuation Once one has derived (using the CAPM) the return investors expect for an equity investment (rs), then the firm's yield to maturity on corporate debt (rd) can be inserted into the WACC (Weighted Average Cost of Capital) equation: WACC=%Debt[rad(1T)]and%Equity(rs) Note that in this example, the firm's total financing is comprised of: % Debt and % Equity =100%

7. A) How does an increase in diversification of assets modify the riskiness of a portfolio? B) Using the diagram below, with a portfolio comprising approximately how many diversified assets can one eliminate specific or idiosyncratic (or nonsystematic) risk? - The following figures shows what happens if we add more and more stocks Following Concepts: The Capital Asset Pricing Model (CAPM), the Weighted Average Cost of Capital (WACC) and Discounted Cash Flow Valuation Once one has derived (using the CAPM) the return investors expect for an equity investment (rs), then the firm's yield to maturity on corporate debt (rd) can be inserted into the WACC (Weighted Average Cost of Capital) equation: WACC=%Debt[rad(1T)]and%Equity(rs) Note that in this example, the firm's total financing is comprised of: % Debt and % Equity =100%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Managerial Finance

Authors: Lawrence J. Gitman, Chad J. Zutter

13th Edition

9780132738729, 136119468, 132738724, 978-0136119463