Answered step by step

Verified Expert Solution

Question

1 Approved Answer

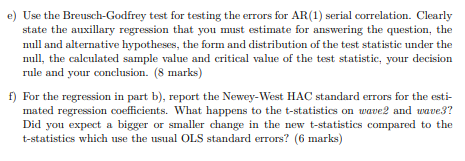

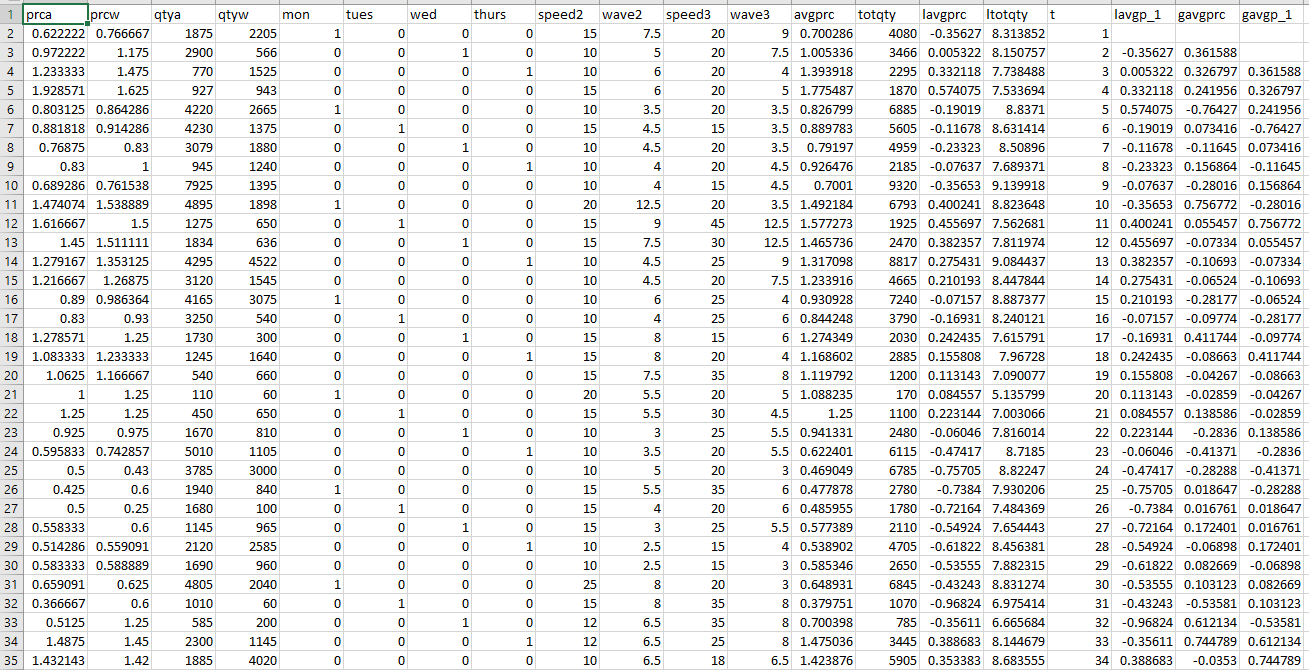

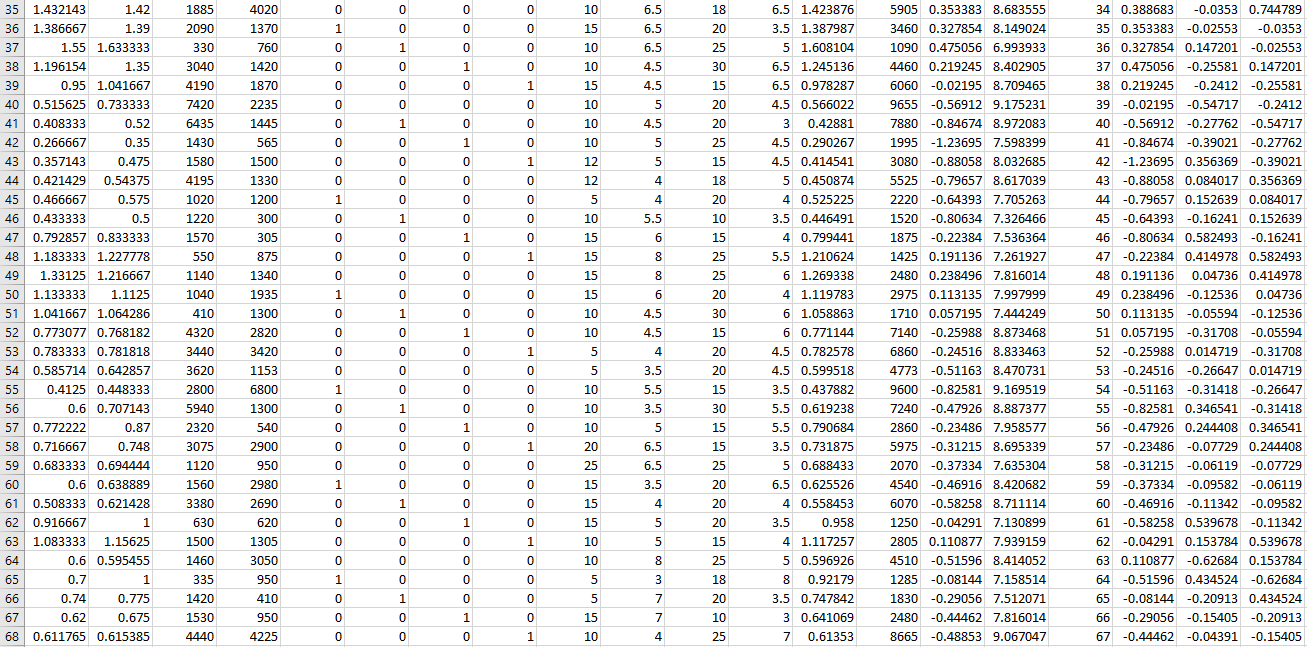

Qn e and f e) Use the Breusch-Godfrey test for testing the errors for AR(1) serial correlation. Clearly state the auxillary regression that you must

Qn e and f

Qn e and f

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Physician Services Verifying Accuracy In Physician Services And E M Coding To Protect Medical Practices

Authors: Betsy Nicoletti

3rd Edition

0998498564, 978-0998498560