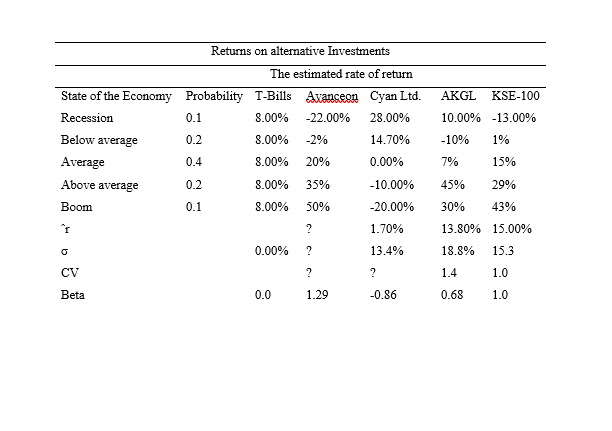

Ql. Assume that you recently graduated with a major in finance, and you just landed a job as a financial planner with Aurigin Inc., a large financial services corporation. Your first assignment is to invest PKR 100,000 for a client. Because the funds are to be invested in a business at the end of 1 year, you have been instructed to plan for a 1-year holding period. Further, your boss has restricted you to the following investment alternatives, shown with their probabilities and associated outcomes. Aurigin's economic forecasting staff has developed probability estimates for the state of the economy, and its security analysts have developed a sophisticated computer program that was used to estimate the rate of return on each alternative under each state of the economy. Avanceon Limited is a technology and communications firm: Cyan Ltd is an investment company and AKGL Co. manufactures foam and allied products. Aurigin also maintains an "index fund which owns a Market weighted fraction of all publicly traded stocks; you can invest in that fund, and thus obtain average stock market results. Given the situation as described, answer the following questions. C) Suppose you suddenly remembered that the coefficient of variation (CV) is generally regarded as being a better measure of stand-alone risk than the standard deviation when the alternatives being considered to have widely differing expected returns. Calculate the missing CVs, and fill in the blanks in the row for CV in the table below. Does the CV produce the same risk rankings as the standard deviation? [Marks 02] D) Assume that the correlation between the Avanceen and Cyan Ltd is perfectly negative. what will be the standard deviation of the portfolio if all the money is invested in only these two shares in an equal proportion. E) Suppose you create a portfolio of T-Bills, Avansegn, Cyan Ltd, and AKGL by investing the funds in equal proportion. Calculate the beta of the portfolio you constructed. [Marks 01| Returns on alternative Investments The estimated rate of return Probability T-Bills Avanceon Cyan Ltd. AKGL State of the Economy Recession KSE-100 0.1 8.00% -22.00% 28.00% 10.00% -13.00% Below average 0.2 8.00% -2% 14.70% -10% 1% Average 0.4 8.00% 20% 0.00% 7% 15% Above average 0.2 8.00% 35% -10.00% 45% 29% Boom 0.1 8.00% 50% -20.00% 30% 43% 1 ? 1.70% 13.80% 15.00% 0 0.00% ? 13.4% 18.8% 15.3 CV ? ? 1.4 1.0 Beta 0.0 1.29 -0.86 0.68 1.0 Ql. Assume that you recently graduated with a major in finance, and you just landed a job as a financial planner with Aurigin Inc., a large financial services corporation. Your first assignment is to invest PKR 100,000 for a client. Because the funds are to be invested in a business at the end of 1 year, you have been instructed to plan for a 1-year holding period. Further, your boss has restricted you to the following investment alternatives, shown with their probabilities and associated outcomes. Aurigin's economic forecasting staff has developed probability estimates for the state of the economy, and its security analysts have developed a sophisticated computer program that was used to estimate the rate of return on each alternative under each state of the economy. Avanceon Limited is a technology and communications firm: Cyan Ltd is an investment company and AKGL Co. manufactures foam and allied products. Aurigin also maintains an "index fund which owns a Market weighted fraction of all publicly traded stocks; you can invest in that fund, and thus obtain average stock market results. Given the situation as described, answer the following questions. C) Suppose you suddenly remembered that the coefficient of variation (CV) is generally regarded as being a better measure of stand-alone risk than the standard deviation when the alternatives being considered to have widely differing expected returns. Calculate the missing CVs, and fill in the blanks in the row for CV in the table below. Does the CV produce the same risk rankings as the standard deviation? [Marks 02] D) Assume that the correlation between the Avanceen and Cyan Ltd is perfectly negative. what will be the standard deviation of the portfolio if all the money is invested in only these two shares in an equal proportion. E) Suppose you create a portfolio of T-Bills, Avansegn, Cyan Ltd, and AKGL by investing the funds in equal proportion. Calculate the beta of the portfolio you constructed. [Marks 01| Returns on alternative Investments The estimated rate of return Probability T-Bills Avanceon Cyan Ltd. AKGL State of the Economy Recession KSE-100 0.1 8.00% -22.00% 28.00% 10.00% -13.00% Below average 0.2 8.00% -2% 14.70% -10% 1% Average 0.4 8.00% 20% 0.00% 7% 15% Above average 0.2 8.00% 35% -10.00% 45% 29% Boom 0.1 8.00% 50% -20.00% 30% 43% 1 ? 1.70% 13.80% 15.00% 0 0.00% ? 13.4% 18.8% 15.3 CV ? ? 1.4 1.0 Beta 0.0 1.29 -0.86 0.68 1.0