Answered step by step

Verified Expert Solution

Question

1 Approved Answer

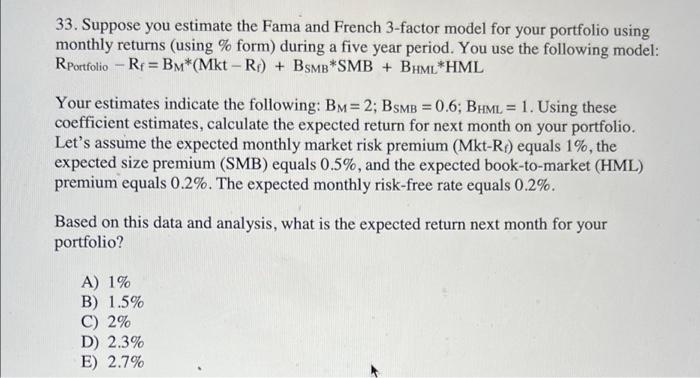

QA 33. Suppose you estimate the Fama and French 3-factor model for your portfolio using monthly returns (using % form) during a five year period.

QA

33. Suppose you estimate the Fama and French 3-factor model for your portfolio using monthly returns (using % form) during a five year period. You use the following model: RPortfolio - R = Bm*(Mkt - Ri) + BsMB*SMB + BHML*HML - Your estimates indicate the following: Bm=2; BsMB = 0.6; BHML = 1. Using these coefficient estimates, calculate the expected return for next month on your portfolio. Let's assume the expected monthly market risk premium (Mkt-Ri) equals 1%, the expected size premium (SMB) equals 0.5%, and the expected book-to-market (HML) premium equals 0.2%. The expected monthly risk-free rate equals 0.2%. Based on this data and analysis, what is the expected return next month for your portfolio? A) 1% B) 1.5% C) 2% D) 2.3% E) 2.7% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Instability Toolkit For Interpreting Boom And Bust Cycles

Authors: V. D'Apice, G. Ferri

1st Edition

023024811X, 9780230248113