Answered step by step

Verified Expert Solution

Question

1 Approved Answer

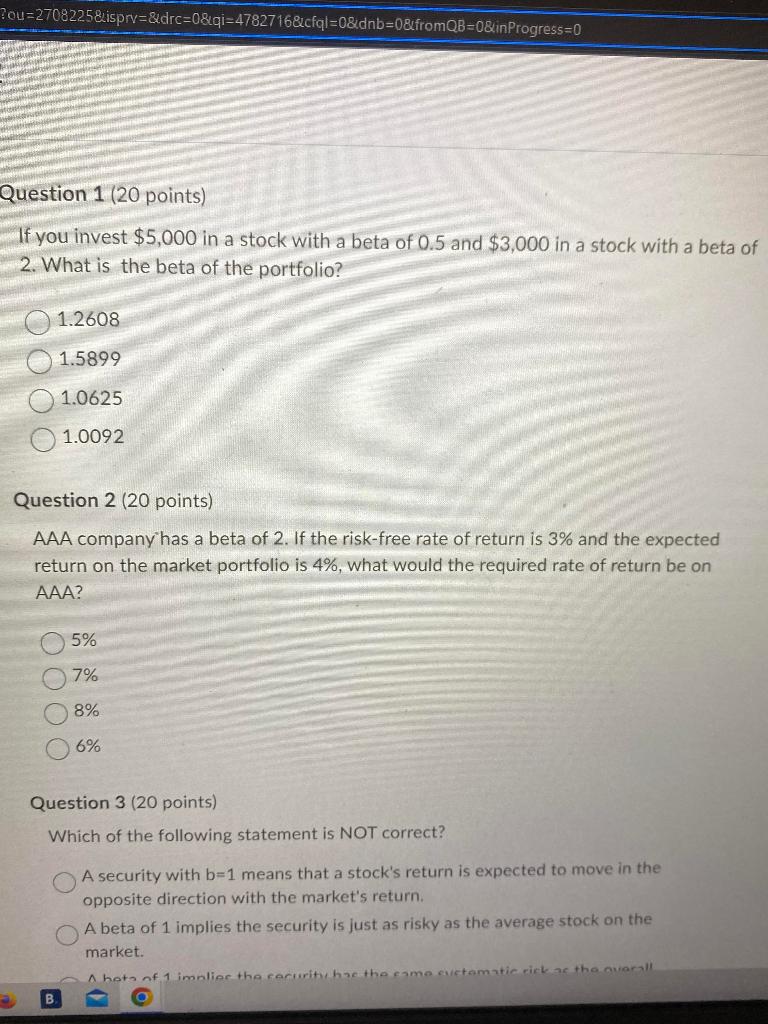

Qestions 1-2. Thanks! If you invest $5,000 in a stock with a beta of 0.5 and $3,000 in a stock with a beta of 2.

Qestions 1-2. Thanks!

If you invest $5,000 in a stock with a beta of 0.5 and $3,000 in a stock with a beta of 2. What is the beta of the portfolio? 1.2608 1.5899 1.0625 1.0092 Question 2 ( 20 points) AAA company has a beta of 2 . If the risk-free rate of return is 3% and the expected return on the market portfolio is 4%, what would the required rate of return be on AAA ? 5% 7% 8% 6% Question 3 (20 points) Which of the following statement is NOT correct? A security with b=1 means that a stock's return is expected to move in the opposite direction with the market's return. A beta of 1 implies the security is just as risky as the average stock on the market

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Deflation Current And Historical Perspectives

Authors: Richard C. K. Burdekin, Pierre L. Siklos

1st Edition

0521837995,0511227671